Marco Pescarmona, are you Italy’s best capital allocator?

Two years after our first interview (Is Gruppo Mutui Online the best Itali… ), it was great to have Marco Pescarmona of Gruppo Mutui Online back. The company has changed a lot since 2021.

We have discussed the following topics:

- Teaser

- Intro

- The biggest challenge in the last two years

- Biggest challenge at the moment

- Acquiring new businesses

- How the opportunities come up

- The structure of the transactions

- M&A at Gruppo Mutui

- How does Gruppo Mutui add value?

- Differences between Italy, France & Spain, and other markets

- New challenges after the acquisitions

- Three to Five-Year Goals

- The D&A from EBITDA

- The strategy with the BPO division

- Debt risks

- Looking back at 2012

- Reading out patterns during times of crisis

- Understanding the revenue side

- Thoughts on the different divisions within Gruppo

- The brokerage market

- Capital allocation framework

- Creativity

- Cashflow

- Closing thoughts

Teaser

[00:00:00] Marco Pescarmona (Gruppo Mutui Online): We also had very interesting M&A opportunities and that kept us quite busy. In the last two years, the company has been really different from what it was in 2021. We are not structured. With an M&A team or anything it’s like the M&A team is two, or three people put together when there are opportunities. I would say that in terms of challenges the biggest is probably dealing with…

Intro

[00:00:27] Tilman Versch: Dear viewers of Good Investing Talks, it’s great to have you back today and I’m happy to have Marco Pescarmona of Gruppo Mutuionline. It’s an interesting time to follow up after two years. How have you been the last two years?

[00:00:42] Marco Pescarmona (Gruppo Mutui Online): Very, very well. Thank you, Tillman.

The biggest challenge in the last two years

[00:00:45] Tilman Versch: It’s great to have you back. And regarding the last two years, what was your single biggest challenge in these last two years?

[00:00:54] Marco Pescarmona (Gruppo Mutui Online): Well, the last two years have been very busy years. So we came out of COVID and basically, that created a number of changes. We had some businesses slowing down like things linked to e-commerce and so on. But we also had very interesting M&A opportunities and that kept us quite busy. And the last two years, the company has been really different from what it was in 2021.

Biggest challenge at the moment

[00:01:27] Tilman Versch: So going into the here and now, what is your single biggest challenge right now as a business owner?

[00:01:36] Marco Pescarmona (Gruppo Mutui Online): I would say that in terms of challenges, the biggest is probably dealing with complexity. So we have a group that does lots of things and managing this complicated and adjusting the organization to increase complexity is an important challenge.

[00:01:57] Tilman Versch: What are you doing to adjust to this increased complexity?

[00:02:01] Marco Pescarmona (Gruppo Mutui Online): Well, this has to do with the talent and the people that are managing the organisation starting from me and Alessandro. But we have a number of very key people. And we try to have the strongest possible team and what was a good team for a specific configuration, is no longer a sufficient thing for a broader and more complex configuration, so we really have to find the best talent and organise these people in the most effective possible way.

[00:02:38] Tilman Versch: So is it mostly that you have these challenges on the talent side or are you also have to adjust structures, IT landscape, and systems to fit together?

[00:02:49] Marco Pescarmona (Gruppo Mutui Online): No, I mean, we don’t have such a big problem finding and hiring and retaining top talent. I think we have a very interesting project. Especially in Italy, but not only in Italy, I think that there is more talent and opportunities, and we have good opportunities. So the point is really designing the organisation and adjusting the organisation to allow the intake of new talent and also to fix, let’s say, all these cracks that one could have like you have made an acquisition and you have like duplicate systems that you would want to eliminate or there are many things that when you have complexity with M&A.

And complexity comes very easily where you need to intervene in situations that are not so easy, so it’s not a clear the thing, but things can be improved and the point is that the organisational design part I would say more than finding the right people.

Acquiring new businesses

[00:04:03] Tilman Versch: So you’ve spent roughly 250 million acquiring new businesses. Correct me if I get the number a bit wrong. Can you maybe walk us through what acquisitions you made and what chances came up for you?

[00:04:22] Marco Pescarmona: Yes, I think I’ll comment on three acquisitions. One is smaller and was done a bit earlier. The smaller one is a company called Europa and it does cadastral services, not only cadastral like title services as well, so it’s very technical services linked to real estate in Italy. And that was a nice acquisition.

It was not big because it was about €15 million in enterprise value, but it was a leader in the field with a lot of potential and also we acquired all the technology behind it. And that’s something which we are building. And it’s an acquisition similar to the ones that we did in the past. So very, very good valuation, I would say, for a business that requires some work. And so there’s an interesting story. But I would say it’s a bolt-on where we found an opportunity and we like the entrepreneur and we thought let’s do it.

So there’s one, but the more important one is a company called Trebi that we acquired for around €80 million. Because in a bit more than that, I think. That’s a company that is the leading provider of software solutions for the leasing industry in Italy. Leasing is a regulated business and requires very specific systems to operate. So the idea was that we had Agency Italia, which was the leading BPO provider to the leasing as well as the long-term rental industry and we also typically the main supplier to many of the players in that industry and we could combine it with basically our clients were using the Treby systems as the leasing clients.

And so we could generate efficiencies for ourselves and for our clients, by having control over like the software, the operating system, I would say of these businesses and the operational path. And also the idea was that we could leverage our knowledge of the rental industry, long-term rental industry, which is like a sister of the leasing industry, but not exactly the same and also develop a software solution for that sector.

So it’s the first time we really tried to combine BPO technology and operations and see if we can create value out of that. And we’re still at the beginning, but I think we are happy that we, you know, took that route and we’ll see how it goes, but we are optimistic in the end. And that’s the second acquisition.

And then the third and the biggest and really the boldest move I would say is the acquisition of a number of international assets that have originally belonged to Admiral Group. This is within the brokering division. And these are some comparison businesses. It’s Rastreator in Spain. Rastreator is the leading price comparison website in Spain. Then there is the LeLynx which is a co-leader in France, it’s mostly focused on insurance. And so I’m talking about insurance here.

And then we also acquired as part of the package, one of the co-leaders in Mexico, it’s called Rastreator Mexico. These are three companies that were profitable when we acquired them. And we think have a lot of potential for two reasons. One, we think this is also what we are seeing, we are able to apply our best practices to these companies and the results are already improving in a substantial way, and this means higher profitability without killing growth. So with some revenue growth, significant EBITDA growth and this is the first reason why we like these companies.

Second these companies are in markets that are even less developed than Italy for comparison and intermediation. And so there is also optionality, meaning that this is outside of our control or only we can influence this only to a limited extent, but these markets, could maybe in 10 years, 15 years, 30 years really unlock they could become multiple of what they are in terms of market size. So we have this option on the unlocking of the markets that we also got with the acquisitions and which we consider very valuable.

[00:10:03] Tilman Versch: Can you maybe explain how the first two acquisitions we talked about the bigger ones a bit later add to your mode? So how do the first two acquisitions add to your mode?

[00:10:38] Marco Pescarmona (Gruppo Mutui Online): Well, let’s say the first one, I think it broadens the offering that we have in terms of technical services linked to real estate and to credit I think we have the broadest panel of services. We are quite often able to offer integrated solutions and also we are able to come up with creative solutions that combine different elements together.

So this ability to offer integrated solutions or come up with creative things is helping us more. But again this is a relatively small acquisition. So maybe it makes a difference but not so big in terms of barriers to entry and so on. But when we look at, for instance, Trebi is clearly designed also to increase our mode, because we now are the, basically, we were already with Agency Italia, the leading supplier to our clients in terms of size and relevance for their business and with this acquisition was typically the second more most important supplier.

For the same businesses, so here we have an even deeper relationship with our clients and we can have a stronger partnership with them. And there is no one in the market that we think can offer anything comparable and the synergies in terms of know-how, in terms of ability to come up with commercial propositions that are really compelling and so on are potentially very high. So I think within the leasing and rental industry, this clearly reinforces our position and again a position as a partner to our clients but clearly there is a mode there and it’s now deeper.

How the opportunities come up

[00:12:51] Tilman Versch: So why did these opportunities exist in the last two years?

[00:12:55] Marco Pescarmona (Gruppo Mutui Online): Well, I think in the last two years.

[00:12:57] Tilman Versch: It’s both for all three opportunities.

[00:13:02] Marco Pescarmona (Gruppo Mutui Online): Well, I think every time there is uncertainty or some dislocations, there are opportunities. I don’t know it could be different things like a manager who wants to find a long-term loan for their business and after seeing COVID and realising that there are lots of uncertainties in life, maybe thinking about a new phase in life is important.

That could be one or it could be in other cases, I would say, well, not only had COVID, but we actually had a lot of stresses. Like we had the war in Ukraine and energy crisis and so on so, interest rates jumping up because of inflation and I think all these things increase the tensions in different places of the system and these tensions were sometimes just psychological in many cases, maybe they could have been also financial. In times of instability, there are more assets available for sale, I would say. And better opportunities for people who have the strength and the long-sightedness to look at opportunities in those moments.

So I think it’s a mixture and we don’t really know the exact reasons, but I think it’s a combination. Again, it’s because I would say there are times when there are more sellers than buyers and times when there are more buyers than sellers. I think the last two years, especially after the beginning of the war and then the inflation and the high interest rates they became more as sellers. More sellers than buyers,

I would say. I’m actually surprised because for us it’s more natural to buy companies. For me, it’s difficult to understand normally why one would want to sell something, especially a good asset. But clearly, it’s not the way most of the people see things.

The structure of the transactions

[00:15:42] Tilman Versch: Yeah, you’re a builder, so to say.

[00:15:45] Marco Pescarmona: Yeah, maybe. Yeah. Yeah.

[00:15:48] Tilman Versch: And especially looking at the biggest transaction you did, how was this transaction structure like, do you own always like 100% of the companies or is it also like that you have different setups within the transactions?

[00:16:05] Marco Pescarmona: In these transactions, we ended up buying 100% in all the recent transactions, but that’s because of the situation let’s say and basically because the ownership of the assets except in the small one was not in the hands of the entrepreneur. So there was a detachment between who would run the company and who was selling so. In that situation, it’s better to buy 100%.

And the way that was the only option available. But our preference in general or we are quite used to doing transactions where we work with entrepreneurs, where we acquire a majority, but then we run the businesses together with the founder or whoever was managing the company and they retain a stake and then we have typically put and call a few years down the road that could be extended in case we get along well.

But that’s our preference because it creates an alignment of interest and so on. But it’s not always possible to do it, and also sometimes we see it wouldn’t work with one person or another or a situation or another. And sometimes people just want to receive cash. But for us, we think that’s the best because it removes some potential pension overvaluation and also it allows the entrepreneur to reap the benefits of additional value creation which we could also help with synergies or knowledge transfer and so on.

[00:18:09] Tilman Versch: Let’s do one small sideway because there was also another transaction you did into a money supermarket where you bought 8% of the shares. And why was this also interesting for you to become a stock investor?

[00:18:23] Marco Pescarmona (Gruppo Mutui Online): Yeah, I would say, one point is that, in general, we are quite flexible. So we really try to generate value for our shareholders, and we do it by running businesses and allocating capital. When we did these money supermarket investments before the acquisitions, even before we knew these big acquisitions could be on the table, they were both a surprise, totally unexpected.

And so we had a financial position of net cash which was sitting on the bank doing nothing, basically. So we thought with more flexibility and I had always been following money supermarkets and the stock all of a sudden crashed in a very significant way. That was explained by a contingent situation in particular. The energy crisis meant that all the energy supply disappeared from the UK market and so money supermarkets, which were making pretty good money from the energy vertical. It was one of its biggest verticals and a big drop in income.

At the same time, there was a change of regulation in the UK regarding motor insurance. And so there was a lot of concern about the company in the short term, and financial performance deteriorated. We’re still making very, very good money, but significantly less than before. We thought the stock price didn’t reflect the value of the company.

And not even at the level of profitability of the time, so even at the level of profitability with energy not functioning, insurance only suffers. The stock price was still too low compared to what the company was able to generate. So we started looking at it in more detail, building models and so on like an investor would do and being from the same sector means it’s easier maybe to understand exactly how things work or read through the words of the annual report and so on and come up with good expectations and the good model. So we really think about the model, look at the model, double-check it, try to speak with people and so on.

And then we said this is a good investment because the energy will come back and the company by the way, just changed its management. So we also thought that the new management was a positive. So we started buying shares and we bought 1% and then 2% and then 3% and so on. And in the UK, you have to disclose it every time you pass a 1% ratio.

So we kept buying until we had enough, which was around 8% and its financial investment in a company that is exactly in our sector, even if in another country. So we are not competitors in any possible way. They are clearly domestic. So they’re not an issue even for our now international footprint.

And we like it a lot and I think so far it’s been a good investment. The company has kept improving. The management has done a good job. And also with inflation, insurance has picked up a lot. The reforms have not been negative actually and now we are starting to see the beginning of the recovery of energy.

We are at the very beginning so it will happen most likely in 2024 and hopefully, that will bring the company back to a more reasonable valuation given its strong brand, strong position in the market and so on. So it’s been a financial investment with which we are very happy and we will see what to do with it in the future. But for now, we are very happy.

M&A at Gruppo Mutui

[00:23:01] Tilman Versch: Generally, how does M&A at Gruppo Mutui work? So are you sitting there reading reports yourself or do you have a dedicated team for this? Or do you just call some experts when something comes up and the team forms?

[00:23:17] Marco Pescarmona (Gruppo Mutui Online): Yeah. This is something for which we are not structured with an M&A team or anything. It’s like the M&A team is two or three people put together when there are opportunities. By the way, we are not even looking in such a structured way at M&A opportunities. So we want to be ready to react if there are good opportunities and so far, we have been able to handle very complex transactions with these setups.

Sometimes it’s demanding like when we did the international acquisition of Rastreator, LeLynx et cetera. That was a very complex setup because there were entities in four or five jurisdictions. The contracts that will be done under UK law and so on. So there was a lot of complexity, and of course, we had to hire lawyers to help us with that. But like, for instance, for the business part like this due diligence. We normally do it ourselves and we do a lot of stuff ourselves and very, very much and so on and quite involved in that part.

I would say now that we like, I used to run, as the first time the brokering division, then we hired the person who’s basically a general manager or more, even the CEO of the brokering division and it’s full to the responsibility. So I have more time and this more time has been dedicated more to transactions. But you’d be surprised. It’s super simple. We are not many people. We are very few and sometimes it’s very intense.

Plus COMMUNITY

Discover the Plus Investing community

The Plus community is a great resource for professional investors. Members get support to grow their business and careers, are easily able to connect with other investors and can share ideas and join in-person events.

[00:25:17] Tilman Versch: That sounds interesting. Let me go to the transaction of the brokering division and I’m interested in how these businesses played together in Gruppo Mutuionline. Are there a lot of synergies between the Italian or the international broken divisions or is it how different interaction?

[00:25:38] Marco Pescarmona (Gruppo Mutui Online): Well, in terms of hard synergies, there are very few because it’s difficult to put together any piece of the organisation or of the systems or anything. So it’s more a matter of you know how to run these businesses and it’s like a lot of details. I think it’s possibly like a paper production plant or a steel production plant.

Where it’s a lot about tuning small details, small secret recipes that make you better than others. And so we think we have a little bit of those ingredients and so far we’ve tried to apply them to international businesses with good results. We still don’t know if we have any particular advantage, but certainly, the synergies are not hard synergies.

They are much more difficult to find, let’s say, and also knowing that the business you acquire could be improved or not is not so obvious because again it’s not costs that you eliminate or bargaining power that you acquire or anything. It’s more like maybe you can do a better advert because it works and that advert sells more.

But it’s very hard to say the recipe that was working in the country will work in another one. This way we are happy with what we did. We are seeing the results but saying that we have a recipe, still a soft recipe. It’s working, but it’s a soft recipe.

How does Gruppo Mutui add value?

[00:28:14] Tilman Versch: Let me do a quick small follow-up on this. So why are these businesses better because you own them?

[00:28:21] Marco Pescarmona (Gruppo Mutui Online): Well, I think we are focused owners. So these businesses that we acquired come from a situation where they were not the core business of their owner, let’s say before they were owned by Admiral and Admiral is a strong insurance company but their aggregator businesses were possibly there to feed in a way, they’re direct insurers or to develop the direct market in which they operate.

So they were enablers and not their core business. Still, they were you know operated by good people and with good principles, et cetera, but they were not the core. And then the businesses that have been acquired by a UK company that had acquired a bunch of assets altogether. Including a large UK aggregator, they were interested really in the UK assets. Because they were a UK company, the international part was not their core business again. And it was small for the complexity that it entailed.

So I think the key difference so far, the easy one to say is that we like these businesses, they are really our focus. We put all our attention into them, and we try to have a simple strategy with strong execution. And I think this focus, and this being a specialist with 20 years of experience in the sector, I think is what makes a difference as a better owner.

So I think the key difference so far, the easy one to say is that we like these businesses, they are really our focus. We put all our attention into them, and we try to have a simple strategy with strong execution. And I think this focus, and this being a specialist with 20 years of experience in the sector, I think is what makes a difference as a better owner.

And by the way, we are a permanent owner of these businesses. So these are businesses it’s not like private equity where they buy the company try to pump it up, and make it flow. But also maybe go plate it and so on to sell it later and create or accept fragilities. We don’t accept fragilities. We try to build, invest in, or shape the businesses for long-term growth and profitability and that also makes us a better owner.

Differences between Italy, France & Spain, and other markets

[00:30:48] Tilman Versch: You already mentioned that there are differences in the market between Italy, Spain and France now. What are these differences and how comparable are these price comparison markets?

[00:31:01] Marco Pescarmona: I would say, well, in Europe, probably the most advanced mark, no, not probably certainly is the United Kingdom, then possibly Germany and then Italy. I don’t know really central Eastern Europe though. And instead like in Italy more or less 10% of the insurance or mortgages go through price comparison.

What is it in Spain it’s probably between 5% and 6%. These are like very ballpark figures. And in France, it’s maybe less than 3% for insurance. And why is it different? I think consumers are very similar. Consumers have the same, more or less level of education, the same level of access to technology and so on but for, like insurance and financial products in general, the difference is normally more on the supply side. So like in Italy, we have a highly competitive supply with a good number of direct insurers and that allows the market to keep growing.

Still, we don’t have the traditional insurers on board, and it will take many years before the penetration becomes comparable to the one-off, say, not even the UK, but say of Germany. But if you go to Spain, still you have some large direct insurers that don’t really work with the channel to its full potential, and by the way, in this way, they’re probably losing the big opportunity and the risk remains behind.

So in Spain, even the direct insurers there are a number of them and most of them work with aggregators, but not all of them and there is clearly an issue both for the aggregator and for the growth of the channel. But also for these players, I would say. And in France, it’s a similar situation, but worse I would say because there are very few direct insurers in France, there are like two or three pure direct insurers and then there are many traditional insurance companies and being conservative, I would say. So the direct insurance themselves are not enough to have a good development of the market.

There are also modern brokers that are helping, but they’re not the same as a fully-fledged direct insurer. So there is a big supply too, and I think also the aggregator maybe in France has not done such a great job in speaking with insurers because the insurers should benefit from aggregators and even traditional insurers, they could learn and benefit from working with aggregators. And it’s something that is happening anyway.

But being these companies like the one that we acquired, but not only ours like Anglo-Saxon origin, they were possibly run in a way that was too linked to an idea of the mark that was the UK model that was too advanced for Europe, so possibly we were not speaking the right language also with insurers.

So I think we would need to have a dialogue with existing insurers. We will need to see new players coming into the market, which is a very nice market. But again, I would say it has more to do with the supply side than with consumers.

And finally, it also has to do with your ability to execute. Ao within the market, the development of the market depends very much in this case where there are supply constraints on the supply side. But it also depends on how good you are at serving the consumers. So providing a good service, an easy service, making it well-known and so and so. Probably also the operators are to some extent responsible for a lesser degree of development of the markets.

New challenges after the acquisitions

[00:35:55] Tilman Versch: Maybe you want to use the chance to drink something because the next question is a bit longer. Acquiring a business is a bit like moving together in a relationship at the beginning it feels good, but over time some challenges might come up that you haven’t anticipated. So coming back to the acquisitions, what kind of challenges came up you haven’t anticipated and how you’re dealing with them?

[00:36:26] Marco Pescarmona: I don’t think we had many surprises. I think we had a very strong business in terms of also brand reputation, and positioning. Also in the labour market in Spain. In France, for instance, we have a smaller business, and we want to make it grow. We will invest in it, but it’s a more difficult market for talent, I would say.

And nothing that we were not expecting. But let’s say also coming from an Italian background, I’m not saying you have a credibility problem in other places but a little bit you have to prove yourself, and that’s maybe less needed in a country like Spain, which has more similarities. In France, maybe it’s a bit more difficult and again we are doing pretty well in France.

So it’s not a big issue and possibly also France is a more complicated labour market but that’s where we are. Sometimes it takes us longer than we expected to recruit people, even if it’s a very, very good opportunity. But it’s very minor things really.

With these acquisitions, we were actually surprised that we didn’t have so many surprises. So by the way, this is like a random thing. Sometimes you have surprises with acquisitions. But sometimes you even have surprises with your own businesses. There’s a point of surprises because they could come from regulations or like new entrants, you know, irrational things. So they could be anywhere. So far, especially with the international acquisitions, I would say very, very few surprises on the negative side.

Three to Five-Year Goals

[00:38:54] Tilman Versch: What is your three to five-year goal with the international brands like making the market leaders, growing profitability or something else?

[00:39:07] Marco Pescarmona: The goal is to develop them to potential. That means increasing. I would say making them grow in terms of revenues and in terms of percentage margins. So we have not given any target on this, but these are businesses that could operate with the EBITDA margins of say, just looking at the international comparison, say 25%, 30% is quite normal if you look internationally and we acquired companies that were doing much less than that. But more importantly,

I think we can help to develop the market and retain or develop a very strong position in each of our reference markets. In a company, the market in its development and potentially see it unlock at a certain point. The idea is that this will be domestic markets for us, just as Italy is and it’s fun for us to look at Spain and France, Mexico and understand the markets and so on and help that the companies develop.

And we are really trying to become on the brokering side of international players. We are at the beginning; we really have to be successful here. We have a lot of work to do but it’s something that is it’s a challenge we really like. Part of it, we do it for like the financial performance, but part of it, we do it for the fun of it. The fact is that it’s a new challenge and we want to see if you’re good at it.

The D&A from EBITDA

[00:41:02] Tilman Versch: You mentioned EBITDA margin. How do I have to think about the D&A in this kind of industry?

[00:41:11] Marco Pescarmona (Gruppo Mutui Online): I would say the best way to look at it is to try to look at the cash EBITDA. What they mean is, well, especially with acquisitions the accounting has an impact on how the results are reported when you make an acquisition of a company that has intangible assets, normally you have to do a purchase price allocation exercise whereby you allocate the part of the difference between the price and the net equity of the company to asset.

Typically, what you will see in companies like the ones that we have acquired is that you recognise there are software assets that are intangible and there are trademark assets like the brand name and so on. And so you make an acquisition and you like those are the numbers to 100. Net equity is 20, so there are 80 to be allocated and you end up maybe allocating, I don’t know, 40 or 30 to the software, another 30 to the trademark, and the remaining part, the 40 that remain are goodwill.

The software and the trademark under IFRS are then amortised. The software is typically in, say in our case, in five years the trademark may be in 10 years, but you create a lot of depreciation. In this example, you would have like 1/3 of 30. So that’s 1/5 of 30 is 6 every year, just for the software and another three for the trademark.

So just this acquisition of 100 million would generate 9 million per annum of depreciation of intangibles that you had bought together with the company and it’s just an allocation. So I would say the best way if you want to get a clean look at the profitability of these businesses, the best is to look at say EBITDA minus the investments or EBITDA minus CapEx. That’s one way to look at it. Or you look at the EBIT and you add back the PPA amortisation.

That’s why we disclosed that kind of information because that’s closer to the cash generation of the business and that’s the best indication I think of the actual performance and the best way to make a comparison and when we make acquisitions. Also, we try to look at things in that way.

The strategy with the BPO division

[00:44:33] Tilman Versch: Shareholders sometimes have fantasies, and there was also a question that had the fantasy involved that you use with the newly entered market. The brokering divisions also expand the BPO division to new markets like Spain and France. Is this an opportunity or what kind of opportunity do you see for the international markets on top of the existing brokerage?

[00:45:02] Marco Pescarmona: Well, I would say for now the strategy is that we stick to Italy with the BPO division because we still have lots of opportunities in Italy and both organically and in terms of M&A and so we are not looking, and we would not be considering normally opportunities abroad. We will consider opportunistic opportunities abroad for the brokering division even if now we are focused on developing the countries where we are present.

Then in general, I must say we have always kept, I mean, someone can then want to sell us a super interesting BPO business in Spain for almost free. We will consider it, but it has to be super compelling. So this our due now that BPO space is local and brokering internationally, but possibly considering other countries, if opportunities arise. But I would say, again, if there is a really compelling capital allocation opportunity that maybe means that we do something abroad for the BPO division, we’ll consider it again. But it’s not what we are looking for, so any gift, we take the gift.

Debt risks

[00:46:47] Tilman Versch: Another thing that changed in the last two years is the debt level, which is also a function of acquiring new businesses. It’s in the range of three to four times EBITDA to debt. It’s not a crazy debt level, but it’s also like a different risk profile compared to 2020-2021. How do you manage this debt risk while also having the changing interest environment in mind?

[00:47:15] Marco Pescarmona (Gruppo Mutui Online): Yes, well actually that level is going to be around three times EBITDA at the end of the year and this is the reported debt level. Then we of course have the participation in money supermarkets and this is worth more than one time our EBITDA. All of our banks now have covenants on the data that consider the net financial position net of the money supermarket participation.

So in the covenants, the debt level is considered to be two times a bit down or a bit less at the end of the year. And of course, the investment in a money supermarket cannot be sold immediately. If we wanted to but it’s quite liquid and it’s something that if we wanted to do a really significant acquisition, we could dispose of. So I think it’s the right way to look at the situation.

So I would say from our point of view as well, from the point of view of the banks, the debt level is around two times EBITDA. And we have a business that continues to generate cash and we will continue to pay low dividends as soon as we are with a significant amount of debt. So there will be a natural deleverage.

I would say the most natural outlook is we sit on our many supermarket participation because we like supermarkets naturally the cash flows we generate from the business progressively the leverage and so it goes down. And then of course, if there are M&A opportunities that come up, we will instead spend the money to acquire the companies. And so maybe we will not leverage or we will go up a little bit, but I would say our comfort level is between where we are.

We are in a comfort zone. We could have a little bit more, I would say up to three times including the money supermarket stake, would be okay for a small period of time, but longer term we would aim to be, let’s say, again net of the money supermarket stake, aim more to be between 2 and 1.5 times EBITDA because that’s what gives you the flexibility to do things.

Otherwise, you are focused on managing the debt, which is not what we want to do. We want to have the possibility to catch opportunities when they arise. And to focus on growing our businesses. I think a certain amount of debt is actually helpful, it’s efficient. Exaggerating could be problematic, but we are not in the situation you asked about the interest rate risk. And of course, interest rates increased a lot and also our interest rate cost increased by, say, probably more than 10 million in a year, which is for us is still manageable.

But we wouldn’t want it to be more than that. And by the way, the other thing we’ve done so far is to stick to bank debt and bank debt is relatively inexpensive compared to other alternatives. But of course, it’s more conservative. So you could get, in Italy, very good terms for corporate debt. But they would lend you up to 3–3.5 times EBITDA or difficult to do more. And we think it’s a good equilibrium because it’s cheap and we don’t get too much of it.

And it’s consistent with the way we want to manage our leverage. Also, sorry, let me say one thing. In the past, but even recently we had situations in which very important pieces of our business suffered significantly. Like, I still remember 2012 when the Italian stock market, sorry, mortgage market almost disappeared overnight. So it was -70% from 2011 to 2012.

And those situations could happen. Now we are much more diversified, so it’s less likely, but you know if you had the time it would have been a very difficult moment. So you cannot have too much leverage also because if you have a serious problem then you could be in deep trouble. But again the level where we are is I think appropriate.

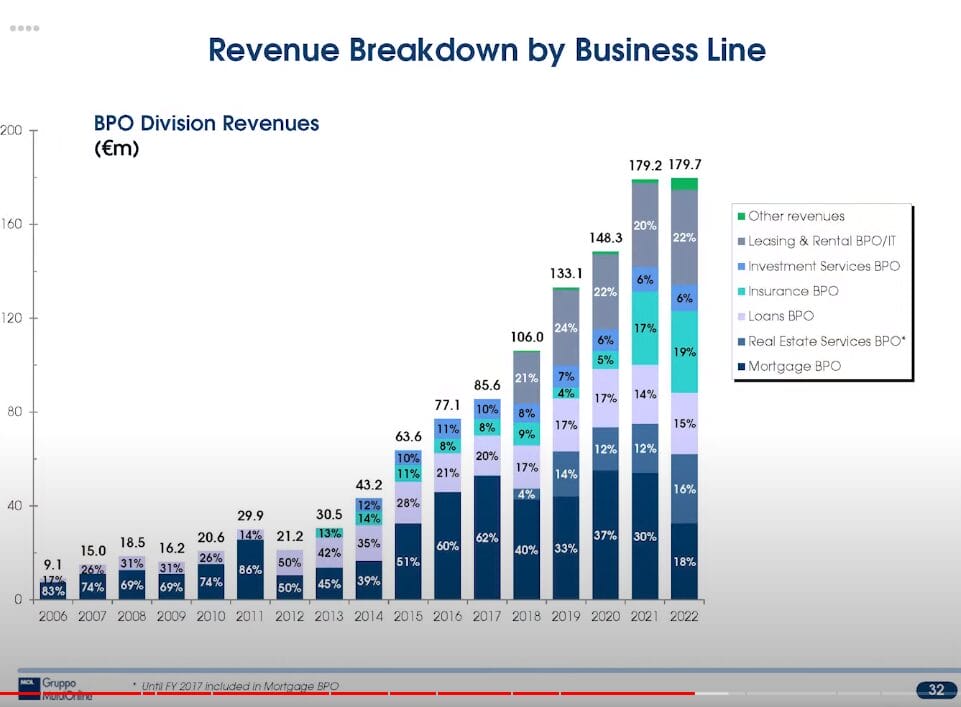

[00:53:09] Tilman Versch: Finally, I have written this chart here where you see the blip in the mortgage market from your presentation. We will embed it in a higher quality so that people can see it and it also was one question like compared from here to here, you have a way more diversified business now.

[00:53:30] Marco Pescarmona: Yeah, it’s well organic, by the way, this year you see we are growing year on year but of course, with the acquisitions, but even organically, thanks to the diversification, we would have seen possibly like a low double-digit. So today in Italy, like in Germany, like in all European countries, in the United States, the mortgage market is down significantly.

That means most recent figures were like -40% year on year. So not like 2012 but still a very deep contraction and despite that thanks to the diversification and at constant perimeters with other acquisitions, we would have seen a modest decline in our results. So we would have been in a safe zone anyway. Of course, we wouldn’t have the debt of the acquisitions.

[00:54:39] Tilman Versch: So I think on this chart it says it’s gone down from 30% of your revenues in this case to 18% of the mortgage part. But still, the revenues are on the same level between 2022 and 2021.

[00:54:56] Marco Pescarmona (Gruppo Mutui Online): Yeah, by the way, yeah, the point is as you said mortgages despite the fact that we are still called Gruppo Mutuionline which means online mortgages. Mortgages are no longer a dominant part of the business. Actually, they are, I would say less than a quarter. And we are in a number of markets and businesses that are correlated and that means we are a much stronger company today than we were in the past.

Follow Tilman for more insights

Follow Tilman for more insights

Looking back at 2012

[00:55:32] Tilman Versch: But nevertheless I want to do a follow-up question on the mortgage part because it’s also interesting to hear your perspective on it. Is it like how bad is it compared to the 2012 scenario?

[00:55:48] Marco Pescarmona: No, it’s not. Not comparable. So 2012 was like Italy could be getting out of the euro, and the euro could fall apart. There was a tail probability, I would say just a tail probability, but we could feel it. The entire banking system would be nationalised and so on. In retrospect, maybe it was unrealistic that this could happen, but at the time we felt there was a risk, and that’s what the financial markets were telling us anyway.

So it was a very, very difficult situation. Italy was at the centre of the storm together with Spain and Greece. And first, the banks in the state were in trouble. And then the measures that were put in place in terms of, let’s say, reforms and fiscal discipline basically scare all of the Italian consumers who for like the next three to four years they stop buying cars, they stop buying houses. They were wondering if they would have a pension later in their life.

And so they were just not doing anything. And they demand it, it frozen. Maybe the reforms were not even too impactful. So it was just the thing that the country was in difficulty and they were to do serious reforms. That really scared everybody. And we don’t have anything like that. So today we have also reforms.

Now the reforms that Italy is doing are possibly similar to the ones of the time and they are now linked to resilience plans. So it’s like Italy is getting money and in exchange, Italy is doing reforms, which is a good deal for everybody, I think. And helps to give political support for the reforms. So we are doing things that are, I would say, as effective. But people are not concerned because it’s not the problem in Italy today.

Actually, there is low unemployment. Companies are doing well and so and so. In general, this is more like a recession that is not driven by a problem in the country, but it is kind of important. It has to do with the energy crisis and so on. And so people, of course, they’re spending less, they’re waiting to buy a house because interest rates are higher and maybe they cannot afford it. But there is not this element of fear that was present. But I think having been in the business for 20-plus years, the one that we have now is a serious recession or the behaviour that you would see in a recession for mortgages.

But it’s a normal situation, whereas the situation in 2012 in Italy was totally normal. It’s one of those things that you see once in 50 years. So I mean it’s not great what we are seeing for mortgages, for interest rates, and so on. But it’s going to pass and really doesn’t feel like what we had in 2012. Even just looking at the mortgage market.

Reading out patterns during times of crisis

[00:59:38] Tilman Versch: So having this 20 years of experience in data is there any comparable phase you had where you might see a pattern that could offer a prognosis basis for the mortgage part?

[00:59:54] Marco Pescarmona (Gruppo Mutui Online): No. Well, I would say the situation we see now there is of difficult market. It’s not exactly the same, but it’s more similar to the situation we had in the financial crisis, the subprime crisis. It was 2008, 2009. Basically, at the time we still had a lot of instability of interest rates, and a lot of issues slowed down like globalisation, but this was coming from abroad. And so we had a decline, at least in some parts of the business.

Especially in the BPO part. Some of our clients were affected. But in the overall mortgage market declined, but you could see it was temporary and things would go back to normal at a certain point. So and also previous recessions. But now I couldn’t tell the years we’re similar. So this a situation that you could see as a fluctuation and nobody in the country anywhere thinks that there is a risk for a permanent change, for a permanent impairment of the economy or whatever. You feel it’s like winter, but then the spring will come.

Whereas in 2012, at a certain time, the sensation that maybe the spring would not come. So the cause a permanent climate change. Here it’s like we are waiting for the spring to come back.

Understanding the revenue side

[01:01:50] Tilman Versch: Thank you for the great picture, that helps. And I have one technical question on the BPO division. When do you exactly recognise revenue? Is it only when a customer, for instance, Allianz pays or is it in advance? And if it’s in advance how much in advance?

[01:02:11] Marco Pescarmona: No, no, there is not much in advance. Customers pay because it’s when we render our services. So like of course we make an invoice and in Italy our customers normally pay, say two months after receiving the invoice.

But in the great majority, there are some very small areas where we have to recognise with estimates but it’s normally we perform an activity and once we perform the activity we recognise our revenue. By the way, quite often we recognise the revenue when the activity is completed. So not halfway through. So I don’t think we have overall this issue. By the way, we have businesses where the activities are longer, but there are not so many.

So of course like mortgage underwriting that could take six months and there you have the issue of potentially recognising things that you have done that certain, but that you are not able to invoice, but that’s minor, but like in many other areas the activities from when we get the task to when we have performed it, it takes, say a month or so and there you easily recognise the revenue.

So I would say revenue recognition is again based on having performed activity and typically the revenue is recognised, then we issue an invoice right away and then the invoice is paid 60 days later. We have working capital because in many cases within the BPO division, we have an issue reconciling things with our clients.

So maybe the clients will pay us in 60 days, but before issuing the invoice we have to send them a report and they have to look at it and so on. And it takes a couple of months to do that. So typically, we have half of our receivables that are invoices to be issued. So we have performed the activity. We are reconciling so the invoice has not been issued yet and then there are another 60 days more or less that the invoices have been issued but not been paid yet.

But again we don’t have an issue of having significant revenues or receivables that come from estimates.

Thoughts on the different divisions within Gruppo

[01:05:23] Tilman Versch: Let me jump to a higher level and talk about business quality. So you have two business lines, the brokering division and the BPO division. In terms of business quality, what line has a higher business quality for you? It’s hard to rank, but let’s try it.

[01:05:45] Marco Pescarmona (Gruppo Mutui Online): No. Well, it’s really hard to rank and I think the two are both high business, high quality. Brokering has these, I think, characteristics that I like a lot. That is a business that can be operated with a relatively small number of people. So it’s a business of know-how skills, systems and so on, trademarks, like of intangibles and a small a small number of people. Then it is open to competition, but also as barriers to entry.

So it’s very nice. BPO is a business, the business that we have that is normally number one in all the important verticals in which we are present. So we have a strong position. It has the complexity that comes from needing not only technology because we use a lot of technology, but also a significant workforce.

So it’s a very strong business, it’s a market leader in verticals. These verticals are not so big. So these are issues that are quite defensible, I would say, but at the same time again we have the complexity of a large workforce and when you have capacity fluctuations, it’s more difficult to adjust. So these are the pluses and minuses of the two businesses.

And then again they’re about the same size. By the way, in the past, this may no longer be the case. In the past, we preferred BPO from the point of view of being able to deploy capital because we could make acquisitions there and we thought we could not do much in brokering. But this not no longer the case because now that we are international, we have possibly also opportunities for brokering to allocate capital.

For us, they’re like half of the business season. We like both, even if they have different characteristics and different investors highly value one part and or the other. It’s fairly like both at the same time.

The brokerage market

[01:08:33] Tilman Versch: What kind of market is the price comparison or the brokerage market? Is it like, will there always be a few players that compete and you need to spend on advertisement and to be on the intention side of the customer? Or are there certain conditions where it could be more like a winner takes most market?

[01:08:55] Marco Pescarmona (Gruppo Mutui Online): Well, I would say both our businesses, both brokering and BPO are businesses that, for different reasons, tend to have a limited number of players and I would say this has to do with high barriers to entry. There are different types of barriers to entry, but it’s common to businesses.

And no, so I think they’re really nice for that reason. It’s also in that type of situation it’s more difficult to grow sometimes because one of the barriers to entry that we have in both cases is normally the fact that capital is not a strong driver of growth. So you commit more money to the brokering of the BPO division for organic growth.

And you don’t really know what to do with it. So you spend it, on brokering on advertising that has a very negative return because it’s all saturated or in BPO where do you spend it for? To develop IT systems maybe, but we are already doing it. It’s difficult to accelerate the growth with capital. This is the key characteristic of both situations and this is a key barrier too.

Capital allocation framework

[01:10:35] Tilman Versch: It’s interesting. Let me change to the most complex task you have at the moment capital allocation because you have so many new options. So we have the buying back shares, investing in Italy, investing in international business in different markets, paying back debt, taking care of opportunities that the market or the stock market offers. How is your capital allocation framework grown or what is your capital allocation framework? Let’s start with this question.

[01:11:11] Marco Pescarmona (Gruppo Mutui Online): Okay, so to say that we have a structured capital allocation framework. I think of course we understand the concept of capital allocation and we know that there are different opportunities and they’re not compatible sometimes with each other so we’ll try to generate value for our shareholders.

There will be flexibility in our decisions and we’ll consider things that are maybe not obvious. The things we could do anywhere from buying back shares to making acquisitions like the investment in money supermarkets was a capital allocation decision. In the end, it could be things like that. We and Alexander are also owners of the business and we try to generate value for ourselves and all the other shareholders within everybody of course. In the same way, allocating capital in a very rational but at the same time sometimes creative way depending on the opportunities.

So we don’t have like a rule that says we want to make acquisitions first, but then we buy make or vice versa, et cetera. We see where things are and based on that we decide. So if we only had expensive acquisition opportunities, we would stop doing acquisitions. If the stock is super cheap, maybe we could become even more aggressive with the buybacks. Or if that is super expensive and we don’t know what to do with the money, we repay the debt. It really depends. The key point is this is done to the limit of our ability in a very rational way.

Creativity

[01:13:21] Tilman Versch: Let’s talk a bit about the creativity in the capital location. Can you maybe explain one or two cases where this creativity plays a key role and like it’s not only the rational key facts?

[01:13:35] Marco Pescarmona (Gruppo Mutui Online): One easy example is the investment that we made in the past in [unintelligible] first and then in Moneysupermarkets. So these are investments we made in companies we could understand pretty well because of our industrial activity. But this was also a bit out of the standard because normally you focus on running your business, acquiring companies that reinforce your business or expand your business.

But we did these investments to some extent working as an investor like doing the same things that people that come to our investor relations meetings. So they build models, and they try to figure out whether the management is reliable or not if they are honest people. So this was a bit outside of our standard, the expectations that people had for us running the company.

But we thought we had compelling opportunities and in the end and saying because in retrospect they would say, in the end, they generated very significant value and helped us to grow because these things have funded. Then we could fund the future industrial growth of the company. And this one thing.

The other thing is that in the past there was this opportunity, we had a different situation like this several times, but there was an opportunity in Italy to revalue intangible assets for tax reasons and it was a very, very nice law that they passed and basically you could pay like a substitute tax and revalue some of your intangibles and then amortise them for fiscal reasons. So that’s an investment in the end.

So you put up a certain amount of money and you get significantly more over five or 10 years. You can calculate the NPV of this and the internal rate of return and so on. The way we looked at it was as is very attractive capital allocation. By the way, this is a law that was very friendly to any company that had intangible assets, but many companies didn’t really realise that it was an opportunity or didn’t look at it the way with the same attention we put into it.

And it was capital allocation. Another example of capital allocation, which is just an opportunity, it’s not something we are currently doing. There are situations in which you could buy tax credits in Italy because they did some like state-sponsored property renovation schemes.

They generated a lot of tax credits for companies in the property sector, and these credits are transferable. And normally you have plenty of companies that have all these tax credits that are in excess of their tax capacity.

And so they might sell them. So you might be able to buy a relief on your future taxes at a discount. And so if discounts are at 5%, it’s probably not very interesting, but if it comes at 20% IRR, it’s very safe. This could be more compelling. So there are many things that could become available that have to do it. In the end, investments are about cash that could generate attractive cash flows given the price, et cetera and all these things are competing with each other.

Our focus is, of course, on developing our business in a way that people can understand that is predictable where we don’t buy a pizza chain, of course. So we do things that are predictable. But within our area of activity will be creative. With investments like money supermarkets that maybe are will be financial only or with things that have to do more with the debt management or asset management side of the company.

[01:18:49] Tilman Versch: So you mentioned this IRR of 20%, is this kind of your hurdle for the capital allocation decisions or…?

[01:18:57] Marco Pescarmona: Well, it really depends. By the way, sometimes when you start calculating hurdles and so on and you look at those positions, it’s also a matter of what you put into the calculations, because if you start estimating on the synergies, this and that, you can convince yourself always that you’re doing an incredible deal.

So, I would say, sometimes we don’t get to the point of doing an expected IRR or having maybe a safe IRR and then taking the synergies or the external benefits as a plus. So that we don’t overpay on the explicit part. And then we have a part that is maybe not fully quantified that we get this bonus. But I think like 20% is a good number anyway. It’s an aggressive number. So private equity firms would normally aim for 20% more or less.

You are not always able to do that. I would say. Yeah, ballpark. I think the things we have done are in that area, but we could do things that are lower. Or where the explicit part is lower because when there is option value for instance, it’s very difficult to give a value to, I don’t know, the option the French market for insurance broker brokering will unlock it’s a lot.

You could do formulas like blocking shoals or more sophisticated ones. It’s very theoretical, so you make sure that you are buying the company for a fair price and then you get the free option sometimes.

Cashflow

[01:20:56] Tilman Versch: You already mentioned the cash flows Gruppo Mutui. I think at the beginning it felt like you had two kinds of cash flow streams and now it feels more like you have like a lot of cash flow streams that come into the company. Does this picture, does it make sense?

[01:21:17] Marco Pescarmona: Well, yes and no. I would say because it depends on how you look at things. Still the brokering and the BPO division. Then of course both of the two divisions are much more diversified. So if you look at the diversification aspect, I think it’s true because you have many things that are linked to different parameters.

Something that benefits from inflation, something that suffers from inflation, something that goes well when the economy is going well. Something that goes well when there is a natural catastrophe. So we have things that are very diversified. So the average cash flows will be, say, more stable. Then the way we look at it is still have two main businesses brokering and BPO. So for us, it’s still this the no part. We still see two main separate businesses that are generating cash flows.

[01:22:27] Tilman Versch: But the verticals and like the correlation between these cash flows in the units is way different compared to 10 years or…?

[01:22:37] Marco Pescarmona: No, it’s a very low correlation. So I would say insurance has nothing to do with mortgages, which has nothing to do with energy staying on the brokering side. So really it’s this what I was saying before the quality of our business is much better now because it’s more diversified.

So now we have a number of quality businesses individually. And to that, we have the quality of diversification. And that’s true for both divisions. By the way, diversification works both ways, so no single issue is going to kill you, but you’re always going to have issues in one place or another because you are playing many different games.

[01:23:30] Tilman Versch: But like, there is no ultimate like 2012 where you had this big crisis with Italy? This is something that’s harder to imagine for you to have such a risk coming.

[01:23:42] Marco Pescarmona: No, it’s very hard to imagine. I mean 2023, maybe it’s not obvious from the results et cetera because the results are actually good, but was potentially a very difficult year. It would have been a very difficult year for the company that we were ten years ago. So we have already proven in 2013 with a very severe shock on the mortgage market. That we could perform quite well and save through it. Then again if you have a nuclear war, we would have problems, but everybody would have problems.

Closing thoughts

[01:24:22] Tilman Versch: Yeah, that’s clear. Thank you very much for the interview and the insights. I’m done with my questions. But at the end of the interview, I always want to give my guests the chance to add anything. So is there anything important over the last two years, structurally with the business that you want to add?

[01:24:46] Marco Pescarmona: No, I would just add that we have changed the Gruppo in a very significant way in the last 10 years and we keep doing it and it’s fun and we create value we think. And we have more opportunities today than we had in the past because we can look at more things. And if we are able to execute well, as we have done so far, I think it will make our shareholders happy.

[01:25:17] Tilman Versch: So maybe one question that came up for me. So you’re a bit in the acquirer phase right now or how would you react if I call you a Syria acquirer?

[01:25:29] Marco Pescarmona: No, that’s not correct. We are an industrial operator. No, we really see ourselves as an industrial operator our key skills are execution and being an industrial operator. Then, that skill enables us to also make acquisitions and create value for acquisitions. Also, we are long-term and friendly to entrepreneurs acquire companies and so on and that also creates value for the long term. But this is only because we are an industrial operator that likes its business.

[01:26:10] Tilman Versch: And thank you very much for making this clear for the end of our interview. Thank you for your time. To the audience. Bye-bye.

[01:26:15] Marco Pescarmona: Thank you. Bye-bye. Thank you.

[01:26:19] Tilman Versch: I really hope you enjoyed this conversation. If you did, please leave a like and a comment and make sure to subscribe to my channel.

Good Investing’s disclaimer

Please be always aware that this content is no advice and no recommendation and make sure to read our disclaimer: