Steve Gorelik, what are the best markets in Eastern Europe?

Steve Gorelik is an outspoken expert on investing in Eastern Europe. Here you can find the transcript of two interviews I did with Steve Gorelik in November 2019.

In this interview we have discussed the following topics:

Check out Interactive Brokers

This episode of Good Investing Talks is supported by Interactive Brokers. Interactive Brokers is the place to go if you are ever looking for a broker. Personally, I use their service. They have a great selection of stocks and accessible markets. They have super fair prices and a great system to track your performance. If you want to try out the offer of Interactive Brokers and support my channel, please click here:

Introduction

[00:00:00] Tilman Versch: Hello. In this video, we’re taking a look at investing in Eastern Europe. This video with Steve Gorelik was taken before the coronavirus hit us, but it’s still up to date. Steve gives some interesting insights on how to invest in Eastern Europe, avoid mistakes, and what countries he likes. Enjoy the video. If you like it, please subscribe to my channel.

Hello, Steve. Nice to have you on our YouTube channel. Can you please tell us more about your background?

[00:00:35] Steve Gorelik: Thank you so much. My name is Steve Gorelik. I am a portfolio manager at Firebird Management. Firebird Management is probably best known for investing in Eastern European public equities. We have been doing it for a little over 25 years, celebrating our 25th anniversary this spring. I have been with the firm for 15 years. Probably the best thing to say is to give a little bit of the history of the firm, and then I can talk a little bit about my background as well.

The first investments were in Russian voucher privatizations 25 years ago, when the whole Russian economy was valued at somewhere between $6 billion and $9 billion,

Firebird has been around, as I mentioned, for 25 years. The first investments were in Russian voucher privatizations 25 years ago, when the whole Russian economy was valued at somewhere between $6 billion and $9 billion, depending on who you listen to. Clearly, the opportunity was there, because you’re talking about a relatively low valuation for what is one-sixth of the earth’s surface and everything that comes with it.

A number of people from different western countries have realized that the value is there and have proceeded to find ways to buy up these vouchers. Soviet citizens received the vouchers but did not understand what they were. My parents were those people.

I’m originally from Belarus, from Eastern Europe. To people like my parents, a voucher was just a piece of paper that somebody is offering you real money for. There was no understanding of what it means to own a share in the company. People who came from the US or from Europe did understand and they understood the value of the voucher.

Firebird was started by four people who saw the opportunity, invested in Russian voucher privatization at first, and then proceeded to be one of the first investors in Kazakhstan, Romania, and the Baltic countries of Latvia, Eston, and Lithuania. They have developed the business around trying to go into a market in Eastern Europe when becomes investable from a rule of law and economic growth perspective. We felt it was important for us, as a firm, to learn the opportunities, get to know the people, and, if it was attractive, to put some capital to work.

I have been with the firm for 15 years. Before that, I was an operational strategy consultant at Deloitte. The operational strategy background is very useful to this day in terms of what I do and how I do it. Our investment approach is based on understanding how companies make money and the moats that give them the opportunity to earn outsized returns.

What is also important is how they allocate the capital and what they do to make sure that outsized returns keep on coming. It is a core part of what we do and how we look at companies. My background as an operational strategy consultant is very much relevant to trying to understand that aspect.

After Deloitte, I was at Columbia Business School for two years in the value investing program. That was a phenomenal experience that taught you how to invest from the fund managers. Amazing experience! I have been at Firebird ever since.

What is also important is how they allocate the capital and what they do to make sure that outsized returns keep on coming. It is a core part of what we do and how we look at companies.

Typical mistakes when looking into Eastern Europe

[00:04:01] Tilman Versch: You said you are not just investing in companies from Eastern Europe, but you also know a bit about the US market. If a typical US investor would look into Eastern Europe, what easy mistakes should he avoid?

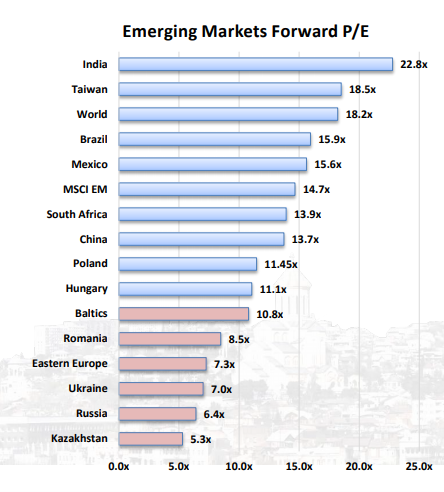

[00:04:16] Steve Gorelik: That’s a great question. When you look at the Eastern European markets, the first thing you see is that they are cheap. The Russian market P/E multiple is around six times right now. If you look at the MSCI Eastern Europe, the benchmark that includes Turkey, Poland, and other places, then the multiple maybe go to seven.

Unfortunately, or fortunately for us, but maybe unfortunately if you are just looking at a way to deploy capital: the benchmarks would feature companies that may not be the best capital allocators. Companies whose earnings do not translate into dividends and do not allocate capital appropriately.

The benchmark in Eastern Europe and I believe it’s the case in a lot of emerging markets, is fairly concentrated with a lot of large state-owned companies that may not be the best companies to invest in.

A cheap multiple is where you start, but it is not the place where you finish. What we found over years, is that it is important to understand how the asset was created and how easy it is to make money. If the asset was created in a questionable way, a way that may be a little weird, then it is possible that somebody will have a way to take it away from the majority shareholder, and you, as a minority shareholder, will get hurt in the process.

If the asset was created in a questionable way, a way that maybe a little weird, then it is possible that somebody will have a way to take it away from the majority shareholder and you, as a minority shareholder, will get hurt in the process.

What we focus on is understanding where the asset came from, how it was created, and how it’s being run. If it is a complicated industry that is difficult to make money in, and the company is delivering excess returns in a young growing market, then you can feel comfortable investing there. If it is a more questionable asset, then you may see something that is trading at a 2 P/E, but it will trade at a 2 P/E forever. It will end up being a value trap.

In Emerging Market investing, it is important to have local knowledge. It is the reason why we do not invest in other emerging markets. We don’t have the local knowledge in Asia, Latin America or Africa, that we have in Eastern Europe. We just don’t feel comfortable with that.

In Emerging Market investing, it is important to have the local knowledge. It is the reason why we do not invest in other emerging markets.

Interesting countries in Eastern Europe

[00:06:47] Tilman Versch: Very interesting. Let us just look into Eastern Europe. There are many countries. Are there some countries which are especially interesting and some where you should be more cautious?

[00:07:11] Steve Gorelik: It’s a very hard question to answer. You should be cautious no matter where you invest. There are two categories of countries in Eastern Europe. There are countries that had stable leadership for a long time for various reasons, like Kazakhstan and Russia, which are resource-based countries depending on the wealth that comes from resources. You can have other sectors develop, something more consumer-oriented, but in the end, you know that these are resource-oriented countries, and you should analyze them as such. No matter what you do in Kazakhstan, it is going to be influenced by the price of oil.

No matter what you do in Kazakhstan, it is going to be influenced by the price of oil.

The other category is countries like Estonia, Lithuania, and Romania, which are all EU members. They are small, open economies. The way that you analyze the companies in these countries is the same way as you analyze a company in Belgium or France, or wherever.

If there is a rule of law, you can count on the courts. You can count on the rule of law. We’ve had cases where we had to defend our rights through courts. We’re not activists, but if something is happening that is hurting our rights as minority shareholders, we will defend our rights. We do it through courts and they work. The courts work even in places like Russia and Kazakhstan. That is not something that a lot of people realize. If you have a clear case, the court system works. There is a rule of law.

In total, there are 37 countries in Eastern Europe. We invest in 11 of them. Other countries, like the Czech Republic, may have a stock market, but it is very shallow. There is not a lot to do there. The companies that are publicly listed there are trading at reasonably high valuations. We think can buy similar companies cheaper elsewhere.

You can have countries, like the ones in Central Asia, where there’s no stock market to speak of. There are countries where there is no rule of law to speak of and it’s too early for us to invest in a place like that.

From the places where we do invest, I can’t say: “This one or that one is my favorite.” There are great opportunities in each country because the region is so overlooked.

[00:09:49] Tilman Versch: What are your favorite markets?

[00:09:51] Steve Gorelik: What are my favorite markets?

[00:09:53] Tilman Versch: Three favorite markets?

Plus COMMUNITY

Discover the Plus Investing community

The Plus community is a great resource for professional investors. Members get support to grow their business and careers, are easily able to connect with other investors and can share ideas and join in-person events.

[00:09:54] Steve Gorelik: My three favorite markets., Russia is a place that will give you great liquidity, and unique world-class companies at prices not available elsewhere.

We own oil and gas companies that are trading at, I think, as of today, it’s 6 to 7% dividend yields. These are world-class companies that are growing their production while generating a lot of free cash flow.

If you take a look at western companies like Exxon or Chevron, they are making a lot of money, but they have to spend that money to keep the production at the same level. If you take an oil company in Russia, like Lukoil, it is making a lot of money. They are spending some of it to grow production while producing a double-digit free cash flow yield that they pay out to you in dividends.

In Russia, there are a number of companies like that, that range from large-cap companies, like Lukoil, to other companies like VSMPO-AVISMA, which is one of the key manufacturers of titanium in the world.

VSMPO is a key part of the titanium supply chain for companies like Boeing and Airbus. They have a world-class asset that comes from years and years of investment. But this is a company that has relatively low liquidity. It trades below a million dollars a day, but it has a dividend yield of I think 9% or 10%, and it’s a single-digit to EBITDA. Any other company in that sector will be trading at an EBITDA multiple of 20+.

That’s one example of the type of things that you can get it Russia, that have amazing risk/reward.

Another place is the country of Georgia. We have been investing there since 2003. We saw a transformation in Georgia over time from a place that was known to be the most corrupt country in the former Soviet Union, to number sixth on the global list of ease of doing business. It just tells you a little bit about how far the country has come.

There is a number of listed companies all of which chose to list in London. The local stock exchange is not very well developed.

One of them is Bank of Georgia, which we owned, if I remember correctly, since 2004. It is trading today at a P/E of under 6 and a dividend yield of 6%, while growing a 10%+, with a ROE of 20%+. At this multiple, I am going to make 20% per year, without multiple changing.

One of them is the Bank of Georgia, which we owned, if I remember correctly, since 2004. It is trading today at a P/E of under 6 and a dividend yield of 6%, while growing a 10%+, with an ROE of 20%+. At this multiple, I am going to make 20% per year, without multiple changes. The company historically traded between 5 and 12 P/E. If the multiple changes, it is also quite interesting.

Georgia, for a number of reasons, is cheaper than it was for quite some time. We think some of those reasons are going to be reversing over next year. If you ask me which country in our region, I’m most excited about next year, it is probably Georgia.

Another relatively major country within our region in Romania. This is also a place that we have been investing in since the mid-’90s. It is a country that went through an interesting transformation in 2011-2012. IMF came in to guide the country after the financial crisis. Part of the recommendations from IMF was that “You guys are part of the EU, but you need to deal with the corruption problems that you have in the country.”

They established an anti-corruption regulator that put people in jail that nobody ever thought would go to jail. That, to us, is a key to the transformation of a country from an investment destination that’s probably a value trap, to something that can generate value over the years.

In Romania, we saw the change in 2012. We saw corrupt people go to jail followed by growth increasing from 2% to 3% per year to 4% to 5% per year. In the process, a couple of companies got listed and the markets got deeper. They were also developing local pension funds.

All of those good things were happening, but over the last couple years, the people who were in power were trying to take the country back in time. They were populists following the blueprint of places in Eastern Europe like Hungary and Poland, which have been taking the more populist approach. Their position was: “We’re going to raise your salaries. We’re going to raise your pensions, but we will also reduce the powers of the anti-corruption regulator.”

Follow Tilman for more insights

Follow Tilman for more insights

Once you lived in a corrupt society and had a chance to live in a society that is free of corruption, you don’t want to go back.

The people went on the streets to protest. Once you lived in a corrupt society and had a chance to live in a society that is free of corruption, you don’t want to go back. People were saying: “You’re trying to bribe us, but we’re not going to fall for it”

The ruling party that got about 40% of the votes after the last election, in the European election received 20% – half of what they had before. They lost their grip on power. The people who were supporting them in the Parliament left them. The government fell apart after that. Elections are coming next year, but you already have different people in power, and the country is being run differently.

You had a situation where companies were doing well, but the market had its issues with the populist government in power. We think next year this is something that is going to clear up.

[00:16:28] Tilman Versch: Thank you very much for these insights. I’m happy to get back into more details in the next part of our interview, so happy to see you there again.

[00:16:36] Steve Gorelik: Thank you so much. This was great.

Disclaimer

Finally, here is the disclaimer. Please check it out as this content is no advice and no recommendation!