Tom Gayner, how do you allocate Markel’s capital? A talk with the Co-CEO

Tom Gayner is the Co-CEO of Markel. In this talk, we have discussed the business of Markel Corporation, how Tom allocates capital and how Tom builds his portfolio.

- MITIMCO's message

- Three songs for Markel

- Looking back at 2020

- The capital raise in May 2020

- Structural changes in 2020

- Measures for success

- Key metrics for measuring Markel's success

- Topics that Tom Gayner wants to understand

- Examples

- Changes in the use and perception of investment concepts

- Owning Amazon

- Where does the money for the portfolio come from?

- Freedom in Markel's cash allocation

- The insurance business - The bullish and bearish parts

- Competitors in insurance

- The Tesla cooperation

- The impact of climate change

- The impact of low-interest rates

- The capital allocation framework

- Decide between different buckets

- The way to decide between inside and outside investing

- Factors to invest in people outside of Markel

- Markel ventures

- What businesses of Markel ventures are especially interesting?

- Everyday life businesses

- Learning in public and private markets

- Tom Gayner, how did get better as an investor?

- The climate in public vs private markets

- Attractive niches

- Why Tom Gayner wants people back

- Buybacks

- Why above 100 positions?

- Keeping focus in the portfolio

- Signal vs noise in the portfolio

- Who influences Markel's portfolio?

- Smaller and bigger positions

- Selling Carmax

- Tom Gayner's trip to India

- India's influence on the portfolio

- Final remarks

- Disclaimer

[00:00:00] Tilman Versch: Today, it’s a pleasure for me to have Tom Gayner of Markel Corporation on. Hi, Tom, how are you doing?

[00:00:07] Tom Gayner: I am well. Thanks so much for having me.

[00:00:09] Tilman Versch: Great that you’re here! As we were planning the interview, I asked you to bring three songs as you have been a DJ in your youth and I want to connect to this for the start of our conversation: I asked you to bring a song that describes Markel’s last 10 years, a song, even the opera or whatever you want to say, for the year 2020 and a song for the next 10 years. What are the songs, but before we go into this question, let me just show you the disclaimer that we are on the safe side here. You can find the disclaimer link below the video and it says, just do your own work. And what we’re doing here is no advice. and no recommendation. Always do your own work and I’m also happy to drop a message from our sponsor:

MITIMCO’s message

This episode of Good Investing TV is brought to you by MIT Investment Management Company. MITIMCo manages the financial assets of MIT through partnerships with talented investment managers all over the world. MITIMCo is eager to connect with emerging fund managers. They invest alongside young and unconventional investment firms, and bringing resources and a creative perspective to the fund management journey. Whether you’re a one-person shop just getting started or a team of investors building something unconventional, MITIMCo would love to hear from you. No firm is too small, too early, or too un-institutional. You can drop them a line at partner@mitimco.org and visit their site: mitimco.org/emergingmanagers.

Three songs for Markel

[00:02:09] Tilman Versch: Thank you very much for listening to the message of MITIMCO. I’m happy to come back to my conversation with Tom on the three songs I asked for. Maybe let’s start with the song that describes Merkel’s last 10 years. What have you picked Mr. DJ?

[00:02:25] Tom Gayner: Well, you were kind enough to send me that question in advance and the problem with getting the question advanced is that implies that I’m actually going to do homework and be diligent and think about it in preparation for a meeting like this. And so often I prefer the spontaneity of answering your question at the moment without any pre-thinking things about that. So when you first started talking about music and favorite songs, the real answer to that is that’s like asking me to name my favorite children or my favorite family members or something like that. There are so many songs. Music is a continuous backdrop to my life. I turn it on first thing in the morning when exercising or running or something like that. And I just have the randomizer throw up things from the playlist that I’ve built over the years, just cause I like to be a little bit surprised so there are a lot of songs that I draw energy from and motivate me.

So now I’ll confess. For instance, if you’re trying to do this kind of response, quick and unfiltered when I thought about what song would best describe the next 10 years of Markel I went to a Frank Sinatra The best is yet to come. So that was the first one that came into my mind, but I love music and then the song that talks about the last couple of years, and, you know, the last 10 years have actually been quite good the last couple of years, we’ve had some challenges. There’s a group called the Wilson Phillips and they did a song called Hold on. So, your listeners may or may not be familiar with that, but no, that was something that had popped into my head about music and then, you know, another favorite song and to call it a song is a little bit cavalier and a little bit almost disrespectful, but since you’re a German by native, this occurs to me, Beethoven six symphony is I think some classical music, but I love a lot of pieces of classical music. But if you ask me to name a piece of classical music real quick, That would be the first one that pops into my head and it evokes sensation and emotions for me. So those are just little tiny snippets and examples of music that is of interest to me.

[00:04:43] Tilman Versch: I see you haven’t lost your talent as a DJ and for picking some interesting songs

[00:04:48] Tom Gayner: I’ll add to my father. I developed my love of music from my father. And when he was asked what kind of music he liked, his response was “I like any kind of music as long as it’s good.” And that would really be my response too, because I don’t want to unnecessarily narrow the music that I would listen to, and I don’t wish to have preconditions and a closed mind. So again, in the same way, that one should approach, you should approach music the same way as minded people willing to listen to some stuff you haven’t heard before you might learn something. I don’t want to listen to just the things I’ve already heard. Although I do that a lot.

Looking back at 2020

[00:05:27] Tilman Versch: Let’s look at 2020, a really challenging year. How did it open your mind going through this year and what came new to your mind this year?

[00:05:37] Tom Gayner: Well, I think this year, one of the themes that came out and I tried to write about in the annual report quite a bit was just the notion of resilience. And you’ve heard that from a lot of people. So things that we did not see coming, that we had not planned for, that we had not expected happened and those were tough gut punches and there were moments of despair and challenge that we had not gained a plan for quite frankly. But yeah, we continued to press on and dust ourselves off and go to work every day and figure things out and that happened in personal life, it happened with your family it happened with my colleagues at work for Markel as a whole. So to be tested in the way that 2020 did justice, and to come out on the other side and demonstrate that this is indeed a resilience machine and a mechanism that is designed to handle things that you can’t foresee. And in fact, do reasonably well at that time, that’s very encouraging and very inspirational.

The capital raise in May 2020

[00:06:41] Tilman Versch: You issued in May 600 million of preferred stocks and you weren’t that expressive on buybacks if I go through the numbers. There was one critical question coming from Twitter on this. Was this a misjudgment of risk you did in hindsight?

[00:07:02] Tom Gayner: Certainly in hindsight, it could be well criticized that we were in a position that we thought that the extra $600 million of capital that we raised, that we did do as a practical matter to the first quarter Of 2020, when you look at the combined ratio and the insurance operations, plus the drawdown in the equity markets and an uncertain environment into what the next day would bring to be double safe, double secure that had a cost to it. There’s no question about that, but it also has an epic payoff and that double assured the resilience and, survivability of the Markel corporation, so tactically, when we sit now with 9, 10 months of hindsight and how things turned out, you know, we were fine, but in the moment we felt it was important to add to the capital base. There’s some expense doing so, but there’s some returns from doing so as well.

Structural changes in 2020

[00:08:04] Tilman Versch: Haveyou shifted anything structurally based on the experience you made in May or April of this year?

[00:08:12] Tom Gayner: I think it’s not unlike what would normally happen in the insurance business, which is our heritage and core business. For any insurance risky write, all of the data that you have relates to things that have happened in the past. Now you use that and you would be unwise and ignorant not to pay attention to what has happened in the past, but the risk you’re writing for is the future. And sometimes the future is different from what the past has been. Now each time you go through something like that and you get surprised, and we’ve had that with things like hurricane Katrina, Rita, Wilma that episode in life, the Northridge earthquakes back in ‘92, all of those went beyond and through some of the model expectations of what losses would be, but in each and every instance, you refine your models, you have new data, you have new learning, so it’s more robust the next time around.

But I think that is the fundamental nature of the business that is likely to continue to be the case forever. And you just have to always be resilient and have enough margin of safety, that things that surprise you and you don’t foresee well, they may hurt. They may sting. They may leave a bit of a Mark, but they’re also the times when you learn and figure out how to iterate, in tactical and strategic ways, to be better the next time around

Measures for success

[00:09:38] Tilman Versch: For the future 10 years, your name, the song, the best is yet to come. How do you want to measure this? The best that is yet to come. What are your measures for your success in the next 10 years?

[00:09:51] Tom Gayner: Well, I think, from an external point of view, there’s layers to the answer to that question, from an external point of view, if you were not an associated Markel or you don’t have a first degree of connection to the company, so you were only a shareholder only observing the stock price. I would certainly hope that 10 years from now the stock price would be meaningfully higher than it is right now because that would be the culmination of all of the efforts and all of the things that are going on, on a daily basis around here.

For someone who’s here and an associate of the company or a customer that come in here, somebody has ongoing relationships with the company, we have the win, win, win architecture, where we want associates to be better off because they are part of this company. We want our customers to be better off because they’ve done business with us. We want shareholders to be better off because they’ve provided capital to us. So the way I would, where you can measure the third one is just looking at the stock price, the feeling that an employee has, while you can have some metrics like turnover and surveys that give you employee satisfaction scores. But I also think that it is a mistake to think you can be overly precise about that. It’s a sensation of thinking about whether your relationships are working or not. So, as an example of that, here in a few short months, I will celebrate my 40th wedding anniversary. And I can tell you that…

[00:11:21] Tilman Versch: Congratulations

[00:11:22] Tom Gayner: Thank you. There are no scorecards. There are no report cards. There is nothing, there are no gimbal walk charts or anything that talks about how the marriage is going. But 40 years later, we are still in it together and we laugh. We smile and we enjoy our family. So, it’s going well. And that sensation that you have in personal relationships, there’s only so much one can quantify and to over quantify, it probably would risk damaging the relationship itself. At least in the context of marriage, I think it sure would.

Key metrics for measuring Markel’s success

[00:11:57] Tilman Versch: But as you know, investors have a certain love for numbers and looking at Merkel’s performance. What are the numbers you indicate shareholders to look at? Besides the stock price? Book value was already mentioned in some comments coming from Twitter, some said your growth and book value declined from 15 to 10. They ask if it’s structurally or if you come back to the 15% or I would also add my question is book value, really the number to look at?

[00:12:31] Tom Gayner: Right. I think book value is not as descriptive a number for Markel as what it used to be. So if you went back 20 or 30 years, when Markel was exclusively an insurance company, think of an insurance company and the three financial statements that comprise the financial statements, the balance sheet, the income statement, and the cash flow statement. Well in an insurance company, the balance sheet is the most important of those three financial statements and the book value per share, which you would derive from looking at the balance sheet and looking at balance sheet year after year after year, that did a very good job of describing the economic progress of Markel over time.

With the addition of both Markel ventures and our insurance like securities business and insurance services businesses, those really are more income statement businesses and cash flow businesses than they are balance sheets. They’re asset-light, in the term that you’ll hear people say, so the book value attributed in associated with those businesses does not really speak to or describe their economic performance very well. So in those businesses, I think, and for Markel, you would look at cash flow metrics. EBITDA is one. We’ve talked about that being the least worst proxy. Or the economic performance of the market ventures businesses. And I would say actually can do that for, for ILS and insurance services as well.

So we’re somewhat of a hybrid. And I think it’s interesting to note that for instance, in the Berkshire annual report this year and the letter that came out, Buffet abandoned the book value chart that had historically been at the front of his letters when opening the book value per share over the years and referred solely to the market price per share appreciation over time. And I don’t know whether he used these words exactly or not, I can’t recall. But in essence, what he’s telling you is that the market in essence gets it right. And ultimately figures out what appropriate values are. And the directional information you glean from looking at the market price per share over time does indeed do a very good job of describing the underlying economic performance of the business itself.

Topics that Tom Gayner wants to understand

[00:14:58] Tilman Versch: To be successful in the next 10 years learning is key. Maybe share a bit with us what you’re currently trying to understand as an investor, as a businessman. What are you trying to understand? What are you trying to figure out at the moment? What are topics that move you?

[00:15:18] Tom Gayner: Well, that’s a fascinating question because I think any fair answer would involve multiple layers. And the big risk here is in simplifying and only speaking to one or two or three dimensions when there are constant dimensions. Andy Grove was one of the founders of Intel, one of the great executives that’s ever walked the face of the earth. One of the books that he wrote, it was called `Only the paranoid survive.

And there’s a certain calibration of paranoia that you should have that, if you have too much of it, you can’t function and you’ll go into the mental illness state of what paranoia describes. If you don’t have enough of it, you get complacent and you don’t have a fear of the things you don’t know such that you’ll go stale and, and get left behind. So you’ve got to have that paranoia meter that, at a certain level that just keeps it in balance. So the fact of the matter is, not being complacent and just always having curiosity and always just wondering. What the next thing is, would be the best way I would describe how I would think about what you should learn.

My wife, who runs a business when she’s interviewing people and trying to find, colleagues and associates to hire, would use the phrase. She likes to find people, ask the, `and then what` question and, what’s next, and have just a sense of natural curiosity about them, such that they’re always just trying to figure out the next thing and the next thing, and the next thing after that. So to answer your question, I think obviously the way in which technology is changing daily operations changing the sense of knowledge, one would have about any particular thing. Those are table stakes, and you have to be better and better and better at that all the time. The thing that I think perhaps is undervalued and that I would expect, it’d be something that the competitive advantage Markel over time is the idea of empathy and always keeping the human dimension first and forefront in your mind. And always trying to think about things from your customer’s point of view, from your colleagues’ point of view.

Rather than your own natural point of view, that mindset and that sensation is not natural. It’s not automatic. It’s not the way people would be wired automatically. So to have that as part of our culture and our system, and constantly reinforce that message about, well, how do other people see this? How’s the customer going to feel about this? thinking about things from other people’s points of view. I think we can match people in the realm of technology. And I don’t think we can ever allow ourselves to fall too far behind. And I think it is unrealistic to think we’re ever going to get too far ahead, but in the sense of empathy and trying to see things from other people’s points of view, I think we can always be world-class at that. And I think that applies, no matter what business you’re in.

Examples

[00:18:29] Tilman Versch: Are there any examples you can boil this? What you’re trying to understand down to something concrete.

[00:18:36] Tom Gayner: I’m hard-pressed to think of some off-the-cuff example that would, that would, that would bring that to life. But I can recall just many, many conversations around our dinner table as examples with my kids growing up where they would say something in the way a kid would. And I would introduce what we called the concept of other people sometimes with air quotes “the concept of other people.” So it was just drilled into my kids or around the dinner table. And, it’s something that I say around here a lot because I find myself in situations where sometimes it seems like we’re not really thinking about other people, so let’s just stop, pause and think about something from someone else’s point of view. And it’s amazing what sort of insights you can, you can gain from that.

Changes in the use and perception of investment concepts

[00:19:28] Tilman Versch: Stop-pause is a very interesting point to go to for my next question because it’s about investing concepts and where have you discovered certain concepts you use in the past where you said stop, pass, rethink this. Does it really make sense? Do I have to modify it? What are examples where you have changed your usage of investing concepts?

[00:19:53] Tom Gayner: Well, for instance, and one of the ways in which, technology and the environment as it is, is different today than what it was 20 or 30 years ago. If you looked at petrochemical companies and oil companies for a long, long time, those were some of the leading most profitable businesses in the world in the last 10 years, it appears the fundamental economics of those businesses may have changed dramatically. So were we shareholders in take example, Exxon Mobil 20 years ago, the answer to that was yes. Are we shareholders in Exxon Mobil today? No, and I don’t claim to be making a statement that says it was a good idea at one point or a bad idea, I don’t know, but I do suspect that the fundamentals of that business are different than what they were 20 years ago. So to think that you can just own something that the thesis would be sound and the thesis for owning it would be unchanging forever. That’s probably oversimplifying the case and you do need to rethink why you own things and what you think the next five or 10 years old as opposed to be too wedded into what the last 5 or 10 or 50 years have been.

[00:21:13] Tilman Versch: Is there another example for you at trusting on investment concepts?

[00:21:19] Tom Gayner: Well, another example would be, many retailers. So it would be a critical sort of component of mine. My thinking that says, look, I’m, I’m not a smart guy, but I try really, really, really hard not to be a dumb guy. And there’s, there’s a big difference between the two so smart people can figure out the new, new thing, and what’s coming next sometimes and make these spectacular returns. And I’ve never really been very good at that. When you think about any white-hot story over the last 20 years, some name that jumps to mind is something that well, if you bought that early on and you’ve held onto it, you just make tons of money. Hmm, my skills at picking that up is very, very limited.

But if you look at things that have really deteriorated and gone away and just become terrible businesses, I’ve been pretty good at staying away from those. So as an example of that. We own a reasonable size position in Amazon. I was not an early, early investor in Amazon, but eventually did sort of figure it out and stop being so, so, so blockheaded that this was really a substantial sound profitable growing business with amazing competitive advantage. So we started buying some and because we have regular cash flows, dollar-cost average. It continued to buy more and more, and there was never one particular entry point or price that it made some dramatic statement, but we accumulated it over a number of years and done dramatically well with that.

Now, in addition to owning Amazon, I also thought about. Well, if Amazon is doing well, what might they be displaced and who might be in their competitive crosshairs, such that there, you know, the economic circumstances of those businesses are severely diminished. So we got out of the way and really didn’t own any mall-based or, or main street retailers for the last 10 or 15 years simply from the insight that if Amazon is doing well, it is, it is some aspect of a zero sum game. So who were they doing well at the expense of? Things like that will be ways that, that the thinking plays out.

Owning Amazon

[00:23:43] Tilman Versch: What belief did you have to give up to be able to own Amazon in a good way?

[00:23:50] Tom Gayner: Well, you needed to be, I’m an accountant by training, you needed to be a better accountant And as I always joke, the way I went from accounting into investing is the opposite. The accountant. It was more interested in dollars than numbers, and there’s a big difference between the two. So for instance, in the early days of Amazon, it appeared to be unprofitable, but you had to look at the nature of the expenses they were incurring that if they have been a manufacturer and they’re building a plant. What would have happened in an accounting sense? So it would have expended a bunch of money and it would have been capitalized. It would have created this asset. And then the expense would flow into the period income statements bit by bit by bit by bit over what the accountants deemed would be the useful life of that asset.

Well, since marketing and building up the customer lists and things like that were really equivalent to manufacturing plants Amazon appeared to be unprofitable, but really what they were doing was creating long-lived assets. And you just needed to be able to think through that and make some assumptions that if they spend X well, while they, while they showed a hundred percent of X flowing through the income statement that year and made it look like they were losing money, that X they were spending If you really thinking about it in net present value kind of math, what would be the lifetime value of the customer relationships that they were getting for that and match up your timeframes to a longer-term rather than year by year, you would have, you would have seen more easily that on an economic basis, they were profitable way before GAAP financial statements made them look like they were profitable.

Where does the money for the portfolio come from?

[00:25:42] Tilman Versch: Amazon is a good bridge to the point I want to do in the next part of our interview. It’s looking at the conditions your decisions are made and trying to re-understand them better and even look a bit deeper into your portfolio. And we have the chance. There’s a lot of data and it’s already public to take a look at this portfolio. I want to use this point. To just tease it on for the audience that we are walking step-by-step to this portfolio investing in. It’s not only this portfolio, you’re partly responsible. It’s also the portfolio of Markel ventures. But before we go into these two buckets and you will help me try to understand how you’re acting there. I want to understand where the money for all this investing is coming from. So have you found a golden pot on the end of a rainbow somewhere in the countryside or where do you get the money from for investing?

[00:26:49] Tom Gayner: Well, no, we’ve not found the golden pot and by the way, I’m not aware of anybody who ever has, although the stories are told of it continuously and there are a lot of people chasing this, but I’ll set that aside. Fortunately, I joined Markel back in 1990 at the time it was a relatively small, specialty niche insurance company, but I got into Steve Markel, Tony Markel and Alan Kirshner and what I thought of them was they were really smart. They’re really creative. They were kind, they were good people. They were fun to be around. And I just had the sensation that over time they would do very well. I was also familiar with The Berkshire business model from that time. And I had seen how Buffett had taken an insurance business and used the profitability of the insurance business to leg into ownership of publicly traded equities, and then control of up entire businesses.

So the playbook was out there. Buffett had described what he was doing. From the early eighties, but first got a tangential awareness. But by 1990, when my opportunity to join the company had come about the playbook was pretty well developed, pretty mature, and pretty much out there. So yeah, Markel was in Richmond, Virginia. I happened to live in Richmond, Virginia and happened to be the analyst at a small local brokerage firm who was covering them. So I had all sorts of overlapping touchpoints and cross points to become aware of the company. In 1990 Markel did one of their double the size of the company deals. Steve Markel had been handling the investments, largely single-handedly. At that point, he had had more to look after and asked me if I’d like to help him. I said, well, that sounds like fun. That was my strategic plan for the rest of my life.

So that’s what’s been going on since, since 1990 is that, there was an insurance engine that insurance business has historically operated with underwriting profitability and culture, the DNA, the creativity of Markel has always been willing to invest the bulk of that insurance profitability into the ownership of equity securities, both publicly traded and, in the case of the market ventures companies, controlling interest in those companies. And that’s, that was the buffet playbook that was out there for anybody to see and follow.

Freedom in Markel’s cash allocation

[00:29:24] Tilman Versch: Referring to the Buffett playbook, I did get a question from a shareholder of yours, Michael Gilligan. Is your current cash balance freely investible or does it serve, for future claims, like Buffett mentioned that he could invest relatively freely?

[00:29:43] Tom Gayner: Well, we don’t have as much range of freedom as what we have. If you look at the size of Berkshire relative to the amount of insurance premium that they write and the nature of our insurance versus GEICO which would be a law of large numbers in the variability of outcomes would be pretty dag-gone tight. There would be more variability in the insurance so that comes with a little more constraint over how widely we could invest, but by and large, the cash balances at Markel, which are higher than they have historically been, are indeed largely available for us to invest proactively. When time circumstances, ideas lead us to things we want to do.

We’re in a good position to be able to do those things. And you need to have those sorts of cash balances at hand. When the time comes to act because the time has come to act if you’re not in a position from your balance sheet to act upon it. Well, then that’s just an idea that you play on paper. So it doesn’t really do us or the shareholders any good. So we always want to be in a position where we have the liquidity and the capability to act on a good idea when it comes around. Now, what that also means is that at any given instant, you probably are always carrying some degree of cash and short-term liquidity that is in excess of what you’re using at that particular moment. But you never want to be in positions where you don’t have as much cash as you want. So we’ll, we’ll accept the burden of carrying too much. That’s a very high-class problem.

Plus COMMUNITY

Discover the Plus Investing community

The Plus community is a great resource for professional investors. Members get support to grow their business and careers, are easily able to connect with other investors and can share ideas and join in-person events.

The insurance business – The bullish and bearish parts

[00:31:24] Tilman Versch: Maybe let’s take a short look into the insurance business, which is not your main playground, but I think you’re well in knowledge about what’s happening there, which part of the insurance business you’re a bit bearish on and which part are you most bullish on in your insurance operations?

[00:31:45] Tom Gayner: Well, within our area insurance operations, clearly we’ve talked about the fact that we’ve not earned the sorts of returns that we think we should for our shareholders in re-insurance over the last couple of years and heavy-duty property, catastrophe insurance coverages that we have been cutting those back over the last couple of years. we have been charging more increasing rates and getting more rates per unit of risk, but the actual costs of the risks have increased at a faster rate than what we could get rate for. So we’ve again taken another step back from that portion of the business as we roll into 2021 and the rest of the portfolio and the rest of the book, that business has been doing pretty well and I’m pretty optimistic that we’ll continue to be able to do going forward.

Competitors in insurance

[00:32:41] Tilman Versch: Have your insurance operations developed through the last years a certain angst against lemonades or other new, fresh fintechs?

[00:32:54] Tom Gayner: Well, there’s several aspects of that. So for instance, to some degree, some of the insurance services, operations that we would have are part of the way that fintechs actually conduct business. So if you look at the fintech world, typically their expertise would be in marketing or risk selection and slicing and dicing what kind of business they want and how to write that at the same time, insurance is a regulated business and it requires a capital base, to support the claims that ultimately come from insured losses that anybody who’s writing insurance is going to have. So in many cases, we’ve actually partnered with some of the FinTech companies and we would do the backend of that business to have a balance sheet that would have regulatory mechanisms, all of those sorts of things. And we think that’s important because of the whether we wish it or not, whether we think it’s a good thing or not, it is reality and FinTech is out there.

So we need to work with them when, when circumstances are appropriate for us to do so, we need to observe and learn and see what they’re doing and adapt to change our processes when they have a good, new, fresh idea. And that’s just the nature of the world in which we live is that new ideas, new technologies are always coming around and you need to be constantly trying to develop them yourself and staying aware of them, and adapting your own operations as appropriate to remain competitive.

The Tesla cooperation

[00:34:29] Tilman Versch: What happened with your cooperation with Tesla?

[00:34:33] Tom Gayner: Tesla was a client of some of our insurance services operated. So it’s a perfect example of where Tesla had an idea about what insurance costs should be and wanting to offer an insurance product to their customers but they needed licensing regulations, things of that nature, so we were able to provide them with that on a fee for service basis. I think, and then again, you’ve correctly identified that this is not my day job, so I’m not at the point of expertise about that. I think they have found some other people to do that for them right now, but that’s the nature of things. We were a fee for service provider for Tesla

The impact of climate change

[00:35:18] Tilman Versch: Then let’s go again on the higher level. How does climate change influence the insurance business at Markel?

[00:35:25] Tom Gayner: Well, largely through the kinds of losses that are recurring. So the property catastrophe losses that we spoke of one never knows exactly what, what causes the wind to blow and the earth to shake. But climate change is clearly one of the factors that’s out there in the world in which we live. So we look at the data, we look at the experiences as to what is happening. We try to have some measured view about what might happen going forward and whether one can collect enough premium to pay those risks or not. And if you can, okay, and every day you learn more but also the rate you might charge for something where you think climate change might indeed cause higher losses you either need to charge more for that risk or not write it and we would do both of those every single day.

[00:36:20] Tilman Versch: Is there a tendency that you’re losing business due to this or that business isn’t doable anymore?

[00:36:29] Tom Gayner: I would say that every day there’s business that we are accepting and a business that we are declining. And if we are correct in our sense of what the true costs of the risks are that should be improving the net economic position of the Markel corporation with each and every decision as a practical matter. We get some of those, right and we get some of them wrong. The thing that would matter to our clients and Markel shareholders over time is that we get more of them right than wrong. And that the size of the decisions would be such that, when we get them right more than offset the times we get them wrong, but it is inevitable in the nature of insurance that we pay out a lot of claims. If you look, the single biggest expense of our insurance operation is the dollars we pay out in claims. And that is as it should be, that is the marker and the metric for taking care of your clients and making sure that you were there to provide them with some money, some cash and capital at their time of need. That’s what they bought insurance for.

The impact of low-interest rates

[00:37:37] Tilman Versch: What is the impact of low interest rates for Markel on the whole bench?

[00:37:42] Tom Gayner: Sure, well, interest rates and the interest income one would earn from the normal heavy allocation of fixed income that any insurance company would have is part of the equation of what makes the economics of the insurance world work. So if you collect a dollar of premium today, generally speaking, that is in anticipation of some loss that might happen in three months, three years, somewhere down the road. So any and every insurance organization that exists has embedded and attached to it an investment operation that holds that money and invests it until such time as the claim is paid, you would, you would calculate in rougher, precise terms, how long you think you’re going to hold onto the money and how much you think you would earn an interest come while you’re holding onto it to help price the policy that you ultimately offered to the customer.

So all other things being equal, and that’s an important statement, because generally speaking in this world, you never get to be in a situation where all of the things are equal, but if all other things are equal, then, whatever rate you would offer a customer for an insurance product, you would need to raise that to increase the amount of income you would expect to generate from the underwriting profitability itself, rather than from the investment earnings you would earn while holding the money so it’s just part of the equation, but there are other steps and facets to that that go into it. And one of the key things to remember is that if interest rates go down, that’s not a unique situation for Markel. That’s true across the industry. Everybody is dealing with lower interest rates. If interest rates go up, then everybody will deal with the higher interest rates. It’s an environmental factor that anybody in the insurance world would have to deal with.

[00:39:50] Tilman Versch: Do they profit your investment portfolio?

[00:39:51] Tom Gayner: In a short term basis they would increase the Mark to market valuation of a fixed income portfolio. But, I think you should keep going and beside whether they really help or not, lower interest rates would take your math, net present values and with everything that already exists, everything you’ve already done, if interest rates go down, you would think they would be worth more. And your financial statements would say that they are indeed worth more. But what I always think about is not just what has already happened, but what happens next? What’s the “then what” question? So the ability to reinvest that money, which is where the real compounding takes place in the future not the past. The mountain gets higher and taller and harder to climb when interest rates are down.

But the amount of return that you need to earn, earn good real rates of return when that goes down too. So I don’t think about interest rates that much because I have no control of it. And so why spend your time thinking about things over which you have no control. I’m better off using my limited brain cells, thinking about the things that I perhaps do have some control over rather than, don’t have control over and interest rates just fall in that category

[00:41:19] Tilman Versch: But you have to factor them in a bit if I use the picture of mountain climbing, then you have an idea of the mountain and find good strategies to climb it. This is the challenge of capital allocation. While is your framework at Markel for capital allocation.

[00:41:37] Tom Gayner: Well, let me go back to that question about interest rates, because they are really, again, I have no control over them, but they do pervade and drive everything. So when I was a kid, I grew up around Philadelphia and there was a museum in Philadelphia called the Franklin Institute. And I loved that museum. I spent many Saturdays just roaming the halls of the Franklin Institute. And I recall one of the things they had, the Franklin Institute was this room. Where they had scales that were trying to teach you something about gravity and how gravity worked and the relationship of the sun, the earth, and where gravitational forces came from. So you would stand on the scale and that scale was called earth, and you knew roughly how much you weighed. So you would step on that scale and that number would make sense to you and tell you how much you weigh. Well, then you would step on a scale called Jupiter or Mars, which was either closer to, or further away from the sun and a number would come up as to what you weighed, if you were on the surface of Jupiter or if you were on the surface of Mars. And what it was trying to reflect was that there were different amounts of gravitational force that applied and those other places.

So interest rates really are like gravitational force. And if interest rates are at the base rate and the 10-year treasury, when I came to work here in 1990, I can’t remember what it was, but it probably was 10 or 12% or something like that. Maybe not. I don’t remember the number, but something along that level. Well, if that’s what the ten-year rate is, to earn real returns you need, if the rate was nine, you needed to earn 10, 11, 12, 15, something like that to start earning real, not nominal with real rates of return. And you could know if the base rate right now, I mean it’s 10 year treasury as we sit and talk today is about 140, 150, something on that level, the idea that you need to earn 15% on your capital, like they did when interest rates were 10, 11, 12%. That’s not true. And I don’t think on large amounts of capital, you really can earn exaggerated returns like you, like you could nominally 30 years ago because the world base rate of capital being provided these days is 2% or you know, where, where you are. I think the base rate is perhaps negative. So an entirely different environment from a nominal point of view, but whatever it is, nominally, we’ll add a couple of hundred basis points to that. And if you are earning that while you’re starting to earn historically very good real rates of return which produced compounding.

The capital allocation framework

[00:44:26] Tilman Versch: So how has your, again getting back to the question that I already dropped, how has your framework for the capital allocation of this capital been?

[00:44:36] Tom Gayner: Sorry to talk over you there. The framework, and this is where I think the beauty of Markel, starts to exist is that we have a 360-degree view of capital allocation. So, and we’ve written about this in the annual report for many years, the first and foremost thing we would look to do as we would look at our existing operations business, we’re already doing people who’ve been part of the organization for a time, have proven their ability to earn good rates of return and whether those in the insurance businesses or some of the ventures businesses or the ILS businesses, when those people who are already part of the team have opportunities that they think they can earn good returns on capital. And they raised their hand. And want some capital to support, that’s the first and most joyous way in which we would allocate capital. Secondly, we would look for acquisitions, to increase the size and scale of where we can deploy capital and earn good returns on that.

Thirdly, we would look at publicly traded securities, whether those are equity, securities, or fixed income securities, where we think we can earn good rates of return, and forth, we would look at our own common stock. And possibly repurchase that if we thought we had fully funded the first three buckets of capital allocation and that our stock was reasonably priced. And over the years, there have been points in time when we didn’t fire at all four cylinders at the same time and some of which we’ve not. And currently, we’re in a position where we, you know, are, are looking at all four of those options and acting on all four of those options. But that’s really the frame we look around, each of those, each of those opportunity sets.

Decide between different buckets

[00:46:30] Tilman Versch: How do you decide between the different pockets, buckets sorry

[00:46:33] Tom Gayner: Well, those they’re in order in that order for a reason. So how we decide would be that we are trying to allocate capital to its highest and best use. Now, if we have somebody who’s been here for five or 10 or 15 years, and they have a proven record of being very good at running their business and earning good rates of return. Maybe they come and suggest that they have some idea that could, I’m just making up a number, a 12% return while somebody else who you don’t know who have no relationship with comes across the transom and suggests some idea that they could produce 15%. Well, 15% is more than 12. So shouldn’t you take the 15%? Well, maybe, maybe not, you should attach some degree of certainty, some degree of confidence that you have into whether those returns will actually take place or not.

So it is my bias, and I think it reinforces our culture that, for people who are inside the organization have done a very good job, we want to say yes to those people. That creates energy. It creates Goodwill. It creates positivity. It rewards people for good work, and we should do that first. Before we allocate limited capital to someone coming across who can say wonderful things, but we don’t have any first-hand experience, whether they can do wonderful things. So those are extreme examples, but we’re, we’re on a risk-adjusted basis. If you want to call it that way, a degree of confidence adjusted basis. We’re trying just to make sure we’re allocating capital to its highest and best use.

The way to decide between inside and outside investing

[00:48:21] Tilman Versch: I want to use this example of the 12% and maybe say someone comes and says he has a 20% return he could make. How do you decide in this example, who is the better use of the capital? What do you factor in your hurdle of decision-making?

[00:48:43] Tom Gayner: Well, again with that example which we’re playing out the 12%, that was internal, you have hard data on that. That’s somebody already inside the organization. So you have a proven historical track record that gives you data, which you feel confident in because you’ve seen it. It has taken place under your own eyes. When anybody comes at you with a story or a proposition or a theory that is external you can and should have a different threshold and process by which you evaluate that. Now, one of the reasons we come to work every day is because we do want to talk to people like that. We do want to hear their stories. We do want to consider what else is out there. Our history and our DNA is designed to accept and accommodate new ideas and new ways of doing things and new ways of thinking about things, but it’s a different hurdle right than what would happen for somebody who’s internal.

Factors to invest in people outside of Markel

[00:49:56] Tilman Versch: But you’re investing in outsiders. What factors make you confident to invest in these outsiders?

[00:50:04] Tom Gayner: Well, that’s in the same way as would take place for insiders we are not ever going to be a hundred percent right. So, we try to be thoughtful. We try to be rational. We are trying to be reasonable. We try to be informed and then you make your decisions and you see how it plays out. And it always just gets back to this law of large numbers sensation that you want to be right. More often than you’re wrong. And you want to be dollar-weighted or whatever currency you’re in, you want to be dollar-weighted right more than you’re wrong. I mean, for instance, I enjoy playing poker.

Well, I have some friends that I’ve been playing poker with for 30 years and, and it would not be uncommon to go through a night where, if there were 50 hands of Poker played in an evening, maybe I only played in five of them or eight. Folded my cards 40 times and either lost very small amounts of money or were folded even before you had to put it in again and that’s okay. But when you stick around and you keep betting and you stay in a hand, you want to win this. And at the end of the night, if there were 50 hands played and you lost or didn’t participate in 45 of them and you made a little money in three, but you had two really nice wins. That’s a nice night in the bunker. And that’s exactly the sensation of what we’re talking about here.

Markel ventures

[00:51:37] Tilman Versch: Let’s take a look at my Markel ventures. What is the history and the concept behind Markel ventures? Are you now one of the crazy winter players throwing billions after unicorns or what is standing behind Markel ventures?

[00:51:51] Tom Gayner: Right. Well, I can assure you that. Yes. We’re not throwing billions after anything and we’ve not thrown them after, after unicorns or things of that nature. So we’re not pursuing venture capital kinds of ideas. We’re pursuing proven businesses. So, the concept and the belief Markel ventures circles back to what we were talking about in terms of capital allocation, where first off we invest in our existing businesses, our existing people, and fund that to the extent that we have opportunities and ideas to do so.

And then the second thing we would do after that is acquisitions of companies and businesses that we don’t already have. Now, historically, the way Markel got started, those were insurance businesses. For all. And for a long time, many of the deals we did were limited to the realm of insurance. In 2005, which was the first year we started in Markel ventures, there was a company called AMF baking equipment. It happened to be headquartered here in Richmond, Virginia. I happened to know the gentleman who was the CEO of the business. I happened to,, through just relationships around town, find out that it was for sale and found out what the circumstances of the company were. And I thought this was a great opportunity to buy a business that was not in the insurance realm, but would produce good economics.

And we started with that in 2005, we bought it and that was the first transaction in the base of Markel ventures. Now in 2005, we were getting into a market environment where prices were starting to go up in general. I mean, it was sort of a hot market out there. So what I thought businesses were worth and what sellers that businesses worth, that that gap started to open up and we were not able to buy any other businesses for a couple of years and the next Markel ventures business we didn’t buy until 2008, when financial markets started to be different and prices started to be different and opportunities started to open up to buy things at rates and prices that we thought would produce good returns. So we’ve bought a number of, I think, 17 at this point of businesses over the years, they’re wonderful market-leading companies at what they do. We do everything from the. From the AMF, which makes commercial baking equipment. So if you eat a hamburger and have a hamburger, the bun has very good odds that it was baked on our equipment and we think there are a lot of hamburgers and hot dogs being eaten all around the world. And AMF has been a leading company at supplying that since the 1930s.

What businesses of Markel ventures are especially interesting?

[00:54:30] Tilman Versch: Let me show the overview of these businesses and connected with a question: What are the three businesses, it’s hard to choose from businesses you’re owning and like it’s maybe the same to choose from children, but currently the three businesses you think, here are the best stories for shareholders. They could be especially happy about owning this business.

[00:54:55] Tom Gayner: Well, I think all of these are wonderful businesses in their own way. Now some of them are very profitable and they have very large market share in the business that they’re in. And as a consequence, their opportunities to grow are perhaps somewhat less than some other businesses because they’re already very much the leader in that market, but that’s okay because they produce very wonderful returns and the returns that they produce, we can then reinvest all around Markel in that 360-degree view that we were talking about.

So the good news about all of these businesses that you look at is that they are very good at what they do. They take care of their customers. They take care of their associates. They make their customers happy generally speaking, those businesses are all ones that have a lot of repeat and return customers, which is a validation of the fact that they are doing a good job of taking care of their customers. Some of them have the opportunity to take that money and reinvest it to grow. Some of them are somewhat constrained in their ability to grow, but they’re part of a team that can, they can use that capital to continue to grow and expand all of Markel so that they’re all unique stories, but I think Markel shareholders should be pretty happy with each and every one of them.

Everyday life businesses

[00:56:15] Tilman Versch: Is there any business shareholders can get an attachment to Markel in everyday life and they don’t even know it?

[00:56:18] Tom Gayner: Well, in terms of consumer products, I’m trying to think. So for instance, Brahman, which makes handbags and leather products, things of that nature, any shareholder in the world. And I would encourage them, reaching in my pocket right now. So this is a Brahman men’s wallet, generally speaking. They tend to sell more of their products to women for handbags, but men could get in on the action too.

I’ve got a Brahman wallet, I’ve got a Brahman, a briefcase. So I encourage you to go to brahman.com and look at their products. And yeah, you can, you can walk around with a piece of Markel any time. Probably most people are not going to buy commercial bread, making equipment for their own kitchen. Or, or a trailer which could haul cars around because they got their car.

[00:57:07] Tilman Versch: That’s good news.

[00:57:12] Tom Gayner: So these are indirect pieces of.. for instance, HAVCO and you can see over my right shoulder here, that wall is actually a HAVCO floor. It typically would be found in the back of a tractor-trailer. So, for tractor-trailers that you see going up and down the road, hauling everything you need, whether that’s groceries, furniture, everything that gets moved by truck. Well, we have a wonderful business that makes flooring for these trucks so the stuff doesn’t fall out on the road. So, while you may not know that your stuff, whatever you have, got carried to you on a half go floor, there’s actually a pretty good odds that a lot of what you live and use on a daily basis is indeed hauled around in trucks that have floors on them.

Learning in public and private markets

[00:58:03] Tilman Versch: Before we go on into the more public market you’re investing in the stock market, you have an insight into the private market with the business under the umbrella of Markel ventures and the stock market. How do you currently see the differences in both markets and, how’s the acquisition climate in the private market from your stance?

[00:58:30] Tom Gayner: Right. Well, one of the points that Buffett made many, many years ago when Berkshire was starting to invest in controlling the interest of businesses more profoundly and expanded from the public security side, was that he said being an investor made him a better businessman and being a businessman, made him a better investor. And I have found that very much to be true. So if you are solely focused on public securities and things of that nature, while you can be very good at that, and there are skills that are involved in being that but I find there is a layer that gets attached to when you’re actually responsible. Well, for running businesses, as we are within Markel ventures, you see these things in flesh and blood and people and the real sensation of what’s involved in running a business and the things that are necessary to run a good durable, enduring business over time, that flow and that sensation and that information that you get in each realm helps the other.

So I think being responsible for the businesses themselves helps make me a better stock picker and a better picker of investments to own because I know how hard it is to run a good business. Similarly, having lived my life in the investment world, when it gets to capital allocation decisions within a business, I think I have first-hand experience with how that works and which ones tend to compound and work better over time, such that I can be helpful in the business setting itself when the capital budgets are being set and the notions of what acquisitions they might do or how they’re making their capital decisions because they have had first-hand experience in the equity markets as well. So it goes back and forth and I think that the ability to operate in both spheres makes you better in each one.

Follow Tilman for more insights

Follow Tilman for more insights

Tom Gayner, how did get better as an investor?

[01:00:34] Tilman Versch: What are examples for this getting better? If you would go back to the young Tom starting off at Markel with investing what lessons would you give him?

[01:00:46] Tom Gayner: I think the first and foremost lesson that you get in that sense is to have a better appreciation for how hard it is to run a really good business. That’s a challenge. So for instance, some of the mistakes of omission that I’ve made over the years would be, if you, if you had a really good public investment and you found a company that you thought was doing a really good job, and you had some notion for what it was worth, and you thought it was selling at a discount and you bought it, and then it went up above that and above your target price. If you use that kind of mechanism or your sales target price, wasn’t whatever, and you sold it, and then you proceeded to realize that probably that sale, in the long run, was not wise because the things that made that business good, continued largely in place. And it compounded it year after year after year after year. And you made a profit. You wouldn’t be criticized for not making a profit cause you did, but you realize that if you had just held on, you would have done way, way, way, way, better over time because it could have compounded.

So my appreciation and sense of that has helped me to hold on to public equity positions more so than might have been the case earlier on in my career because I know how spectacular it is to run a really good, good business. Similarly, if you have a business that is just fundamentally challenged and structurally difficult, sometimes it is tempting for an equity investor who can buy and sell things and trade much more easily. When you’re trading pieces of paper and buying and selling and being responsible for real businesses in flesh and blood human lives, you can be seduced by a cheap price and own a mediocre business at a great price.

And maybe you can trade that. I’ve really lost interest in doing that. When I was younger, I did try to fool myself into thinking that I could successfully execute those sorts of strategies, but I’ve come to the conclusion that that’s just too hard a game. And from observing what a good business is, and maybe businesses that are part of are so good and have structural challenges when you find good ones, stick to them and stay with them

[01:03:12] Tilman Versch: So no more cigar butts.

[01:03:15] Tom Gayner: Not if I can help it.

The climate in public vs private markets

[01:03:18] Tilman Versch: That’s good. I want to go back to the acquisition or the buyer climate you’re having in both markets. What do you see in the private market and what you see in the public market? Are there any big differences currently?

[01:03:33] Tom Gayner: I think in general prices are high. And I think that relates to a lot of things. There’s market psychology going on. The dispersion of prices I think is a little bit higher and wider in public markets than it is in private markets as a broad brush general statement. There are pockets within the public markets where prices are very, very high. And we are in a period of time where there have been some spectacular successes in venture capital, light companies, and newer entities that have great promise of things that are going to be someday but have not necessarily proven out that the case so far. So there are a lot of things in the public market that you would find like that there are cases in the public market where there are companies that are not so exciting to people or not as attractive or interesting and the psychology and the fringy frenzy hasn’t really developed. So there’s actually some reasonable pockets of valuation in the public markets.

In private markets because private equity has grown so much because the number in nature of transactions is so much more than what it would have been 10 or 20 years ago. The notion of prices in the private markets tends in very broad bus general terms too, to be on the high end. And everybody thinks their business is a great one. So they all want the high price and they don’t want a price. That is what the last person got without perhaps adjusting for the dispersion of what, what their business is worth, or how good it is compared to other people’s business.

Attractive niches

[01:05:19] Tilman Versch: What are the niches or the regions, you still find attractive?

[01:05:25] Tom Gayner: Well, for instance, I get back to Markel these days. I mean, if you looked at the insurance industry in general, as I look at… And here’s an example and it’s, it’s not a large holding, it’s not something that we’ve invested big dollars in, or, or that I have an opinion about, but, earlier. This week, Allstate raised its dividend by 50%. And if you look at Allstate’s returns on equity and their performance over the last couple of years, I would argue that Allstate is pretty good at what they do and have consistently done so for, for many, many years of pretty good returns on the capital, they have a good consumer brand name, and had that happened in a different industry right now, I think probably investors would have snapped to attention and raised their head as a signal of good news. As it turns out, on that day that Allstate raised their dividend by that much, I don’t know if the stock was up down or, or what, but it, it, it didn’t move very much. And I understand that the dividend rate has no actual theoretical implication as to what the stock should be but if you, if you look at the fullness of their performance over a reasonable period of time, it seems to me, the market’s not head over heels in love with it. So that would be an example of something where the valuation seems reasonably attractive.

And I think if you look across the insurance industry for a variety of reasons, not the least of which were the losses that the industry had in 2020 with the pandemic and whatnot and investors aren’t, head-over-heels in love with the insurance industry. As I’m looking around and thinking about where valuations might be attractive, our own insurance business bite might be pretty attractive.

Why Tom Gayner wants people back

[01:07:17] Tilman Versch: Is I want you back currently a song that comes in your head when you’re thinking about your stocks?

[01:07:23] Tom Gayner: Well, I want you back. Yes. It’s funny. You should ask that. So in the Jackson Five, which was what I think is the original group that recorded that, we’re talking about remote work and the ways in which the world has changed, I’m an extrovert. I like being with people and I played that song more than once over the course of the last week thinking about reconnecting with colleagues who are working remotely, love to see you in person and, and cherish and welcome opportunities to do so. And in fact, one of the things we would have to share is our annual meeting, which is on May 10th, we’re very hopeful that we can have that meeting in person. And we love the time that we get to spend with our shareholders.

We love the relationships that are built in person. We’d love serendipitous conversations that can’t be planned or scripted, and we have no control over what the circumstances will be, but it appears as though the trends are getting better, vaccines are on the horizon, the incidents rates are going down. So if circumstances permit, we’re going to have our meeting on May 10th in person, and we would love to see you. We would love to see your listeners and people who are listening in person and we would welcome the chance to house them in Richmond, Virginia at that time if we can. So yeah, we want you back

Buybacks

[01:08:49] Tilman Versch: And will you announce on your annual meeting then, if you can say this here, or maybe let’s phrase this differently, is there a chance that the song will be played in relation to stocks you bought back and you got back? How attractive do you currently think your valuation of your stock is?

[01:09:11] Tom Gayner: Right. Well, I think it might well, and by that time we’ll be reporting our first-quarter results. So let’s stay tuned for what you might see as examples of we want you back

Why above 100 positions?

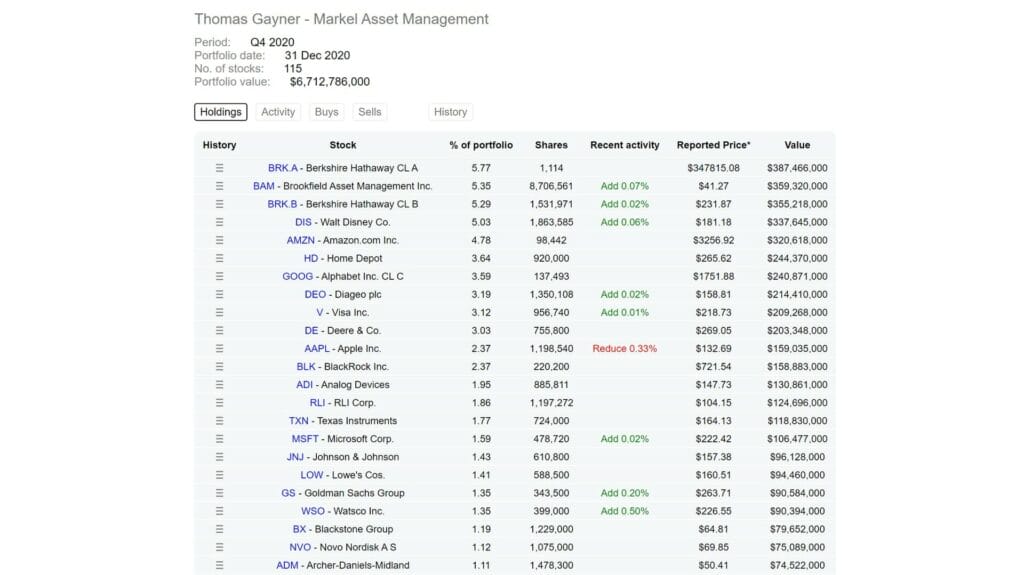

[01:09:25] Tilman Versch: That I will. Let’s take a look at your portfolio as I already promised you can have a look at the. Positions, you have to disclose on Dataroma or other portals and what comes for me as one first observation. When I see the portfolio as the number of stocks you’re owning in a 115, how should one understand this number? Is it really different positions or do you think as positions, as groups? How are you, what do you think about the positions you have?

[01:10:09] Tom Gayner: Well, I think there’s a lot of layers involved in answering your question. One simple answer is, do you think of positions as groups in some cases, Yes. The answer to that is yes. So for instance, Diageo is a very large holding for us. Brown-Forman is a modest size holding for us. To some degree I would group those together and that they both are producers of alcoholic beverages. There’s other degrees of overlap that would exist in terms of a consumer product. So if you were doing a Venn diagram of some of those, there would be a large amount of overlap. Similarly, you’d see some concentration in the realm of insurance or, or financial, and it could have some overlap now. The top 20 names…

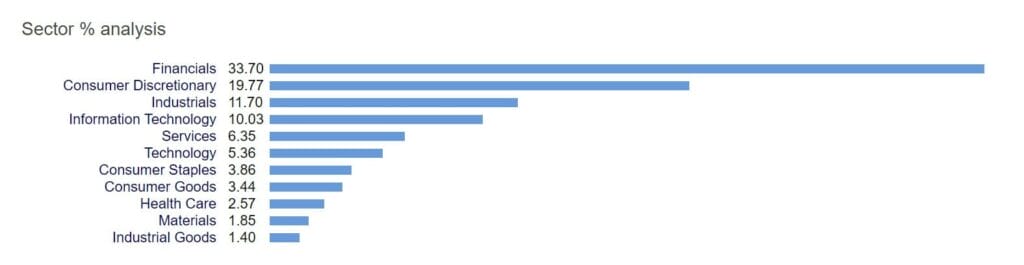

[01:11:02] Tilman Versch: Here you have the numbers based on sectors.

[01:11:06] Tom Gayner: Right, and that’s not my work, I don’t know which analyst did that but it’s probably directionally correct. I don’t really think about it from a sector point of view, but if you looked at the top 20 names, that would oftentimes be 60%, maybe, maybe up to two thirds, maybe 55%, something like that, depending on how things were on any given day. But the bulk of the portfolio would be accounted for by the top names. Now, one of the ways that I’ve thought about it, my whole life has been the top 20 names, it’s kind of like a baseball organization. So if you were looking at a major league team, the New York Yankees to the Baltimore Orioles, they would have farm tapes. So there’s the major league roster. Let’s call the top 20 teams, the roster of the major league team, those baseball teams have AAA teams, AA team, A teams where they’re evaluating talent. They’re looking at players. They’re looking at athletes and some of those athletes are going up on the list. Some of those athletes are going down on the list.

I find just from my own mentality owning some stock in something causes me to pay more attention to it, to be more connected to it, to think about it more than I otherwise would. If the stock goes up or down by reasonable percentages when it’s a small player, I accept the point that that in and of itself is not going to move the needle for Markel, but it can inform other decisions and things can get promoted or demoted over time. So that process in and of itself, I find to be quite helpful.

Another more subtle point. And I’ve listened to some of your interviews with some other folks that you’ve talked to. There was a very famous investment book by a guy named Charlie Ellis called Winning a loser’s game and this book dates back maybe 40 years now or something like that. And he talked about the example of tennis. If you’re a world-class tennis player and you’re playing at Wimbledon, generally speaking, that each shot you hit, you’re trying to win the point. So you’re attempting to defeat your opponent on the other side of the net by hitting a shot that they can get back together. If you’re a recreational tennis player or anything other than the very, very, very top tier. And you wanted to be very good at your club or the local parks or anything other than the very, very top tier, the number one strategic thing you should do is try to hit the ball back over the net and let the other guy hit it into the net because the mentality is always to try to hit that winning shot, go for that extra twos and to be excellent. And it is an unnatural thing for competitive people, such as myself, such as the people you interview, the people that you would broadcast to.

We all want to be the best. But there’s a really bizarre thing in the world of investing that to be among the very best and to not necessarily think that you would be the best in the world, but really, really, really, really good at what you do, to adopt that mindset of a little more calmness and just trying to be good and hit the ball back over the net, rather than trying to get the win. That, in and of itself can produce better returns and they can be more durable returns because they have less risk of having something traumatic or really bad happen. And they can be more scalable because the ideas can apply to more capital over more time. So I’m really trying to win the loser’s game as Charlie Ellis would talk about. And so, I completely acknowledge that there are a lot of people in the investment world who are smarter and better than me, and they talk about using their advantage and to use their intelligence and their skills to really see that pay off. They want a smaller number of names in their portfolio. They want a 20 stock portfolio or a 10 stock portfolio, or boy if you were really smart and you knew you would have a one-stock portfolio buy the one that’s going to go up the most. Why don’t you, why don’t people do that? Well, because you know, in your heart of hearts really should but you’re not that smart.

Now I’m going to accept the fact. There are a lot of people who are smarter than me, so they could have a 10 stock portfolio or 12 stock portfolio, or even a 20 stock portfolio. I think A) I’m not that smart and B) within the context of being a steward who’s responsible for the assets of an insurance company, and to make sure that we’re always there to honor the claims that policyholders will have, it is appropriate to dial back that degree of ferociousness or intensity. And trying to win, win, win, win, win, and play a game of, to some degree, not lose it.

And that is a subtle and somewhat dangerous lie to get it just right? Because if you play too much not to lose and too defensive, you’re going to sink into a morass of mediocrity. And I don’t know how to tell you how to calibrate that or where to have that line, but I can tell you for 30 years, I’ve thought about that. And for 30 years, our success has been such that I could argue that we do a pretty reasonable job of trying to calibrate that and figure that out. And I’ve heard the commentary that, that that’s just too many stocks. For the vast majority of your audience, that might well be the case, but I have different circumstances here. And the nature of the money that we are managing here is different than many of the other folks who you might have on.

Keeping focus in the portfolio

[01:17:16] Tilman Versch: How are you keeping focus with 115 positions? Because there are 115 signals that are screaming at you at a certain point or just want to have a bit of intention.

[01:17:28] Tom Gayner: Well, yeah. Generally speaking, if data is good, more data is better. So to your point about having 115 things that are bombarding you with information and flow, I think those things and that flow is extraordinarily helpful in helping me make decisions about the things that are at the top 20 tier. So I accept your point, that it may seem like the focus is diffused, but in my wiring and way of doing things, I find that those signals are helpful in helping me to make better decisions on the things we’ve put more weight behind.

Signal vs noise in the portfolio

[01:18:13] Tilman Versch: Let’s go back onto the idea of focus and the quality of data you already mentioned. What are these aspects, you`re laying your focus on to understand the signals from the positions you have?

[01:18:28] Tom Gayner: Well, included in the sensation of the positions that we would have, and the sources of data are the actual operating businesses of Markel ventures. And by the way, also that includes the insurance business. The underwriters around here are seeing economic activity and insuring pieces of economic activity. So it has been of immense value over the years for me to wander the halls and talk to people of the organization and to see what their business flows are like and where things are getting better, where things are becoming more challenging so I can’t put my finger on any one particular aspect or particular point, but to come to work every day, always be curious to always be listening, to always trying to have a sense of what I’m hearing and learning from all of the different sources that I have. That’s what I do all day, every day. And I like having more of those rather than fewer.

Who influences Markel’s portfolio?

[01:19:34] Tilman Versch: If you think of the handwriting of the portfolio, is it just your handwriting or are you, do you have a kind of model like Warren has: all the possessions up the billions, the 1 billion, 2 billion, 3 billion are his, the bigger ones that list when he does, and he has tapped and taught who are doing the smaller positions?

[01:19:57] Tom Gayner: Well, over the years, I’ve added two folks to the team who help in the equity management process Dan Gardner and Sarah Bodan, Sarah has been here three or four years now. I lose track of time and 10-ish, sort of years. Again, I lose track of time, so don’t hold me on that. Exactly. The good news is the relationships with those guys as such I feel like they’ve all they’ve always been here. Although the fact of the matter is, I guess I was here 17 years before hiring Dan. Now, one of the wonderful things that has been the case at Markel over the years, as we’ve had some wonderful shareholders and we continue to, and I always tell our large shareholders, I said, “the ironic thing is that you’re smarter than I am but in actuality, I’m managing money on your behalf.” So, the relationships and the friendships that we’ve built over the years with some of the large shareholders of Markel, those are wonderful ways to have conversations and to stay plugged into thoughtful observations about businesses and companies, and who’s doing what, and I’m just trying to stay plugged into that flow.

And over the years, I’ve found those all to be parts of the mosaic that comes into the Markel portfolio. So I don’t have specific, sentence diagramming type techniques to tell you how this name got in or that name got in or what I was thinking when I bought this, what I was thinking when I bought more of this or sold that. But that’s what I do all day every day is to try to stay plugged into the flows, which I’ll be thoughtful about that.

Smaller and bigger positions

[01:21:37] Tilman Versch: What does make a stock qualify for being a smaller position in your portfolio, like a 0.01% holding? And what makes it qualify to scale up, maybe make it a 3% position?

[01:21:53] Tom Gayner: Right. Well, the four lenses and we talked about this in the annual report, but we want to run good businesses profitable with good returns on capital that don’t use too much debt and too much leverage to do it. We want the management teams to have equal measures of talent and integrity because one, without the other, is worthless. We want the businesses to have reinvestment opportunities and or capital discipline. And we want to be able to buy them at fair prices. So those are the four lenses that we would look at everything through. So if something somehow or another found its way into the portfolio, it means I’ve made some initial judgment about each of those four aspects. And every day that goes by every month, that goes by every quarter that goes by I’m continuously rethinking that. And retesting the hypothesis and re-evaluating it on each of those four dimensions. And when I think that I’m right and that things are continuing to play out or we buy more and more of that. And when I’m wrong, we sell and do less and less of it.

Peter Lynch in, again, older investment literature talked about sort of the general experience that people tend to psychologically be more comfortable selling winners and things that they’ve made money on and holding on to losers until they broke even on just the psychology of that. Well, we’re pretty good and not doing that. And Peter Lynch called that pulling the flowers and watering the weeds. So we were trying to do the opposite of that. We look at the things we’ve done and, and again, this is why I think it’s a value to have some small positions and tiny things that you had scattered around. Those are seeds in the garden and some of those seeds start sprouting and showing the promise of becoming good plants. Those plants you give him more soil. You give them more fertilizer. You give him more water. You give them more sun and you nourish them and then they become bigger and bigger positions. And the ones that don’t well, you plow over that ground to try a different seed. That it’s a very organic type of process.

Selling Carmax