Sebastian Grabmaier, can JDC digitize the Germany’s insurances?

JDC is a German company trying to digitize the insurance sector with its software and service approach. Together with the co-founder Sebastian Grabmaier, I could do a deep dive into the company.

We have discussed the following topics:

- Check out Wise*

- Introduction to Dr. Sebastian Grabmaier & JDC

- Why get out of bed every morning?

- JDC's history

- Sebastian Grabmaier onLearnings from difficult times

- Focusing on one thing

- Tips for the "past self"

- Re-capitalizing JDC

- The insurance industry

- Clock speed in the insurance industry

- Early mistakes

- How JDC solves problems

- The B2B2C model

- Difficulty in comparing insurance companies

- Onboarding insurance products

- Project cycles in insurance

- Sebastian Grabmaier on the saving banks

- Where they earn money

- Maintenance costs of the infrastructure

- Room to grow

- Improving with a client

- Comdirect

- Reasons for losing customers or change of contracts

- Tenders

- Having a platform that stands out

- Thought experiment on Amazon

- The data flywheel?

- Digitalisation

- Community Exclusive: Impacts of the pandemic

- Addressing customer needs

- Demographic shift within the broker industry

- Example of Deka

- Choosing a specialized broker

- Germany within the European market

- Expansion

- Competition for JDC

- A look into the future

- The right management mindset

- What investors look for

- Staying ahead of the game

- Disclaimer

Check out Wise*

[00:00:00] Tilman Versch: Are you planning to travel abroad during the next weeks or months? Then please check out the service of Wise. They offer free credit cards and very good exchange rates, so if you want to pay locally with $, €, swiss francs or any other currency, Wise has a big repertoire of currencies. Their solution might be an interesting option to consider. You can also store foreign currencies in their accounts – and even get interest payments on them!

Introduction to Dr. Sebastian Grabmaier & JDC

[00:00:40] Tilman Versch: Dear viewers of Good Investing Talks, it’s great to have you here back for another episode of the podcast. Today, I have another interesting European company. Mr Grabmaier, it’s great to have you here. Your company is called JDC or Jung, DMS und Cie what is the spelling of the company?

[00:01:02] Sebastian Grabmaier: Well, it depends on whether you are German or not. You say, Jung, DMS und Cie or JDC group is fine.

Why get out of bed every morning?

[00:01:09] Tilman Versch: Okay, that’s great. So, you have been in the position of the CEO of this company for 17 years now, so let me ask the first question about like the motivation for running that long and staying in the same position that long. So, what drives you out of bed every morning with a level of ambition to work and challenge with this company?

[00:01:33] Sebastian Grabmaier: Well, my partner Rob and I, founded the company in 2002 and went public in 2005, when we developed the first digital, that was a consolidated account statement in the fund industry, so were the first company in Germany to tell our clients and customers the performance of different investment funds that were located at different investment companies. And from there on until 2008, we founded the leading investment platform that sold one billion investment funds in 2008.

So, the biggest platform apart of the German bank. When Lehman happened, we had very challenging times after, we started from scratch in the insurance industry. What drives us is to deliver our customers, so the final retail customer, a full 360 degree on his financial assets both investment and insurance, which is much more complicated insurance to have like a real financial home for the clients. So we are a completely client-driven company and in our business model, we enable all kinds of intermediaries to deliver these tech developments that we internally develop to our retail clients.

When Lehman happened, we had very challenging times after, we started from scratch in the insurance industry. What drives us is to deliver our customers, so the final retail customer, a full 360 degree on his financial assets both investment and insurance, which is much more complicated insurance to have like a real financial home for the clients. So we are a completely client-driven company and in our business model, we enable all kinds of intermediaries to deliver these tech developments that we internally develop to our retail clients.

JDC’s history

[00:02:43] Tilman Versch: This already brings the bridge to a chart I have prepared with my highly skilled possibilities here. It’s a printout of your stock price chart, and maybe you can explain a bit the phases in more detail if you’ve already touched it in your answer. What phases is the stock price been going through?

[00:03:07] Sebastian Grabmaier: We never were a start-up company because we started by merging three existing companies with routes back to 1958. So we were an existing sales company. But then we had the first wave of digitisation until 2008 when we have a very steep development after this little tech investment we made. We attracted 10,000 brokers, and we were a very successful company in the German investment markets, only to find out that after these booming times in 2008, we had a terrible down, followed by Lehman.

And to be honest, if your sales drop off by 80% at the same cost base, we almost couldn’t make it. You could see it in the chart where the share price dropped to 150 at the lowest low. Ralph and I did a buyout and refinanced the company to have enough investment to start from scratch in the insurance realm. So now we have the leading tech stack platform for the processing of insurance companies. And then you see that the share price then now takes it up again, and now we have very good prospects to be the winner in the platform business for the processing of insurance contracts.

Sebastian Grabmaier onLearnings from difficult times

[00:04:27] Tilman Versch: Before we go to your good story, maybe let’s stick a bit in the face of 2012 to 2016 when you had real financial problems and issues. What did you learn from this time that helps you today?

[00:04:44] Sebastian Grabmaier: Well, it’s like meekness, if you want. It’s like when you start up a company and everything runs well. You’re enthusiastic and you have even higher targets. But then when markets go completely in another direction and you have extrinsic shocks such as in 2008, 2009. You’re way more aware of what was important in building up a company, being more profound. Now, it’s very important that we are not only relying on one asset class such as investment, or if you look at the HyperPort story now, the problems they have because they have like mortgage only. So now we are quite diversified in our product portfolio and therefore we rely on them a huge number of very small cash flows like aggregating all these little cash flows of these insurance contracts that are on average €35. So we’re not dependent on a small number of big clients, we’re not depending on the small market because we are now in the overall broad market with 4,000,000 very small cash flows. So, well more balanced and recurring revenue and so much more stable than it ever was.

Focusing on one thing

[00:06:01] Tilman Versch: Are there any other lessons you took away from this time on how to build the business today or even in the future?

[00:06:09] Sebastian Grabmaier: Well, in 2008 we were part of a bigger group, and were conquering the world. We have five partners, had offices on 4 continents and had a very different business model, and now it’s all about focus, focus, focus. So Ralph and I bought the company out of the partnership. We’re now doing one thing only, it’s only the processing of financial products. So it’s not like a thousand business models or not even three, but it’s one model where we think we are now the market leader and that we follow this path and from that point on it’s much easier to take the decisions. It’s focus, focus, focus, so that’s the key learning.

It’s focus, focus, focus, so that’s the key learning.

Tips for the “past self”

[00:06:54] Tilman Versch: It’s a bit of a tricky question, but if your younger 2006 self would meet you today and ask you for venture financing. Would you give that to him?

[00:07:06] Sebastian Grabmaier: Oh, definitely. 2006, we were the new kids on the block, Hot Cheat. So that was the thing to finance or to put my money and I think looking back in 2006, nobody could have imagined that in 2008 a real banking group would go bankrupt.

Banks would not lend money to each other. So it was not in our minds. So with the same historical learnings or mindset, for sure, there was really a company to put the money in. And it’s the same today. Now, let’s say 12 years later, or 14 years later, well, the company’s more stable and well more mature. But from the prospect on, it’s even much better than it ever was because the insurance market that we are now in and that we are very successful in is much bigger than any investment markets or mortgage markets. It’s 10 times the market, and we are at the same point in conquering this market that’s vacant still.

Re-capitalizing JDC

[00:08:16] Tilman Versch: You already mentioned this with a small note that you and your partner took some, I think private money, to refinance the company in 2012 or something like this. Why did you do this? Maybe you can tell me a bit more about this.

[00:08:32] Sebastian Grabmaier: By 2012, we’re in a position where we knew that the investment world would not recover that fast and we knew we had to put money in to develop what’s now the leading tech stack in the market and from this, we knew it would take about 20, €25 million. So what did is we pledged all we had, all our private homes, everything we had in our small bank accounts, and found some investors that gave us money on the private side that we then put into a capital raise in the company. And this is when we started the tech platform.

So it was a very high risk from our side. So we’ll venture into financing from our private side, but we believed in the digitization of the insurance industry. And now, on a yearly basis, investing another 6-7 million a year after a complete investment of more than 70 million. We have now a complete platform for the processing of insurance contracts that just turning out to be very profitable.

So it was a very high risk from our side. So we’ll venture into financing from our private side, but we believed in the digitization of the insurance industry. And now, on a yearly basis, investing another 6-7 million a year after a complete investment of more than 70 million. We have now a complete platform for the processing of insurance contracts that just turning out to be very profitable.

The insurance industry

[00:09:35] Tilman Versch: Why insurance?

[00:09:38] Sebastian Grabmaier: The insurance industry is interesting because it’s huge. It’s 6 1/2% of the German GDP, but it’s very slow.

The insurance industry is interesting because it’s huge. It’s 6 1/2% of the German GDP, but it’s very slow.

You know most insurance companies still live on heritage systems, IT systems that are 30, 35 years old. This means that there is no standard data because it comes out of the machines just as it developed. And it’s the only industry that completely slept in digitization. And well, if you say that there are industries that will not digitise at all, then we are not the right company.

But logic tells you that everything is digitising and where everything goes into platforms; insurance has not. So if you buy an investment product now, 15 years, 20 years ago you would fill in a paper and send it to whatever, Fidelity or Templeton. And eventually, two weeks later would came back. Today, you would have the expectation, as a customer, that the next cut-off time, like the next day in the morning, the fund sits in your depot. But insurance, same day, you would still accept to fill in paperwork and this is not very modern.

So it’s easy to say as you can save about 30, 40% cost of everything, insurance spending and digitization. So it’s very logical to just make insurance processes much more efficient and just start digitization. And today, our biggest clients are the insurance companies themselves which don’t come to you at first point, but we offer insurance processes to insurance companies. That’s exactly the point where the industry now uses our systems to improve their efficiency.

So it’s easy to say as you can save about 30, 40% cost of everything, insurance spending and digitization. So it’s very logical to just make insurance processes much more efficient and just start digitization. And today, our biggest clients are the insurance companies themselves, which doesn’t come to you at first point, but we offer insurance processes to insurance companies. That’s exactly the point where the industry now uses our systems to improve their efficiency.

Clock speed in the insurance industry

[00:11:19] Tilman Versch: Let’s talk a bit about time and also time to success. We had this experience in the fund industry where we all came out of this small bubble we had last year and but things go quite rapid, prices go up and down, and also like cash flows from this kind of businesses go up and down. And then there’s the insurance industry where you said it’s quite, let’s say stable, and their timeframes are different. Maybe you can try to compare both timeframes from both worlds or especially what kind of timeframe investors have to think when they think about like structural changes in the insurance industry winning business there.

[00:12:00] Sebastian Grabmaier: Yeah, so there is already a big base. So there are 450 million insurance contracts in the German market alone. 450 million. It’s a premium volume of €220 billion in what’s paid by customers to insurance companies every year. So that’s a huge number. What people do not know is out of these 220 billion, almost 30 billion, three zero billion, are paid to intermediaries as commission and other payments. And most of it is recurring. So 2/3 come year over year over year with the automatic renewal of the contracts.

So it’s a huge money stream coming in very small portions that these €35 each. So it’s a huge industry that develops slowly because even if growth figures on a 450 million base contract and move up by 5%, you don’t feel it in the huge amount of insurance contracts. So it’s all about aggregating existing policies and not so much on new business, so the waves are much slower but at the end of time you have less volatility and smooth development of growth. So that makes the market interesting because there’s no way that your insurance policy never became cheaper. So your car insurance goes up your household, your building, insurance, everything goes up with inflation or more than inflation. As a commission is diving into the premium it’s like an inflation-protected model.

Early mistakes

[00:13:47] Tilman Versch: When entering the insurance market, what mistakes have you made and where have you corrected them?

[00:13:55] Sebastian Grabmaier: Well, we didn’t have any sales volume insurance at first, so we had to buy a number of companies just to get the entry barriers, to get like a top condition with our insurers. So we bought a full number of sales companies which gave us a starting point. And as you can imagine, when you buy a number of companies in a very small timeframe, not every company was a good idea. So this is what you also can see, a lot of on our balance sheet, a lot of impacts like these companies that we bought with the big tax shield, for example, with lost forward and that we still have. But then we sold the company without it, so you still can see it in the balance sheet. And I think there was no alternative to developing this way. But there is one or another company that we shouldn’t have bought. That’s learning.

Well, we didn’t have any sales volume insurance at first, so we had to buy a number of companies just to get the entry barriers, to get like a top condition with our insurers. So we bought a full number of sales companies which gave us a starting point. And as you can imagine, when you buy a number of companies in a very small timeframe, not every company was a good idea. So this is what you also can see, a lot of on our balance sheet, a lot of impacts like these companies that we bought with the big tax shield, for example, with lost forward and that we still have. But then we sold the company without it, so you still can see it in the balance sheet. And I think there was no alternative to developing this way. But there is one or another company that we shouldn’t have bought. That’s learning.

And it’s all about the people. It’s about the managers that sit on the companies. And if you look very thoroughly at them you might see where the company is and what the development might be.

How JDC solves problems

[00:15:10] Tilman Versch: Let’s take a look at your current business angles that you currently have and maybe let me start with–

[00:15:17] Sebastian Grabmaier: I like the paper charts, by the way, Tilman.

[00:15:19] Tilman Versch: Yeah, it’s the problem I can’t show it here in digital, but in the video, we will see it as a slide, that’s embedded. What kind of problems are you solving with these businesses for the customers you’re serving?

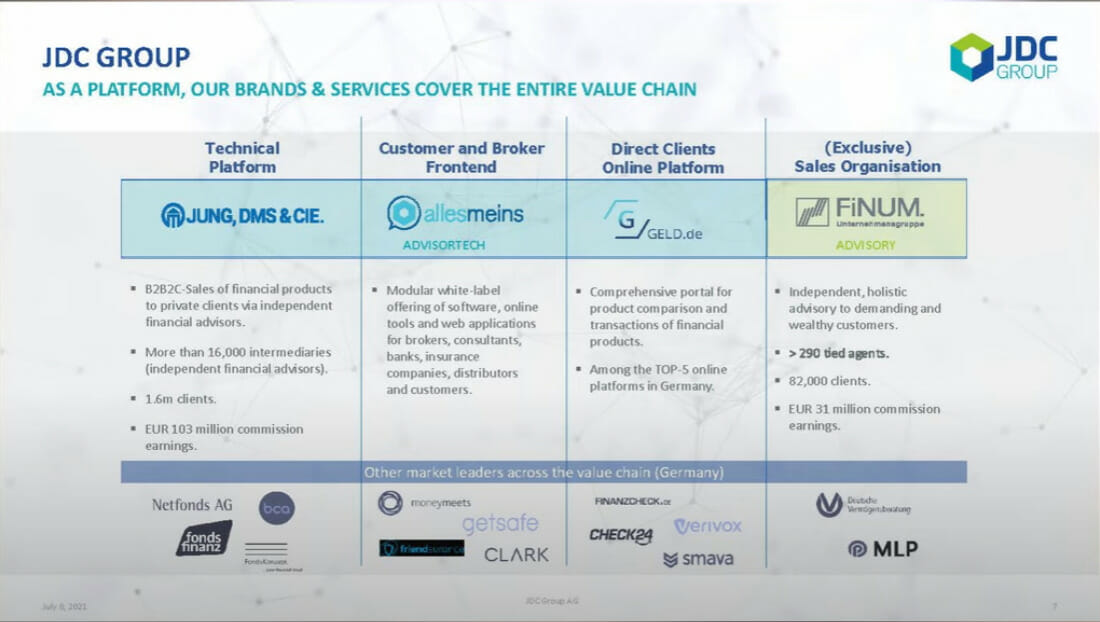

[00:15:38] Sebastian Grabmaier: So let’s say, you are a bank or there is a broker. There are hundreds of IT programmes out there, but we are solution providers. That means, with us, a customer gets IT plus data plus processes. And all these three together make sense for the customers because we want, let’s say, plug and play, with one plug, with one contact with us, that for a broker is two pages long. You can access all of our tools and all of the financial products in the German market.

So let’s say, you are a bank or there is a broker. There are hundreds of IT programmes out there, but we are solution providers. That means, with us, a customer gets IT plus data plus processes. And all these three together make sense for the customers because we want, let’s say, plug and play, with one plug, with one contact with us, that for a broker is two pages long. You can access all of our tools and all of the financial products in the German market.

So there are more than 18,000 products of almost 1000 product providers, and this is a solution that encompasses all kinds of legal and data protection and compliance things you wouldn’t think of at the beginning, but we do this in the highest industry standard, which is an app for banks, insurance companies, and all kinds of corporates. So our customers are Lufthansa, Volkswagen, and BMW and therefore we have the highest data protection levels or information security levels. And this is something that doesn’t come naturally. If you look at a broker customer relationship tool.

So there are more than 18,000 products of almost 1000 product providers, and this is a solution that encompasses all kinds of legal and data protection and compliance things you wouldn’t think of at the beginning, but we do this in the highest industry standard, which is an app for banks, insurance companies, and all kinds of corporates. So our customers are Lufthansa, Volkswagen, and BMW and therefore we have the highest data protection levels or information security levels. And this is something that doesn’t come naturally. If you look at a broker customer relationship tool.

The B2B2C model

[00:16:49] Tilman Versch: But you also have these other business lines like geld.de, money.de to translate it. It’s a direct-to-customer. So you have B2B to C businesses and you have D2C business? Or is there anything I missed?

[00:17:07] Sebastian Grabmaier: Yeah, so the B2C business is less than 2% or 2 1/2% of our P&L. So we bought geld.de, so you know like money UK like insurance supermarket. We bought it as a contract portfolio. We just got the platform on top, but we use this by integrating all these end customer tools into our platform offering our B2B clients better use for their end clients. So we’re not marketing our platform to retail customers, but contrary to this, we use the tools that we bought, integrated them into our B2B platform, and now we are on a B2B2C model only. So if you want to grow, let’s put it the other one, if you can spend a lot on TV ads or Google ads and then you can acquire customers very expensive. So it’s about 120 to €250 a customer, so that has to, let’s say, amortise over the years or you can buy portfolios. Or which is our way you can just get the customer for free by cooperating with a number of intermediaries that then you have to split up the commission with and that’s our model. We don’t use our money to acquire customers, but then we rather share our revenue with our intermediaries and that’s for us the cheapest way to grow.

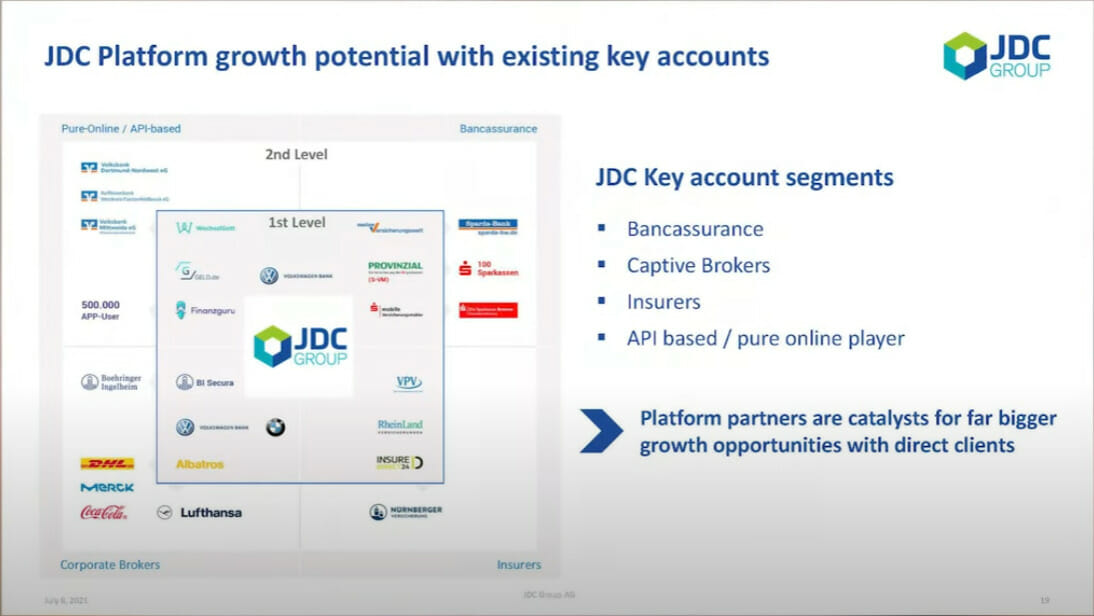

[00:18:37] Tilman Versch: You have another nice chart in your presentation that shows a bit of positioning between the different customer groups. So what kind of in the value chain? Where are you positioned with your services and where do they take place to run the machine?

[00:18:53] Sebastian Grabmaier: We are a classical platform business like in the platform economy. So we link the product providers with the retail customers and then whoever owns customers is our most preferred client. And we looked at the list of people or companies that have the most clients in Germany, the most clients are sitting with the savings banks. It’s by far the biggest banking group in Germany as you know but maybe the people abroad would not know, so they have fixed them.

[00:19:21] Tilman Versch: Sparkasse and folks spanking as German say.

[00:19:24] Sebastian Grabmaier: Yeah, that’s right. To the Sparkasse, the savings banks have five zero, 50 million Germans as customers and the Folks bank have 30 million. These three zero million Germans as customers, so together, theoretically, if you have these two groups as customers, you can present your platform to every single German customer in the market and that’s where we started out. And as you might know, there might be a question in this, we now want the savings banking group as a customer, and we also want the corporative banking group as a customer by attracting the insurance companies behind these groups to become our customers. But then we will still add customers from the corporate side or the insurance private insurance side on top.

Difficulty in comparing insurance companies

[00:20:10] Tilman Versch: I have done this insurance comparison and if you think about the platform, it’s hard to do an insurance comparison well because insurance is especially like a house, that position, I think it’s the protection of the things you own. There are so many levels you have to get right. So how as a platform, your job is to standardise these kinds of products, and a lot of still like you said, legacy systems are not standardised. So how much work was it to standardise this and get this workflow that makes things more productive than just making everybody mad?

[00:20:47] Sebastian Grabmaier: That’s a very good point because other than on the security side or investment, there is no morning star S&P delivering data. So the only ones who have the data are the insurance companies. And then that’s our first task to standardise all the data and make it comparable both on the product side and on the individual contract side, because there are some things that are only known to you as a customer, like your health conditions and the insurers. So we need the insurers to deliver data.

Then we have to validate the data because especially on the product side, some insurers tend to cheat. So they have the product in their window a little bit better than it is. So we have about 20 mathematicians that recalculate the tariffs. So we get a real comparison on the tariff and this also what we’re standardising and showing the customers a real comparison of the real facts of the contracts and this we make really easy and very easy to use like you get just an overview and the rating on every product and then with some clicks as we have all your data in our system, you can have a comparison under your individual risk facts.

Onboarding insurance products

[00:22:05] Tilman Versch: Is there a certain data flywheel you’re having when onboarding new contracts or Nuernberger physician is, for instance, launching a new health insurance contract and they ask you to evaluate it and onboard it? Is getting better your system over time?

[00:22:22] Sebastian Grabmaier: Definitely because like the 10 leading insurers already use our, that’s our subsidiary Morgen & Morgen, they used them before they launch a product in the market and at the end of the designing phase of the product, they asked us to compare the products with all others because when they bring it, you want to be among the top three products in this product line. So if you are not, you can just stop launching because it makes no use because nobody buys it. So people would just use the comparison calculators and just buy the top products of the best providers, and this is how the sales cycle works and so we start to deliver benefits of our data pool very early in the product design phase instead of just having existing products in our tools.

Project cycles in insurance

[00:23:16] Tilman Versch: Walk me a bit through the sales dance you do when you try to onboard new customers and win them for the platform. So how is it arranged? How long does it usually take till you’re dancing together and not apart?

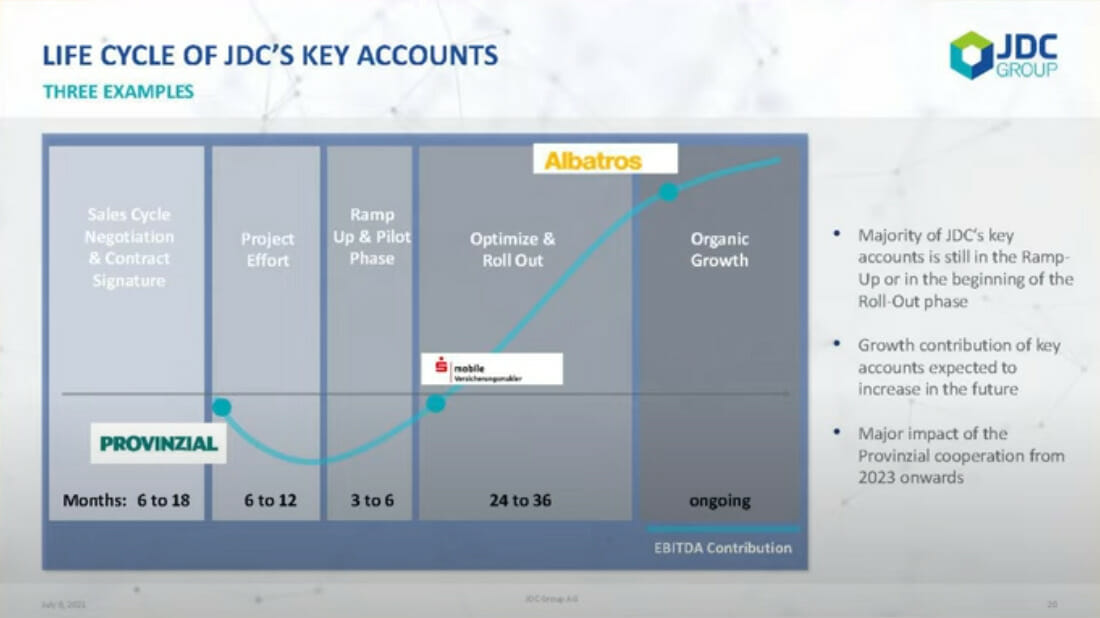

[00:23:30] Sebastian Grabmaier: So most projects start with a real tender. So the big institutions, the big insurance companies, they asked the entire market to issue offers and until now, interesting enough, we want every single tender of these big institutions by going through all these phases and then having the decision taken on the worldwide holding board, Lufthansa for example, you go to the worldwide holding board twice. You go up like in doing the tender office then you get the departments of Lufthansa check, whatever, the legal, the data protection, the compliance side and then you are up for the decision the second time.

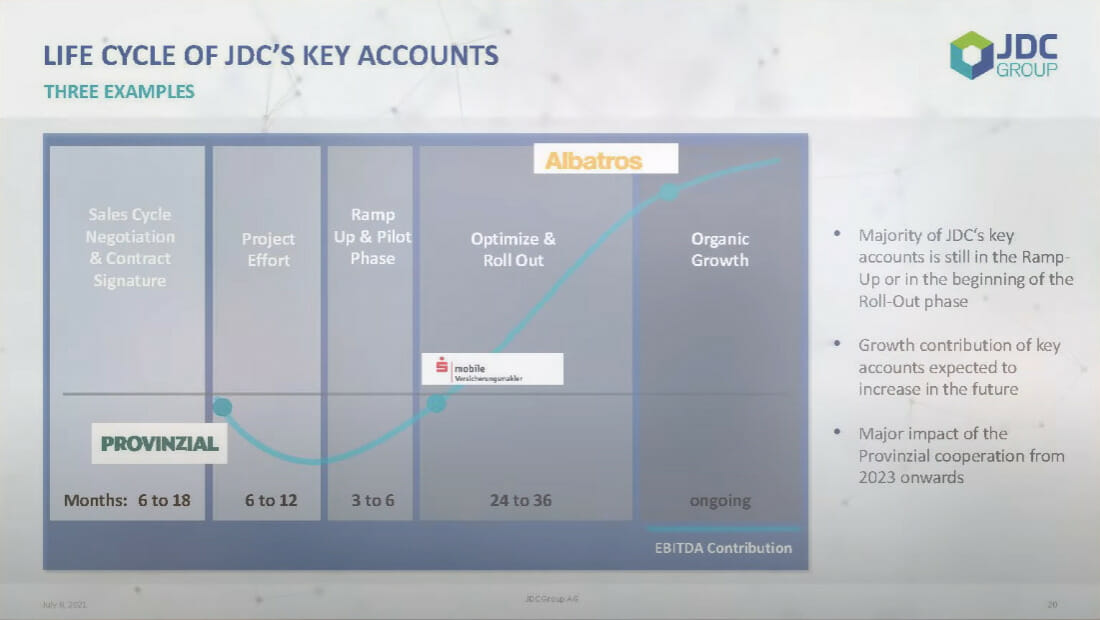

So this circle normally takes up to 2 ½ years. On average, it’s no project is much faster than 12 months. So the sales cycle until you have a natural organically growing business of this very big client just starts after three years. So from our very big clients, only the first two or three are in an organic growth phase and all others are still in the ramp-up, roll-up phase.

[00:24:39] Tilman Versch: You have a lot of cost with this on your side, so how much does it take to do the sales well and cost-efficient?

[00:24:49] Sebastian Grabmaier: So there are more than 60 people working on these onboarding projects. So it’s a huge task to talk to all these departments of these very big organisations and answer their questions right. So this is the cost that we have now, knowing that the turnover and the earnings will come 2 ½, three years later. So if you look at the first set of 80 savings banks coming with our first Provinzial projects after now 2 ½ years, we’re just onboarding the savings banks knowing that the conversion of clients only comes after, and earnings come even after that. So the real impact on our P&L will be four years after starting the contract and into the projects. But on the other end, you can imagine if you have these hundreds of banking institutions on your platform with thousands or even millions of contracts, then it’s very hard to leave. So it’s a very stable business once you have it, but you know the downside is that to acquire it, it’s quite some effort.

Sebastian Grabmaier on the saving banks

[00:25:51] Tilman Versch: Maybe let’s talk a bit about the world of the Sparkassen. It is a bit like you said on your slide about your one hundred Sparkassen saving banks and Sparkassen. They look united but honestly from my experience at are small like landlords who listen to him as the Germans saying that they sit in different regions, they own the regions and if the boss isn’t really satisfied, he doesn’t do what the central organisation does. How you’re going about these tensions to like it’s 100 Sparkassen, but is it like you can do business with all of them? And how is the implementation done with all of the small rulers?

[00:26:36] Sebastian Grabmaier: That’s a very good point. So indeed. The individual savings banking institution in the field makes a decision on what process platform to use. But they are all combined in associations and also the public insurance or the insurers behind these savings banking associations have some say in the way they decide because a lot of business now comes from the insurers, behind these savings banking associations. For example, like now, our first client is the Provinzial insurance company that just merged. So Provinzial has or is the home delivery or the home product provider for about 110 of these savings banks in Western and Northern Germany.

And then there are positions come up by BKB that has about 90 savings banks in the South of Germany. And then the list goes down on all these public insurances because they provide sales support within the branches of the savings banking groups. So our way was to attract the very big public insurance behind the savings banks that have about 300 of these 370 banking institutions and come to the door of the established sales channel of the sales insurance sales specialists in the branches. That was our way to attract these savings banks instead of going from one door to the other of these savings banks in the villages.

Where they earn money

[00:28:01] Tilman Versch: Give me a bit more details on how you earn money with your customers. As you said, you have many small cash flows, where are they coming from?

[00:28:10] Sebastian Grabmaier: So if you look at your insurance portfolio, you would not know that, indeed, you have more than seven or eight insurance products in place. First, you think that your building or household, but then you have a car, you might have a boat, you have a bicycle, you have travel insurance, you have accident insurance or disability insurance. So a normal German has seven to eight insurance products. And each of them, on average, pays €35 and we take in these commission streams and then we normally take up to 25% stays with the platform, we pay out 75% to the intermediaries and this is how the money comes in. Once we transfer your contract, your platform, which we can do by reading out your bank account and then just transfer it with two clicks. Then at the next due date, we get the commission, and this is how we earn these, whatever, €7, €8 on each of these contracts that you own as a customer. So in the end, we collect all these little euro bills and then we deduct our 25% and we send the rest to our intermediaries.

So if you look at your insurance portfolio, you would not know that, indeed, you have more than seven or eight insurance products in place. First, you think that your building or household, but then you have a car, you might have a boat, you have a bicycle, you have travel insurance, you have accident insurance or disability insurance. So a normal German has seven to eight insurance products. And each of them, on average, pays €35 and we take in these commission streams and then we normally take up to 25% stays with the platform, we pay out 75% to the intermediaries and this is how the money comes in. Once we transfer your contract, your platform, which we can do by reading out your bank account and then just transfer it with two clicks. Then at the next due date, we get the commission, and this is how we earn these, whatever, €7, €8 on each of these contracts that you own as a customer. So in the end, we collect all these little euro bills and then we deduct our 25% and we send the rest to our intermediaries.

[00:29:16] Tilman Versch: A friend of mine who is also working in the industry talked at the podcast and he said he thinks you are slightly a bit more expensive on this side with the service you are offering. What would you say in comparison to the service of others?

[00:29:30] Sebastian Grabmaier: Well, it depends on what the range of services is. So execution only is the business we like best. So we’re just taking the data and we throw it out in our systems or by an API structure to the systems of our clients. We are quite cheap, we’re rather speaking about 10% to 12% of this commission base. So I think there’s nobody can do it better and cheaper. But what we do is we add on services if the client wants them. We do full outsourcing, so we staff the call centres and do all the communication around the contract and then our margin goes up to 30% where we do everything for the clients and that’s more expensive because there are real human beings who have to pick up the phone and it’s not digital only, but in a pureplay which we can offer, I think nobody is cheaper for the performance we deliver.

Well, it depends on what the range of services is. So execution only is the business we like best. So we’re just taking the data and we throw it out in our systems or by an API structure to the systems of our clients. We are quite cheap, we’re rather speaking about 10% to 12% of this commission base. So I think there’s nobody can do it better and cheaper. But what we do is we add on services if the client wants them. We do full outsourcing, so we staff the call centres and do all the communication around the contract and then our margin goes up to 30% where we do everything for the clients and that’s more expensive because there are real human beings who have to pick up the phone and it’s not digital only, but in a pureplay which we can offer, I think nobody is cheaper for the performance we deliver.

[00:30:29] Tilman Versch: Let me follow up a bit on the question on how you earn money, and you have this nice slide again in your presentation and can you walk me a bit through this and explain how long does it take to get a customer fully profitable? Or even maybe also then upsell from basic services?

[00:30:49] Sebastian Grabmaier: Well, it can be very quick because the system is ready. It’s paid for and it’s by an API structure. You can very easily introduce it into your system. So a very good example is the Sparkassen agreement. They wanted to change their provider and after six weeks they were up and running on our system. If you use our standard system. The other example is Provinzial, who had a huge list of specifications for the platform and did a tender. After the tender, they did a merger and then they did a new tender and then they did a pilot and then only after 2 ½ years they started the project by founding a joint venture company and only now are rolling up the individual savings bank. So now, we are three years into the project and just are still in the ramp-up phase. So it depends on how big the project is. But then as you might have read, also Provinzial wants to provide one million clients to the platform, and you can imagine that huge projects like this. They take longer time compared to just starting with the new business the next day.

Maintenance costs of the infrastructure

[00:31:57] Tilman Versch: How big is your yearly cost to keep the system maintained, like with maintenance and also does it mean that it keeps running reliably, but it also stays state of the art?

[00:32:07] Sebastian Grabmaier: So our IT cost, so we now have almost a hundred people in IT and IT architecture, so IT costs it’s about €7 million and half of it goes into just running the system. So you have to maintain servers and data quality. It’s about three and a half million, and we have another like the pure development is maybe three to four million of development of the tech stack and the interesting, you have the rest of the cost is a lot of processing and taking the data, data standardisation and just servicing the contracts.

So our IT cost, we now have almost a hundred people in IT and IT architecture, so IT costs it’s about €7 million and half of it goes into just running the system. So you have to maintain servers and data quality. It’s about three and a half million, and we have another like the pure development is maybe three to four million of development of the tech stack and the interesting, you have the rest of the cost is a lot of processing and taking the data, data standardisation and just servicing the contracts.

Room to grow

[00:32:44] Tilman Versch: Where do you see the best chance to grow with the customers in the future?

[00:32:49] Sebastian Grabmaier: Well, I think it’s these very big customers. They quite take a little bit of time to take them on, but once the system is up and running and that is what we can see now, the first big clients we are onboarding like Lufthansa, Albatros or Bavaria, BMW or Rhineland. We can see that, and we can grow organically because we’re improving their business. You know we’re teaching them how to do campaigns with their clients, and how to service them better to avoid churn. So the people are happy with the platform adding new contracts, upselling the contracts, and cross-selling them. So there are a lot of ways. So once you have the clients improve their business and then grow with them.

[00:33:33] Tilman Versch: So there’s also this element where you onboard a client and make him better?

[00:33:39] Sebastian Grabmaier: Yes, definitely. So we grow in three ways. One is attracting new clients. The second is like aggregating more business and having more shares of wallet. So not only get different individual business lines but get all of their business. And the third is, in the same business lines to improve their business by being more efficient for the people. For example, have fewer inbound calls because there are more digital services, and they can be used to service their clients better.

Improving with a client

[00:34:07] Tilman Versch: Can you maybe walk me a bit through what this could mean for a client of yours if you make them better?

[00:34:15] Sebastian Grabmaier: Well, if let’s say you are Albatros, Lufthansa, so a lot of time for your employees goes by receiving the letters, opening them, reading them, putting them in classifiers in the closet. This can all be saved because the data comes completely digital into your systems, not only for the client but also for your internal departments that have to process all these insurance workflows. So Lufthansa, for example, could reuse almost forty of their employees to put in their client service department where they could service the real client need instead of only pushing paper. So you save about 30% of the cost by digitising the paper processes and this is what you can use if, well, you can just save it, but if you can reuse the people that are specialists in the market in outbound calls to the clients and explain them more about how they could improve their portfolio. You have got a double impact and have much better customer relationships and much more benefits for our customers.

Comdirect

[00:35:22] Tilman Versch: Instead once customers are on the platform, it’s hard for them to leave, but I think in 2021, Comdirect has left you, why?

[00:35:34] Sebastian Grabmaier: Well, Comdirect just ceased to exist by being merged into their mother company. So obviously, Commerzbank had some financial trouble and Comdirect, their direct bank, was working very well. Actually, the same week that we had Comdirect, the merger was published. And now Comdirect is just not existing anymore. So it’s not that they were not content with the system or with their plan to digitise the business. Interestingly enough, most retail customers we lose because they just die. Almost 2% of our customers die every year, which are very sad fact, not only because it’s a personal tragedy sometimes. But it’s the contract and ceases to exist. Your life insurance, your health insurance just ends when you’re not living anymore. So the non-existence of a customer is a hard point we have to accept but as most of our customers are companies, they have a long life. But Comdirect, unfortunately, doesn’t exist anymore.

Reasons for losing customers or change of contracts

[00:36:40] Tilman Versch: Yeah, what is the second and the third reason that you lose a contract?

[00:36:45] Sebastian Grabmaier: At least not a bigger contract. We haven’t lost one until now. So there’s one exception.

[00:36:54] Tilman Versch: And on the customer level? I meant with the contract. Sorry, my question wasn’t super precise. After people die?

[00:37:02] Sebastian Grabmaier: So for example, if you change your asset like if you sell your car, normally, you seize your car insurance and then you take out another and different types of contracts with a car, it sometimes goes with the car dealer. Or you just start from scratch because it’s very money sensitive and you take another point of sale. So car insurance is the type of insurance we don’t like, we most dislike it because the normal duration is only 3 ½ years. And number two, pets. For example, because they only live for seven to eight years on average and then everything else, household, building, that’s very nice because that’s normally 14 years plus. So we like long-running contracts.

Tenders

[00:37:55] Tilman Versch: You mentioned the tenders you’re running or you’re applying to. Who else is also running for these tenders and who also often gets the song as German say? Or just like doesn’t win it?

[00:38:11] Sebastian Grabmaier: I can talk about it because they published it themselves. It’s a very good company called Hyper Port, that had some maybe some downturn. So they ended up very good second, a lot of times now, but it’s a company that we like because they started a little bit earlier than us on the mortgage side, and then there are two companies that also started as broker pools or you might have read a Form Finance because they were just bought by Hg Capital. So they will be there eventually and there might be some competition somewhere down the road.

[00:38:51] Tilman Versch: Imagine you have a new person coming from university who is also set to work on the tenders and to scan the insurance industry for tenders. What would the advice to this new person, say it doesn’t make sense to look for tenders there because we have a really bad chance to win them or there’s already a competitor who’s taking the position? Is there any part of the insurance industry like this where you would say it doesn’t make sense to allocate time for the tenders?

[00:39:26] Sebastian Grabmaier: Well, it’s just a volume play in the end. So the bigger the customers are, the more sense it is to follow up on the tender because there is some effort with it. So, this why we’re focusing on the very big tenders and then down the road if you are– well sometimes you have individual brokers that are quite some hassles to onboard because they look at 10 different platforms and ask you a hundred questions and then they just send you four contracts a year. This is not what we are specialising in. We love this because we have 16,000 of these individual brokers. We love many of them, but we are more focused on the ones who send more than 10 orders a year. So the bigger the clients are, the better they suit our systems.

Having a platform that stands out

[00:40:11] Tilman Versch: Let’s take another slide I’ve prepared. Look at your system or platform, what are the ingredients that make this platform you’ve built better than other platforms and other technical offerings?

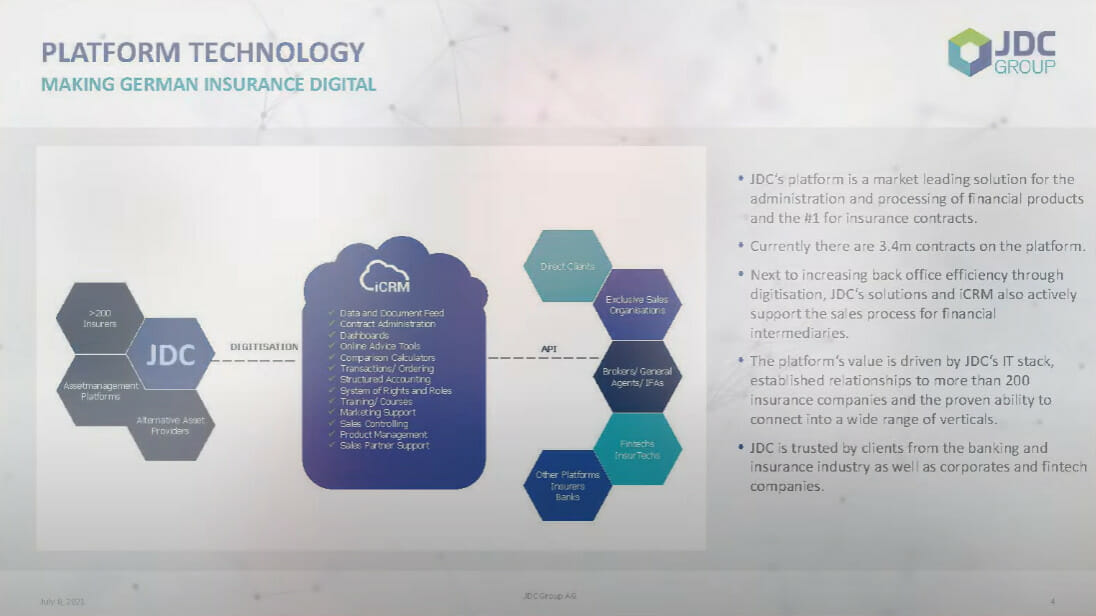

[00:40:31] Sebastian Grabmaier: So I like this slide because it explains the business model best. So as I said, we started as a marketing and product platform. But what it means today is that you are a data processor. So our core task every day is to take in all the data of 220 insurance groups, all the alternatives and the estimated platforms, the alternative product providers, the mortgaging bank, so we’re taking the data, we standardise it, we process it, and then we throw the data out to different visualising systems either our own or the systems of our clients.

So as I said, we started as a marketing and product platform. But what it means today is that you are a data processor. So our core task every day is to take in all the data of 220 insurance groups, all the alternatives and the estimated platforms, the alternative product providers, the mortgaging bank, so we’re taking the data, we standardise it, we process it, and then we throw the data out to different visualising systems either our own or the systems of our clients.

So I think about Amazon for financial products. That’s exactly what we do. And there is no data standard, so we have to, as I said before, you have to get the data from the individual product providers and then you do a lot with the data. You show the contract data, I show your data as a customer. Then I show you all the documents behind the product. So you have the entire things that are piling up on your kitchen table, normally, you just can bring the bin and then use your little app or website to have all this information out of your contract. So that’s rather a platform business today than a sales company that you might imagine.

Thought experiment on Amazon

[00:41:56] Tilman Versch: You mentioned Amazon already, so I take the example because some investors in the US think Amazon will enter the insurance market with all the data they have. So let’s say Amazon, they have a lot of money, they have technical capabilities, but how long would it take for them to replicate something you have built?

[00:42:17] Sebastian Grabmaier: Well, the first thing they need is the entire contract for every individual insurance company. One, for the data; and the second, as a sales and as broker intermediate. So, that’s a lot of running around. Then they have to reprogram the platform we build, and then you have to do it right. So the chances this is happening and is not big. So for them, it would be way cheaper to take participation, for example, in JDC than to start on their own. And now we have programmed this platform for the last 10 years, I think it’s a very high hurdle for them to enter the market now.

Well, the first thing they need is the entire contract for every individual insurance company. One, for the data; and the second, as a sales and as broker intermediate. So, that’s a lot of running around. Then they have to reprogram the platform we build, and then you have to do it right. So the chances this is happening and is not big. So for them, it would be way cheaper to take participation, for example, in JDC than to start on their own. And now we have programmed this platform for the last 10 years, I think it’s a very high hurdle for them to enter the market now.

[00:43:04] Tilman Versch: How much trust does a competitor, not only Amazon, need to be able to get all this data in the insurance industry and how long does it take to build the trust that you are accepted as a player?

[00:43:19] Sebastian Grabmaier: Well, quite a bit, because you have to give them business also, right? So why would why Allianz transfer contracts to our platform? Only because they know that the customer service is better when they’re both digital and personal, and then that the churn rate is lower or the retention of the customers higher once it’s on a platform. So this is the only reason why an insurance company would give me their client and if you cannot show them that you’re good for the client and you have a lower turn, then it just wouldn’t do it. So if just enter the market and I want to aggregate the contract just to do something, move them into other industries or other products, then this will not happen. So yeah, but it’s very typical for business not only about the retail clients or intermediaries, but it’s also about the trust of product providers.

The data flywheel?

[00:44:12] Tilman Versch: Let’s go five years back and think about the quality of your processes and like the speed, where have you gotten better, also with more data and where has your flywheel gotten better on the platform?

[00:44:26] Sebastian Grabmaier: So the first milestone client was Lufthansa Albatros and they transferred 400,000 contracts of these 120,000 Lufthansa employees. And first, there was an individualization list for our platform. There were like 95 points on it which made us reprogram the platform quite a bit and they had completely different standards for information security or data protection and also documentation. So we reinvented the platform to make it industrial and make it in their banking or air travel standard and saying what Lufthansa says, well, we are an airline, so it’s not a 99.9% system but it’s 100% system. So our data quality and our processes are– I know you cannot compare it how it was when we just did it for individual brokers

[00:45:22] Tilman Versch: Are there other parts where you’ve gotten better with your systems over time?

[00:45:27] Sebastian Grabmaier: What we’re measuring is the rate of contracts or processes. We just do it automatically. So the things we do not use human beings to process and our rate is now by more than 85% which is good news because it started at zero and now most of our processes are automatized but still, we have 15% of processes that we need someone to look at. So whether the data is right, whether the fill-ins of our brokers are in the contracts. We try to become more and more efficient and, in the end, to put in numbers we can reuse about 20 to 25 employees, about 5% or more than 5% of our employee base and can bring them to more service and customer-oriented task because we just have the machine learn to do their job.

[00:46:31] Tilman Versch: Is there anything you might need to grow, the workforce, to do future business better?

[00:46:40] Sebastian Grabmaier: Yeah, that’s what we said. If we do execution only like low margin but a highly automatized business that we like, that we can charge about 12% or 10% of the margin, the costs are very low, it’s about 2 percentage points. For example, if we take in these one million contracts of Provinzial, for these, with a hundred million of turnover, then margins only 12 million but there are only two million costs. So you hardly need anyone to support the process teams. But then on the other side, if we add, which we do with our joint venture Egypt Hall, EGV, add service components where we offer a call centre or service centres that answer emails, you will need up to a hundred new employees to staff these service centres and this is expensive because this costs up to 15 percentage points of your turnover and maybe you earn about three to four percentage points, so the earnings quality is much better in this execution only models.

Digitalisation

[00:47:51] Tilman Versch: Let’s jump a bit to the level of your market, the insurance market. How digital is the market? In your way to rate it, maybe 10 is super digital and one is like all is done by paper and fax.

[00:48:05] Sebastian Grabmaier: Maybe three. There is a long way to go and even if we are fast, our market share is like .5%. There are a lot of ways to grow and it’s a platform like ours that will grow. It’s very fast to like normal levels of market shares but the insurers themselves, for them, it would be a very long way to digitise.

[00:48:30] Tilman Versch: Has the speed of digitization changed over the last years? Got it faster this transformation up from two to three?

[00:48:41] Sebastian Grabmaier: Well, COVID was a catalyst for digitization of the market, because until then a lot of people had the opinion, no, the customers want to see an intermediary and this has to be all in person. That’s not true. More than half of all customers like digital and do not want to see a sales rep in their living room. So in their view, up to 80, 85% of all business can be done digitally. So this was a wakeup call for many board members who would have said, well, you know my contract is another five years in this board and I will survive this with not re-changing the entire company because it’s not only a change of processes, it’s a huge culture change to not ask the client for data, but get the data where it is with the insurance companies. So this remodels many of the ways to do business with an insurance company.

Community Exclusive: Impacts of the pandemic

[00:49:34] Tilman Versch: Let’s maybe go back again to this slide a bit, because COVID, like I think 2020, most people were busy with just managing the pandemic somehow, and maybe at the end of 2010, they started to make decisions towards more digitization or how do you see the timeline here and also with like your two to three years’ timeframe of onboarding and stuff like this?

Hey, Tilman, here. I’m sure you’re curious about the answer to this question, but this answer is exclusive to the members of my community, Good Investing Plus. Good Investing Plus is the place where we help each other to get better as investor day by day. If you are an ambitious long-term-oriented investor that likes to share, please apply for Good Investing Plus. Just go to good-investing.net/plus. You can also find this link in the show notes. I am waiting for your application and without further ado, let’s go back to the conversation.

Addressing customer needs

[00:50:37] Tilman Versch: You also have to win the brokers or the broker pools. It’s like the insurance business. The customer relationship is your thing. You want to have your fingers on and control it and don’t give the emails of the customers out so that another person can message them and try to get them away, so digitalization leads to a certain transparency and the platform. There’s also we see with Amazon that the platforms can play foul there. And the smaller businesses can lose ownership of the customer data. How do you go about this tension?

[00:51:15] Sebastian Grabmaier: Well, 80% of your needs is a customer, a quite standard. You have one car with standard car insurance, you have a house. Well, that’s more individual, but in the end, it’s all about size and square metres. So you can do it electronically and insurance intermediaries should concentrate on this field that is very digital. Your personal pension planning, your life planning, maybe you want to do a sabbatical, or you want to have your fourth kid, and this is where it’s worth spending time between the client and the intermediary to talk about these important things.

But 80% of all talks and time is wasted talking about your car, household, whatever, or building insurance that’s just standard and can be done with a small number of clicks. And this is what we do, your data, with your client with the platform, your data is already completely sitting in the system, and we don’t have to ask you for all these whether you own pets or how many kids you have, how much size you need. So this is all in the system already, so it’s just with like one or two more data points. In about four minutes, I can reinsure your car. Over two minutes, I can reinsure your household. So it’s very efficient and I can spend my time with you as a client just talking about the things that move you and where you’re different to all other clients.

[00:52:35] Tilman Versch: Maybe walk me a bit through if you have a customer-facing insurance broker and their client comes and says, hello, I want to become your new client. What is on the customer-facing side happening with your systems involved? So Dieter Muller comes and wants a new insurance relationship with the advisor.

[00:52:55] Sebastian Grabmaier: Yeah, so there are two ways of customers. One is Dieter Muller comes to me and says, I bought this new car, I wanted to be insured and I have three minutes. So that’s number one. That’s easy. But then people come to you and said, well, I don’t want to have anything to do with all this paperwork. I don’t understand it really. I do not want to spend time. Help me with organising it. And then we say well, just let me read out here, sign me a broker proxy, let me read out your account. Here, I show you within a very short time, after two minutes, I can tell you how many insurance premiums you pay out of your account, and then you were aware of the customer for the first time, how many insurance contracts you have because obviously, they are paid at certain different time periods.

Most customers have no clue how many contracts they have. So for the first time as a customer, Mr Mueller has a full view of his insurance portfolio. Most of the time he has two or three accident insurance because not only his best friend but also his brother-in-law sold him one of his three different life insurance products that don’t fit together and maybe he doesn’t have disability insurance or liability insurance which he needs. So with dim norms or with a group of German scientists and industry they issued standards for how he should be insured at this point of age, and so he gets a comparison of what he already has and what he should have and so at some points he’s double and three times insured and there’s a gap, so very easy.

I can show him what he should have in his product portfolio and then can take out with some more clicks, take out new insurance or cancel insurance which is double insurance, or three times insured and after a process of between 25 and 45 minutes, the customer is very happy to have it all clear and very transparent. And as we give our customers also these comparison tools, you can even check whether he has the best insurance and the best price-performance relationship. And this makes very, very happy clients that whenever they have a problem in their financial or insurance world, they come to me as an intermediary and use me as their number one intermediary.

So with dim norms or with a group of German scientists and industry they issued standards for how he should be insured at this point of age, and so he gets a comparison of what he already has and what he should have and so at some points he’s double and three times insured and there’s a gap, so very easy. I can show him what he should have in his product portfolio and then can take out with some more clicks, take out new insurance or cancel insurance which is double insurance, or three times insured and after a process of between 25 and 45 minutes, the customer is very happy to have it all clear and very transparent. And as we give our customers also these comparison tools, you can even check whether he has the best insurance and the best price-performance relationship. And this makes very, very happy clients that whenever they have a problem in their financial or insurance world, they come to me as an intermediary and use me as their number one intermediary.

Demographic shift within the broker industry

[00:55:16] Tilman Versch: Let’s also look a bit at the broker side, the insurance broker side and the insurance broker market. I think the demographic clip you have in Germany, there’s a demographic Kenyan because I think 40% of the insurance contract 140 million will have to look for a new advisor because a lot of the advisors retire. It’s quite an old cohort that has customers in their age group as well a lot, but a lot of these people will retire and their insurance mandates will look for new advisors. So what do you think about this as a chance for you and what does this demographic shift mean for you?

[00:55:55] Sebastian Grabmaier: Yeah, as you say that there will be much more market for the individual intermediary. So on the broker side, it’s even worse though every second broker will go out of the market. So he cannot really do it non-digital because they do what they do and they are very full-time working on the clients they have but they will be the double number of clients and therefore contracts on the individual broker. So the only way to cope with this development is to become more efficient in their daily work.

And instead of using 60 to 80% of my time as a broker to do all this administrative stuff, to reduce this to maybe 30 to 40% and for the rest and do value creative stuff and talk to clients. And also, we will see more aggregation, so there will be bigger brokers like partnerships or big brokerage houses, and they need different tools because they have they need workflow management and become modern companies. So democracy alone is will be a huge driver for digitization in this field. And then if you look at environmental arguments, it’s crazy that in your household half of the correspondence, half of the letters is pepper, and is insurance papers. It’s insurance change of contract or information to you as a client, so we can save tonnes and tonnes of paper and the energy or this fuel in the mail trucks and if we use digital tools.

[00:57:28] Tilman Versch: So if there is an issue with a lot of brokers going out of business, it means that also like the other brokers have to pay more and maybe after the drought there comes the flood and the cyclicality of the markets. Do you think that many more young people will then enter the broker space, or do you think it’s hard to get young people into the space?

[00:57:54] Sebastian Grabmaier: It’s not attractive at all for a young person to get in this paper closet room of their parents maybe who are brokers and look how they do business, but we see that if we fully digitise the business then and the insurance broker is a very nice job because you talk a lot of people. And you have real need of the clients that are very grateful. And it’s a very clean and valuable creative job. But still, there is the old picture of someone sitting in a paper crowd, overcrowded room with a lot of boring work and this is not attractive. This is the reason why there is a drought because young people choose to work for many companies, but not for an insurance agent or broker.

Example of Deka

[00:58:42] Tilman Versch: I’m jumping a bit back now to the Sparkassen because I got this idea of the so-called direct for the direct sale of funds. For instance, Deka funds and stuff like this. With your tools, it is a global comparison you’re doing. You’re providing for the service providers and not as like that certain product of focus that is in-house products that they want to sell, especially.

[00:59:07] Sebastian Grabmaier: Deka is a very good example. So 20 years ago, a savings bank would offer Deka only, so just one product line and with one product provider. Today, if you’re going to savings banks, you can buy every single fund that has an eye worldwide with your savings bank’s portal. So very modern, and well-developed, and that’s what I expect as a client I have a modern partner and advisor in my financial advice. Funny enough, if they go to an insurance site, there’s only one product on the shelf. How can this be? it’s very easy to say the reason why savings banks are having third-party products is because at the point of sale, they’re selling more and have more trust of the retail clients.

In the end, the business volume is much more to a point where even Deka is benefiting because in absolute terms, even if there’s now sell maybe only 80% of products sold in savings banks in Deka, the absolute number of fund transactions with Deka is higher than before because there are more customers using the savings banks as their portal for the investment side. And the same will happen on the insurance side when they allow third-party businesses so and have the customers see their third-party products then there will be more volume of insurance business done in the savings bank branches. In the end, savings banks will place more business for Provinzial or VKB and all these other insurance companies. So it’s a very natural thing in benefiting, you know, benefit for all market participants.

Choosing a specialized broker

[01:00:52] Tilman Versch: It also helps Sparkasse to win back their customers that have left because the offering wasn’t like specially tailored, IF left then and went to a special broker because it was more in my interest to get a better selection than Sparkasse had.

[01:01:06] Sebastian Grabmaier: I’m a good example also, I’m a Savings Bank customer. You remember these trucks, the buses that would drive around in the elementary school and would give you a five marks credit if you open an account. So basically, that’s how they attracted their customer. And I went away with my investment business a lot to go to a specialised bank. But now I’m back because my accounts are with the Savings Banks and my credits are with the Savings Banks. It’s very convenient to do all my normal investment business on a Savings Banks platform that’s very modern and would be even more convenient. And this I think the strong strength of savings banks because in Germany, other than in other countries, once a week, people take their cash out of an ATM in a bank branch. So there’s real customer contact.

[01:01:54] Tilman Versch: You mentioned these big pools that are now general of insurance brokers and that need special tools for their needs like workflow management and stuff like this. Is this also something you’re thinking of as a business line, or is this out of focus, focus, focus as a platform?

[01:02:13] Sebastian Grabmaier: What happening now is that as the tech development is so expensive, there are platform businesses joining up with money, that’s private equity coming in, and some of the product providers to have these big market participants that will form like own platforms. And in our view, same as in other markets, there won’t be another what is like today there are maybe 30 broker pools. My belief is that as tech investments are becoming more challenging and also regulation investments are becoming more challenging, the number of these platforms will go down further. And they will have a full stack of services and products. And combined with money pots given by private equity companies, they will also heavily buy in the market so they will become relatively way bigger than the market participants today.

Germany within the European market

[01:03:10] Tilman Versch: We are mostly talking about the German market, at the moment, but there’s also Europe around. I’m not sure if there are many European countries that love insurance as the Germans do. But if you look at the different European markets and their dynamics, which market could be a kind of role model for you? What would be possible in Germany or might be like five or 10 years ahead of Germany?

[01:03:33] Sebastian Grabmaier: Well, we don’t believe it, but in this insurtech side, Germany is the market leader, so there’s no other company that has such so much digitization in the insurance industry as we do. So even if we are slow, let’s put it this way, other countries are much lower, so one of the markets is in Austria and we have some business in the Czech Republic, and Slovakia, so we can see that it is not as much. Maybe there are some Scandinavian countries that are more digital, but they are much slower. And if I speak to my international investors a lot, a lot of people like in Singapore or the US would say, wow, that’s fantastic. I would like to have this as a customer. So we could export the platform and we’ll do so after just grabbing all these low-hanging fruits here in Germany we start to expand whenever we find good management teams in different countries such as the Netherlands, and Switzerland. We’ll talk to these teams and then maybe acquire our smaller companies because there is no other insurance platform like this in Europe.

Expansion

[01:04:45] Tilman Versch: What is your playbook if you think about expansion, like how you’re going about the market, are you going like that there’s a pull from the market that pulling is pulling you in? Are you looking for the management teams just as you explained?

[01:05:00] Sebastian Grabmaier: Well, the easiest is to grow in Germany. So we have a .5% market share of all the insurance business in the markets and for us, it’s very easy to grow whatever two, three, four, five percent and why not 10% to grab like bite some chunk of the German market, and only with the contracts we already have savings banks and corporative banks and these other big customers, we will grow fast in Germany. But then if you find platform teams in neighbouring markets we would buy these small platforms and then expand from there.

Competition for JDC

[01:05:33] Tilman Versch: So on the international level, there’s no competitor you would, so to say “fear” that might be challenging for you that you’ve spotted?

[01:05:43] Sebastian Grabmaier: Well, we don’t know any and also the investors we have don’t know any that’s more advanced, so no, there is no big fear. There are always talks about when Google comes into the market, but why should they? So their insurance business is running perfectly but just selling ads, so why would they do the hassle to buy tech or to build up a tech platform? So I don’t believe that they are coming. So these talks are gone. Right now, it’s a very good market positioning for us because we are winning all these tenders, meaning we have the leading tech stack and this is what we can roll out in other European countries as soon as we are deep enough connected in the German market because now it’s all about getting all these big customers in Germany but then we will not stop but go abroad.

A look into the future

[01:06:28] Tilman Versch: Maybe let me ask you, what do you think your business will be in five years? So imagine we are having a chat again in 2027 and what will you tell me where you positioned and where you also lay the fruits today for being positioned in this matter?

[01:06:47] Sebastian Grabmaier: Well, if you look at developed platform markets. So it’s not rare that big platforms have 25, 30% of the market. So we know now, five years from now, we will be way bigger than we are now. So if we only take in the context, we already have savings banks and corporative banks. Again, all these big players, so it’s very easy to think that from this 250 million we once gave as a vision for 25, why should we not have 500 million in turnover? Earning about 50 to 60 million.

So you can see that once the platform scales up, it’s much easier to earn money. So now the platform is paid for it, there’s no Capex anymore needed to develop any further. So with the existing platform, it’s no problem to take in these volumes. And then it’s a very profitable company with a very nice valuation. And then you can like go away that Fidelity took in UK or Schwab and US to be one of the leading platforms and platform providers, process providers in this market. And then this can be big. So that’s still far out in their vision. But I think investors can see that step by step by step, we will execute on these back contexts. We will take in all these volumes and then they will see a growth of 20% plus year over year and this will bring to these huge volumes and I don’t see any reason why this should not happen. As we know, there are a lot of things, there are always waves in the market and there are terrible things like the Ukraine wars and inflation but over time like mid-term, the term and long term I have a very good prospect to this.

[01:08:21] Tilman Versch: Were you looking to protect to do a mistake or that something goes wrong on this journey? Is there anything you’re especially focused on not doing or not running into?

[01:08:36] Sebastian Grabmaier: Well, very high focus on data security and process security. So what’s the worst? What can happen? You know that now Russia hacks you and whatever it takes away, they steal your data. So I think that’s the worst and we have high standards of penetration tests and data security levels to avoid these cyber-attack worlds and lose the data because the rest I think you can see. We have a clean balance sheet. We are net cash. We have good cash flows. We have good customers, and it is very stable. It’s recurring. So I don’t see big risks on the business side as long as our machine is running and producing data.

[01:09:29] Tilman Versch: How much, if you think about the other markets, you’ve proven that you can do business in Germany, but European markets are also meant like markets in themselves or nations that have waived the build trust in a certain nation. What do you think about this? Like it’s easier to scale in the US if you have a common market with 300 million people or 400 million people. But in Europe it’s you have to take country by country, which brings you to a stronger position. Because if you once I’ve taken it, it’s harder for others to enter, but you have this national focus and this national trust, so to say. What do you think about this?

[01:10:05] Sebastian Grabmaier: The fun fact about the US is that insurance they’re also fragmented. So you have to go state by state, so you will start with the big state like New York and California, and then go state by state. And same applies here. Well, in a perfect world, Europe should be regulated level playing field, but you’re right, every market is different, and especially every individual system of insurance companies is different, so we would go to these markets and have individual contracts with the individual insurance companies and then do this acquisition work to then be able to start these platforms. But our platform, it’s existing in English and Czech and Slovakia, and for example, it’s very easy to now translate all these little text surfaces and it’s working for all insurance. We do this for Austria, basically. A lot of insurance turn actions, and that’s not a big problem. It’s rather on finding the management teams to run these individual platforms in the other markets.

The right management mindset

[01:11:13] Tilman Versch: Do the right management teams need to have to be right?

[01:11:19] Sebastian Grabmaier: They need this digital view on the industry because most people look at the industry and said if we digitise it, we just copy the paper processes into digital and that’s wrong. So digitization means our system just ping the data stream from an insurance provider. But with your name and the name you tell like your car insurance is with Allianz and under your name. Allianz is so nice with one signature on your smartphone to send me all your data. For example, on your car, under your name or all the cars. And it’s very easy. And if you realise that the data stream can be reversed and using the data word is, there’s a lot of efficiency gain there.

[01:12:09] Tilman Versch: We mentioned COVID. We mentioned the demographic change as some kind of tipping point that could go in your favour. Do you see other tipping points like this or structural changes that could go in your favour?

[01:12:23] Sebastian Grabmaier: Well, I think we have a lot of tailwinds by demography, as you mentioned, one; digitization, two; and then aggregation which is three. So that’s already a lot of tailwinds there. We’ll see what comes. We know that regulation is not a headwind. Because that’s, IDD me fit, that’s done. GDPR, data protection is done. So ESG is rather positive and negative, is some effort. But in the end, it’s good because the clients think that way. So now it’s a lot of positive signals for our business model.

What investors look for

[01:13:05] Tilman Versch: For the end ask a small question on numbers because you have many investor talks. What are the usual things investors focus on or ask about questions when they see your numbers or asked number-related questions?

[01:13:19] Sebastian Grabmaier: Well, there’s the typical German investor question. Why is the summer quarter always a little bit weaker than Q2, and what do you expect for Q4? I love investors that have a mid-term view and see rather entire years and then year over year to see the path. And then have a five to the three-to-five-year horizon to watch how the platform is developing. And I think that most investors are very, very similar to your questions. You know on all these very big projects because they are harder to understand and what’s the implication of it? And also understand the huge volume that is behind these contracts because if we take these big numbers that Lufthansa transfers 400,000 contracts or Provinzial is expecting one million clients, it’s quite an intake for investors to see these big numbers that are coming.

[01:14:23] Tilman Versch: Or the 140 million that will have no advisor through demographic changes. Also, like a number that is just like.

[01:14:31] Sebastian Grabmaier: Wow! But it’s a fact. It’s a lot of facts that are in favour of our model.

[01:14:40] Tilman Versch: For the end of our interview, is there anything you want to add we haven’t discussed or that comes to your mind as important?

[01:14:48] Sebastian Grabmaier: Well, we have touched upon this aggregation game that’s happening. So in the end, German insurers could have been the drivers for consolidation in the market which they are not. So there are still 500 insurance companies out there, 220 of them doing business with brokers. And on the intermediary side also there are now the first rollout models, but it’s still very fragmented. There are more than 200,000 intermediaries and what we’ve seen in other markets like US and UK is that there are now, well, money pots, investors coming, buying these brokers heavily. And this is why, together in a joint venture with Bank Capital in Great West, we are now starting our old roll-up model with an equity piece of 150 million. There will be a debt of about 350 or something million. So we have like firepower to buy now. A lot of other smaller market participants to even grow the platform faster. And this will be another fuel for our growth.

Staying ahead of the game

[01:15:47] Tilman Versch: This landscape that isn’t consolidated is also in your favour, so you have many small players and with many small players the platform makes much more sense or?