Is Georgia Capital a deep value compounder, Steve Gorelik?

In this video, recorded on 06th November 2019 during the International Value Investing Conference, Steve Gorelik of Firebird Management explains why he likes Georgia Capital.

We have discussed the following topics:

- The Quiet Revolution: Corporate Governance in Eastern Europe

- Who said it?

- Returns on Capital of Steel Companies

- Reasons for changes

- Investment Idea: Georgia Capital (CGEO)

- Management record of accomplishment - CEO, Irakli Gilauri

- Management’s record of accomplishment - value creation in the portfolio

- Capital allocation

- Georgia Capital - current NAV

- Georgia Capital - Value

- Georgia Capital - Reinvestment opportunities

- Georgia Capital - expected NAV growth

- Q&A session

- Disclaimer

The Quiet Revolution: Corporate Governance in Eastern Europe

[00:00:08] Steve Gorelik: Thanks, Michael. So, as Michael mentioned, I am a fund manager at Firebird Management. Firebird is best known for investing in Eastern Europe and that is the side of the business that I am going to talk about today.

[00:00:21] Steve Gorelik: We’ve been investing in Eastern Europe for a little over 25 years – we celebrated the anniversary earlier this year – and within that time, we saw the region go from cheap on an asset value basis, so, when you talk about Russia and then voucher privatizations when we started the business, the whole Russia was valued at $7 billion (about $22 per person in the US) (about $22 per person in the US), to now, the region is cheap, not just on the asset basis, but also cheap in an earning basis as well. So, we are investing in the region with an average PE for the index right now at around 6x PE, which we find extremely attractive.

[00:00:54] Steve Gorelik: And there have been a lot of positive changes in the region. Last year presented the company Agora, which is a diversified Polish media company. A lot of good things happened. The stock price did not move that much, happy to take any questions about it if you are interested. But today, I am gonna talk about what we call ‘The Corporate Governance Revolution in Eastern Europe,’ something that we have seen, the changes that we have seen over the last 25 years that are not necessarily apparent to people who do not do this on a day to day basis.

Who said it?

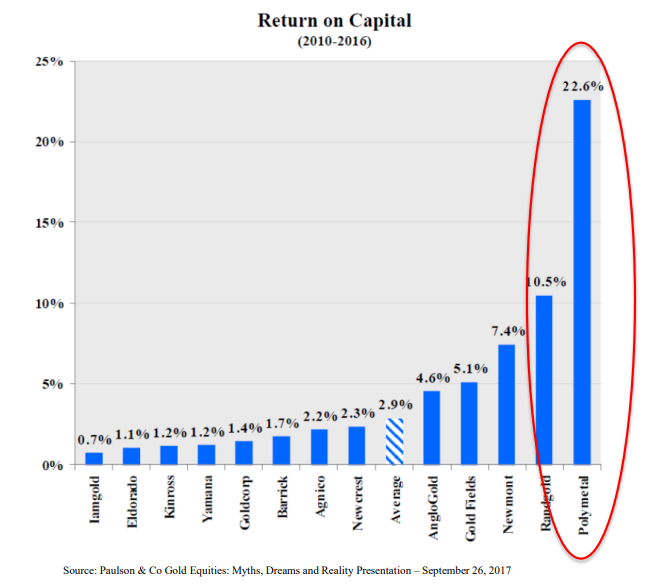

[00:01:23] Steve Gorelik: So, I am gonna ask for a little bit of audience participation. One of these quotes is from an Eastern European company, and one is from a developed world company. So, the first company says, “…We remain focused on driving our industry-leading growth projects forward under a disciplined capital location process in order to grow our business…” The second company talks about, “…really transforming production into dividends and dividends remain the first priority on capital allocation before any gross spend…”

[00:01:56] Steve Gorelik: So, if this quote is from a Western company, can you raise your hand? Okay. And if you think this quote is from a Western company? Okay. So, this (Polymetal International PLC) is a Russian gold company. The company on the left (Eldorado Gold) is a US gold company, and they do not just talk about it.

[00:02:21] Steve Gorelik: So, you can see the companies that talk about dividends, they talk about returns on capital, they do what they say they are gonna do. So, this company has the highest return on capital out of the major gold companies around the world.

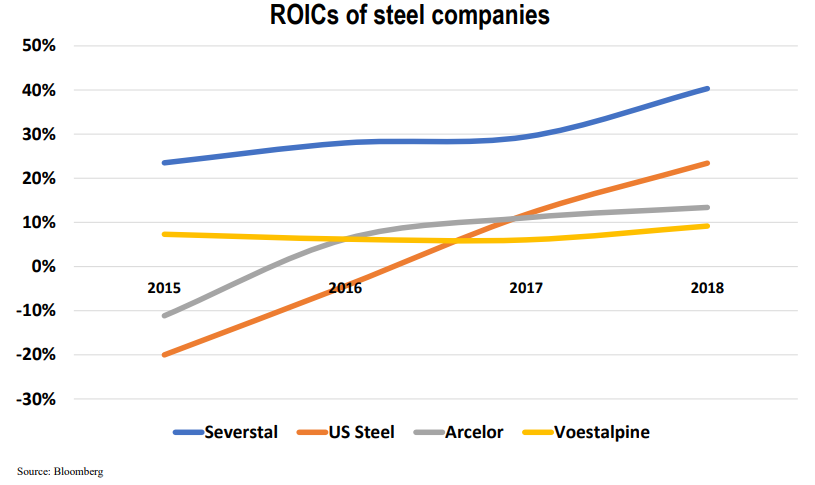

[00:02:38] Steve Gorelik: Another example from a different sector, we have a company that says, “…We effectively convert our EBITDA to free cash flow and committed to our approach to have smart CapEx with higher than 20% returns…” And another company says, “…We’re investing in operational excellence, investing in technology, investing in innovation that’s aligned with these critical success factors that we mentioned, or moving up the talent curve and moving down the cost curve, and then winning the attractive markets we got to take share.” So, which company would you rather own? Is the one on the left or the one on the right? The one on the left? Just a couple. The one on the right? Nope? Yes.

[00:03:17] Steve Gorelik: So, we like the one on the left as well (Severstal). It is a Russian steel company that does not just talk about capital location, they practice it. They do returns on invested capital over 20%, the dividend yield on it is over 10%, and they pay you a quarterly dividend. The company on the right is US Steel.

Returns on Capital of Steel Companies

[00:03:36] Steve Gorelik: So, you can see once again, returns on investor capital in Eastern Europe in a lot of companies that we are buying are much, much higher, and these returns are being distributed to shareholders.

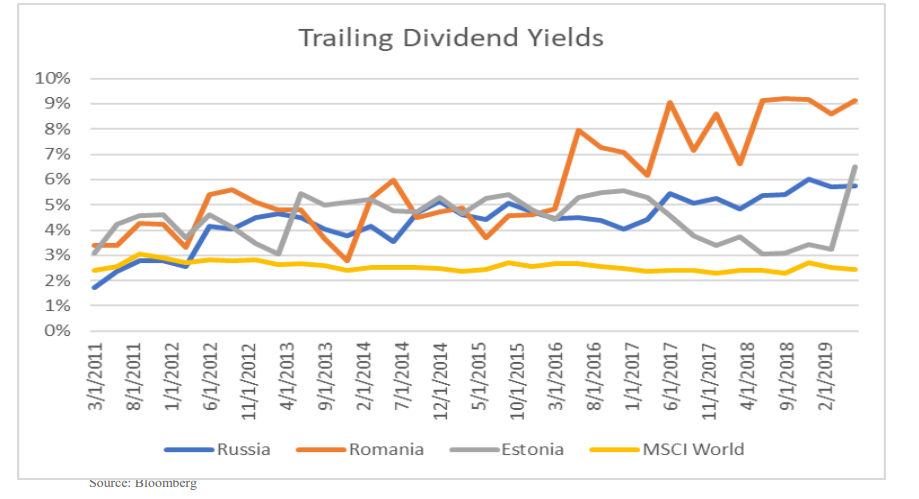

[00:03:45] Steve Gorelik: We see that change. So, one of the examples that we give is that back in 2002-2003, the Russian stock market was validated around P of five and the dividend yield was one and a half. So, there, you had a lot of earnings, but you were not sure what was happening to those earnings, whether they were either being spent on some projects that were not necessarily high capital returns, but you were not getting that money.

[00:04:08] Steve Gorelik: To date, P is six. It is up a little bit over this year, the market is doing quite well, but the dividend yield of the Russian market is over 6%. So, they are sharing the earnings. They understand what capital allocation is, they understand what it means to have minority shareholders, and they treat us accordingly. Romania has even higher dividend yields. So, we see this happening not just in Russia, but we see that happening all over our region, all these significant positive changes.

Reasons for changes

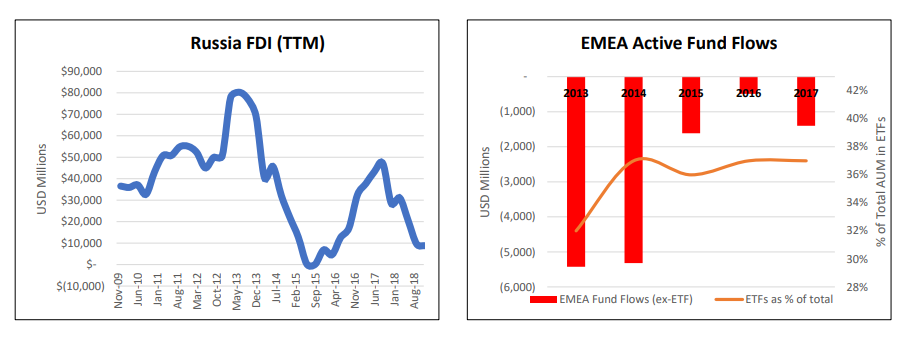

[00:04:34] Steve Gorelik: So, the question is, “Why did that happen?” And there is a few reasons that we put, and I pointed out two things. Before 2008, there was a lot of money coming into the region from all over the world. You had banks buying subsidiaries, Western European banks buying subsidiaries in Eastern Europe, pumping capital into the market because that capital had higher returns on capital. As quickly as the capital came in in 2008, they left because of the problems that the banks had on their own books in Western Europe. So there is no more capital flowing from these banks. There are still some subsidiaries around, but there is no more capital flowing from Western European banks into their Eastern European subsidiaries. It is more of the other way around.

[00:05:17] Steve Gorelik: And the second thing is in 2014, there was a war between Russia and Ukraine that is still an ongoing conflict, but that was another…in 2015, what happened was a lot of people that started looking at the market because of the good valuations really pulled back because, now, you had political risk, you had sanction risk, and there is a lot of different things that were happening in the market that really made you uncomfortable with investing there. So, we were in a position, our markets have been in positions of constant capital outflow for over 10 years at this point. It accelerated after 2014. So, what happens? Companies must learn how to be more capital efficient because they cannot count on capital coming in from the outside. So, in that turned over time, we see that translated into better performances of the business.

[00:06:05] Steve Gorelik: The other aspect is good corporate governance. If you run your business cleanly, if you have established the asset cleanly, then it is less likely that somebody will go after this asset. So, there is less likely that there’s gonna be a predation where unsavory actors will go after this asset because there is really nothing to catch on to. You cannot blackmail, you cannot… it is much easier if you run the business cleanly than if you can continue running the business and running the business well.

Investment Idea: Georgia Capital (CGEO)

Georgia Overview

[00:06:34] Steve Gorelik: One of the best examples of improved corporate governance and good corporate governance we find is in this company, Georgia Capital, which is the company I am gonna talk about today. Before I am gonna talk about Georgia’s Capital, I want to spend a little bit of time on Georgia, which is a country of 3.7 million people (about twice the population of New Mexico).

[00:06:51] Steve Gorelik: It is on the Eastern side of Europe and one of the distinguishing characteristics is that most of its neighbors hate each other. So, Armenia and Turkey do not get along, and Armenia and Azerbaijan don’t get along. There are a lot of conflicts around the region. So, while the countries may not be particular fans of each other, the business people want to trade and Georgia being the open economy that has free trade agreements with a lot of places, including EU and China, has become a natural hub for business activity in the region. And it is also a beautiful country. So, coming to visit Georgia as a tourism destination, the tourism numbers have grown constantly, and all of that is translating into good GDP growth. We see a GDP growth of four to 5% per annum in real terms, and closer to eight to 10% per annum once the inflation was included in nominal numbers.

Georgia – how did it get here?

[00:07:50] Steve Gorelik: Georgia has an interesting history, and you must understand where it is now in terms of how it got there. So, the early post-Soviet period was not a good place to be. You are talking about separatism on the borders, you are talking about civil war. If you go to Tbilisi today, the capital, you still see the signs of those conflicts all over the place. If you just go a couple of blocks from the main streets, you see buildings with bullet holes, and you must understand it was also like the most corrupt country in the former-Soviet union, and that says something. So, this was a country that was not a good place to be until 2003 when this guy Mikhail Saakashvili came in with a mandate to change things. He got elected with over a 90% approval rating. And he came in with a mandate from the people to change things for the better. And one of the first things that he did, he proceeded to fire every single police officer in the country because that was one of the roots of the corruption. And he then proceeded to say, “Okay. If you want your job back, you’re welcome to have it back. You can apply food, but things are gonna be different from now on. We are not gonna have corruption. We are making the government as small as possible.” He solved one of the separate conflicts with Adjaria, the two other ones are still outstanding, but it became a much better place to do business. It went up dramatically in rankings of doing business and became a country where you could live. And corruption has been eliminated as a result.

[00:09:18] Steve Gorelik: And once you eliminate corruption, the people who used to live in a corrupt environment and they no longer must, they really want to hold onto that. But the thing that he does not get any credit for, which is most important to the story of where Georgia is today, is in 2012, and he had this benevolent strongman approach to running the country. In 2012, they had an election. And there was a night, the election night when it was close where it was not certain whether he lost or not. And what he did is because he knew that if he tries to hold onto power in a way that is any way doubtful, it is gonna kind of really throw the country back into where it was before. So, he just left. He said, “I lost. I left.” And he left the country.

[00:09:58] Steve Gorelik: And the new people who came in, they continued to run the country like the same fundamentals that were built up during the Saakashvili years. They continued to be there from the point of view of the free open economy. This is still a wonderful place to do business, but there’s no longer that stigma that came with Saakashvili’s years as the strongman that he was.

Georgia today

[00:10:19] Steve Gorelik: So, right now, if you go to Georgia, Georgia is a good place to be. I have some pictures. This building on the left, bottom left, is a police station in Georgia. Every single police station in Georgia is made of glass. The reason it was made of glass is to show that people are watching them. You are not watching us, we are watching you. And that is one of the ways that the country continues to say, “We’re not going to have corruption.”

[00:10:47] Steve Gorelik: The building on the top right is a building in Tbilisi. There is one in every major city. This is called the Government Services Building. Anything that you want to do in Georgia that has to do with the government can be done within a building like that: pay your utility bills, renew your license, whatever you need to do, all in one place, once again reducing opportunities for corruption. The other two pictures are just nice tourism photos to encourage you to go.

Georgia Capital

[00:11:15] Steve Gorelik: Georgia Capital is a company that was listed last year in London. It was spun out from a bank – the Bank of Georgia. This was a collection of assets they have built up over the years by investing in other non-banking businesses. They decided to spin it out as a separate company because it was becoming a little too complicated as part of the bank. And today, it has a market capitalization of around 450 million and trades 1 million per day. And this is a fully listed company in London.

[00:11:43] Steve Gorelik: It gives you exposure to every segment of a Georgian economy that matters. We are talking they still have a shareholding in the bank that’s [00:11:50 inaudible] out, they have a majority share of a healthcare company that is also listed in London and they also participate in utilities, wine, and beverages, hotels, housing, education, you name it. They are involved in it if it matters. So, by buying Georgia Capital, you get exposure to the strong, vibrant economy and I am gonna make a case that you are buying at a particularly fair price. But one of the most important things about Georgia Capital is its management and how good of a manager they are and the record of accomplishment that they have.

Management record of accomplishment – CEO, Irakli Gilauri

[00:12:24] Steve Gorelik: So, the person running Georgia Capital right now is this guy Irakli Gilauri, who was CEO of the bank from 2006 to 2018, up until the spinoff. And then he decided, instead of staying in a larger bank, he said, “I’m going to go work…I’m gonna lead Georgia Capital,” which is always a good sign in case of a spinoff. If you see the CEO going towards the smaller company, that is one of the things that we look for. As the CEO of the bank, he did well. The bank’s net income grew by 18 times within the 12 years that he was there, the book value CAGR was 17% and he has a lot of skin in the game. So, he personally owns two and a half percent of the company, and both he and all of the top management gets paid primarily in shares of Georgia Capital. So, they have a continuous incentive for the share price to do well and they are very much aligned with us as shareholders.

Management’s record of accomplishment – value creation in the portfolio

[00:13:22] Steve Gorelik: It is not just directly. They have a strong management team, a large part of the bank’s management teams went into this business. They like being in this business because it exposes them to many different sectors. And the young people, when they go to work for Georgia Capital, they know that they can work at the bank, no more at the bank, but they can work at the healthcare company, they can go work at the utility company and they get to try a lot of different things until they find their home. And there is a lot of opportunities for advancement within that.

[00:13:50] Steve Gorelik: They have an extraordinarily strong record in everything that they have done. The housing development that they have done in the past has IRRs of over 75%. Georgia Healthcare Group, the company that they still have control of, was a company that was built up…they used to have an insurance division, a healthcare insurance division. Then, they realized, “Okay. The money is not on the payer’s side, it is on the provider’s side. So we can invest a lot of money into building up a strong healthcare company with hospitals, clinics, pharmacies, et cetera.” They have tripled their EBITDA in just three years and continue to do well. And everything that they have touched, as I mentioned, does well.

Capital allocation

[00:14:33] Steve Gorelik: One of the most important things about them is their capital location. This is what they are saying is their key competency.

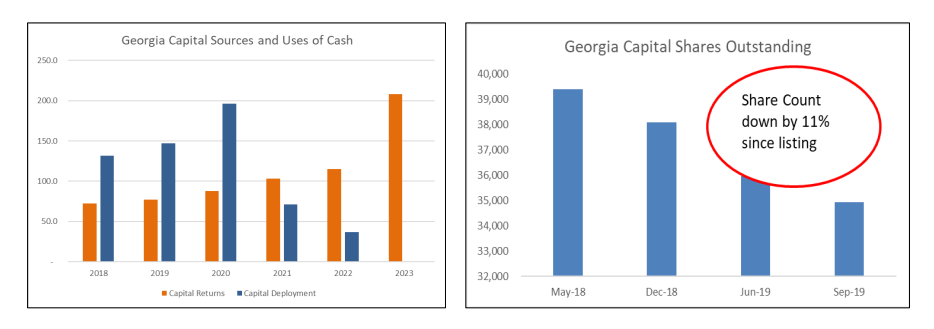

[00:14:42] Steve Gorelik: They focus on capital allocation and everything that they do. One of the criteria that they have is, “Okay. We have our own share price and we are gonna compare any capital that we are going to allocate to where our shares are trading. And if we have free capital and our shares make the most sense, we are gonna buy back shares.” In just a little over a year since listing last May, they already bought back 11% of their shares outstanding. So that kind of shows that they believe that the value of the shares is there. And meanwhile, with a lot of the capital they are gonna be deploying over the next two years, they do not need to issue any more shares. They are gonna be deploying capital that is coming in from the businesses that are already developed.

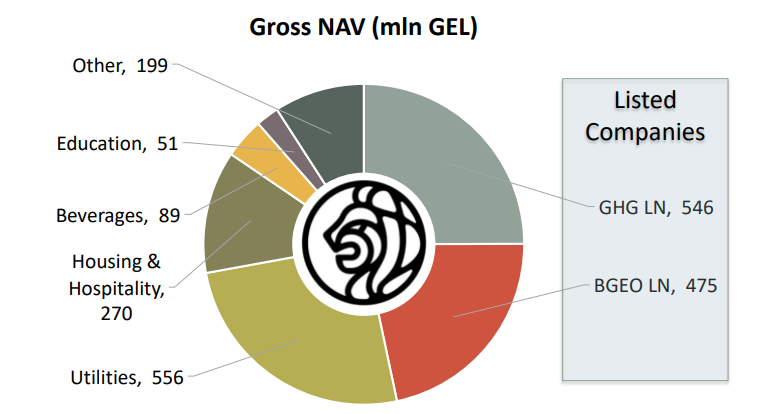

Georgia Capital – current NAV

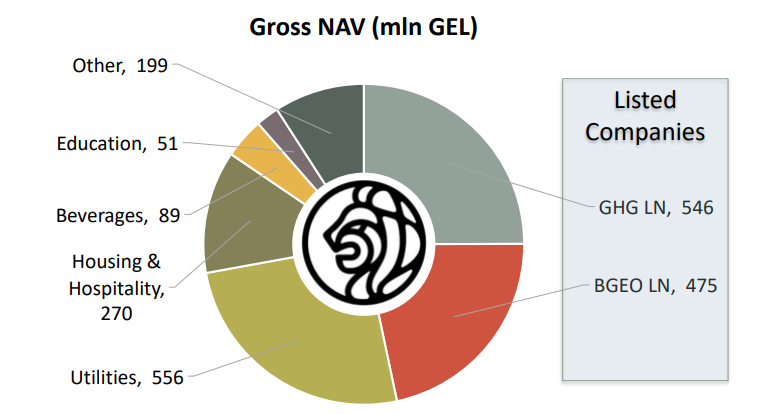

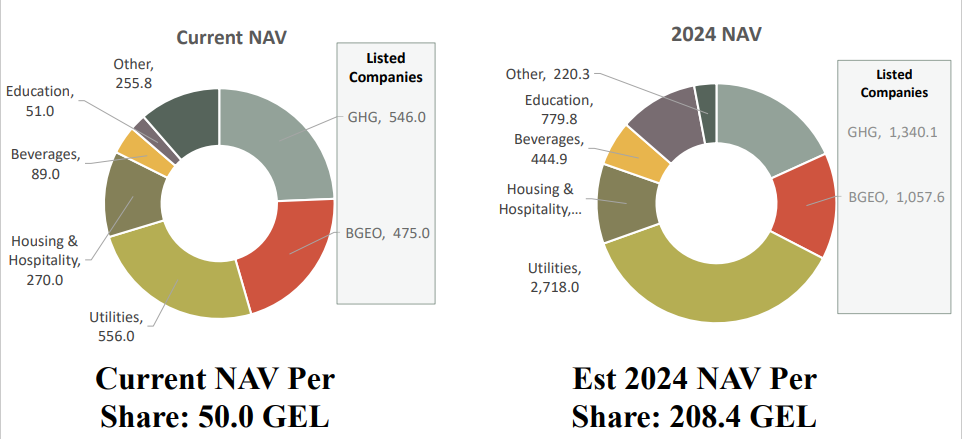

[00:15:19] Steve Gorelik: Their current NAV is about 50 Lari per share. About half of it comes from the two listed companies, so you can track exactly where it is. And they give you a lot of disclosure of how they produce the NAV of the rest of the businesses. If you look at their disclosures – this is an incredibly open company – they explain to you the multiples that they use. The important thing is that this NAV is growing.

Georgia Capital – Value

[00:15:45] Steve Gorelik: The company is cheap. It is not just the company itself that is cheap because it is trading at a discount to NAV, but also every piece of it, if you look at it separately, is cheap. Bank of Georgia, which is listed in London, is trading around 6P and 6% dividend yield, which is a bank that gives you 20 plus [00:16:00 inaudible] per year, grows at 10% plus per year and pays you 6% [00:16:06 inaudible] yield. We own the bank directly. We think it is extremely attractive.

[00:16:10] Steve Gorelik: Georgia Healthcare Group, same idea. This is a company that is trading at I think six or seven EBITDA whereas the other healthcare companies in emerging markets are trading at double-digit numbers. So, this is discount on top of discount on top of discount from the point of view of what you are getting here. And once again, the key here is the capital allocation and the capital allocation opportunities that they have coming up.

Georgia Capital – Reinvestment opportunities

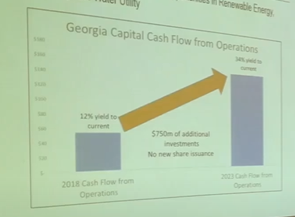

[00:16:35] Steve Gorelik: They’re building up a lot of renewable energy, they are building hotels, they have a lot of places where they can deploy capital. This is a company with a 450 million market cap today. They plan to deploy over 750 million dollars into various projects in various sectors over the next four years, and a lot of that money is going to be debt funded. They do not need to issue any more shares for these projects. And if you buy in it at a 12% yield today, then by 2023, once all these projects are online, a lot of them will have double-digit ROICs on an unleveled basis. So, on an unleveled basis, you are talking 30, 40%. You are gonna get to a free cash flow yield to today’s price of 34%, just in the next few years.

[00:17:32] Steve Gorelik: Aside from reinvesting in the existing businesses, they also have is they have platforms for acquisitions in various sectors, like beverages, where they are able to buy smaller wine and beer producers in the country and consolidate them into the sectors with what they have. They are doing a similar thing in education, they just made their first acquisition on automotive services, and they made the first acquisition in digital marketing.

[00:17:53] Steve Gorelik: So, what they are saying is that we have access to cheaper capital. We can deploy it in better ways than what a lot of you guys can. So, we are going to be very opportunistic. If we see a good opportunity to buy, we are gonna buy. If we are gonna see better opportunities in our shares, we are gonna buy shares. But meanwhile, we have all these different projects that we must spend money on.

Georgia Capital – expected NAV growth

[00:18:18] Steve Gorelik: Putting all this together, we have a current NAV of 50 GEL per share, and it is trading at about a 25% discount to that. By 2024, the NAV should be over 200 GEL per share. So, it should quadruple, which gives you a CAGR of about 35%. We have no view of where the discount should be. I mean, if you look at where the holding companies trade, 25% usually sounds about right. We think that these guys are good capital allocators, but you could say the same thing about XOR or any other company. And it is not like those companies traded the premium to their sum of the parts, but we do think that 25% discount is about right. But meanwhile, you can get an incredibly good CAGR in this company from the way that they are investing capital over the next few years.

Q&A session

[00:19:05] Steve Gorelik: So, that is about it, and I have two minutes left. Thank you very much.

[00:19:14] Moderator 1: So, do we have some questions?

[00:19:19] Speaker 3: Isn’t China active in that market?

[00:19:22] Steve Gorelik: So, China and Georgia have a free trade agreement that just came up, it was signed a couple of years ago. The country is, to be honest with you, too small for China. So, when the Chinese want to deploy capital, they have a billion dollars to deploy. Georgia, it is a country of three and a half million people, you really cannot spend that amount of money on one thing. And to do what these guys are doing, where you spend 20 million here, 30 million there, 50 million there, most of the people from China are just simply not going to bother. But the relationship with China, because of the free trade agreement, is important. So, what people are doing is they are setting up manufacturing, for example, Israeli people from Israel setting up manufacturing in Georgia to sell to China.

So, the free trade agreement makes a lot of sense. It is important, but meanwhile, they are not competing with people from China for the assets that they are buying.

[00:20:22] Moderator 2: Any other questions?

[00:20:28] Speaker 4: Yes. I see that you project remarkably high returns.

[00:20:32] Steve Gorelik: Sure.

[00:20:33] Speaker 4: But I guess that most of them are nominal terms, right? So, is this the catch? What is the inflation in Georgia?

[00:20:44] Steve Gorelik: So, the inflation in Georgia right now is around 5%.

[00:20:47] Speaker 4: 5%? Okay.

[00:20:48] Steve Gorelik: Yes. And so, to the other point of what you are asking is what happens to the currency, because this is the returns in local currency, and the currency has been weakening about three to 4% on average, which reflects in the inflation. We think that right now, for several reasons, the currency is cheaper than it should be. So, it is a suitable time to buy Lari-earning assets if you must. But the important thing that a lot of the investments are doing…I have a couple of slides here on renewable energy.

So, these are like returns on invested capital based on PPAs and dollar terms with the government. So, for example, these returns are dollar-based and that is where they are gonna be spending a lot of the money that they must deploy. So, from this point of view, I do not think they are assuming any kind of Lari changes when they are putting in their numbers, but you are protected here. You are protected in a lot of the other places in how they earn their money.

[00:21:52] Moderator 1: Any other questions? Can I ask one question, then? The discount to NAV is 25%, is that like [00:22:01 inaudible] a discount because you also have a discount on the listed companies which you calculated, or is this just based on the market value of these firms?

[00:22:09] Steve Gorelik: So, half of…where is this slide?

So, half of the NAV is the list of companies, so that is where these companies are trading whenever I made the slide, a couple of weeks ago. The other half is what they estimate the value of their holdings to be, which if it was recently acquired, is based on acquisition price or most of it is an earnings multiple. So, the discount is to that value, not to what we think the fair value of these things is.

[00:22:45] Moderator 1: Okay. So, that would be an even greater discount?

[00:22:48] Steve Gorelik: I would agree with that.

[00:22:50] Moderator 1: Okay. Well, thank you very much.

[00:22:51] Steve Gorelik: Thank you.

Disclaimer

Finally, here is the disclaimer. Please check it out as this content is no advice and no recommendation!