Markel Annual Meeting 2026 Transcript

Read the full Markel Group Annual Meeting 2026 transcript (Markel Reunion 2026 transcript) covering Jana Partners, Markel Ventures, combined ratio recovery, social inflation, and the Berkshire Hathaway position.

Follow Tilman for more insights

Follow Tilman for more insights

Easily discover all the topics of this Markel Annual Meeting / Reunion 2026 – Transcript by clicking on the table of contents:

Executive Commentary & Key Takeaways

This is the full transcript of the Markel Annual Meeting 2026, also called Markel Reunion, held May 20, 2026. CEO Tom Gayner, Insurance CEO Simon Wilson, Ventures President Andrew Crowley, and CFO Brian Costanzo walk through Markel’s financial performance, the insurance underwriting turnaround and improving combined ratio, the exit from Global Reinsurance, and capital allocation across Markel Ventures.

The shareholder Q&A tackles the most-watched questions of the meeting: management’s response to the Jana Partners letter urging a sale of Markel Ventures, Markel’s large Berkshire Hathaway position after Warren Buffett’s retirement, and how Markel is underwriting climate risk and “social inflation”.

Start of the Markel Annual Meeting 2026 Transcript

[00:00:49] Start: The meeting starts with corporate intro video showcasing Lancing, AMF Bakery Systems, Havco Fusion Floor, EPI, Costa Farms, VSC Fire & Security, and Brahmin.

Opening Remarks and Reunion Overview (Markel Annual Meeting 2026 Transcript)

Welcome and Agenda

[00:06:41] Tom Gayner: Good afternoon. It is absolutely wonderful to see you here for our 2026 reunion – the Markel Group annual meeting, or as we say, the reunion. None of us actually came up with that name, “reunion.” We just heard you use the phrase pretty frequently. We do our best to listen and learn from others, hence the reunion became the crowdsourced name. So thank you very much for the idea.

Here is our agenda for today. I’m going to share just a few thoughts, and then Matt Johnson will soon present our Markel Style Award winners to associates selected by their peers for our highest honor. Following the style awards, your senior management team—including our CEO of Insurance Simon Wilson, our President of Markel Ventures Andrew Crowley, and our CFO Brian Costanzo—will join me on stage to present some financial highlights and opportunities. Then we’ll be here to answer your questions.

After your questions, we’ll take about a 10-minute break to prepare for our formal AGM, which will be conducted by our Chairman of the Board, Steve Markel. During that break, feel free to either remain here for the formal AGM or join us outside at the reception for some hospitality in the form of food, drink, and music. It’ll be right out that way.

Now, before we kick off the meeting, let me first welcome you all. I also want to take just a minute to thank some of the people that made today happen. A lot of work goes into preparing for the reunion, and I just want to take a minute to thank some of the people who have led that effort. Unfortunately, time and space keep me from being able to thank everyone, but I do want to specifically thank a few. First, I want to thank Tyler Brown. He has led the effort for the last three years in making this meeting special, and we would not be where we are today without his leadership. Tyler would be the first to say it’s a team sport, and he’s right. As such, I also want to thank Caroline Paul for her partnership with Tyler.

I’d also like to thank Cynthia Green, who leads events for our insurance business, for joining this effort, as well as her teammates Gretchen Nearburgger—who is succeeding Cynthia in that role—and Cara Mountain Wilman. I’d also like to thank a couple of all-around athletes, Cynthia Federman and Christina Mati, for their crucial contributions to anything and everything that comes up in all matters reunion. And finally, I’d like to thank Lynn Blevins, who captains the many Markel volunteers who shepherd us through all of the aspects of this meeting—from planning to helping us know where to find a bathroom, a bite to eat, or a place to park. Thank you all for the work you do.

The Purpose and Purpose-Driven Philosophy of Markel

[00:10:20] Tom Gayner: In 1986, when Markel went public, Alan Kirshner, along with Tony and Steve Markel, penned our company’s creedal statement of values: the Markel Style. Those 214 words will forever be the philosophical and cultural lynchpin of your company. The Markel Style establishes the foundation of how the company approaches its business and long-term decision-making. It guides how we allocate capital and serve all of our constituents. We are not perfect. We’re human. But the Markel Style remains as a constant north star.

That’s important because Markel Group today is more than 22,000 people. We’re a decentralized system of exceptional leaders and teams operating market-leading businesses across an array of industries. We believe in autonomy and accountability. Our creed, as stated in the Markel Style, keeps all of us grounded in our common values and moving forward together as one team.

In its own way, the Markel Style addresses the question: what is the purpose of a company? We believe it is to serve. We work every day to serve our customers, to serve our fellow associates, and to serve our shareholders forever and right now.

First, the Markel Group serves its customers. We pay insurance claims for storm damage, ocean shipping losses, professional liability claims, and other complex specialized risks. We also provide essential products and services such as bakery equipment, pre-cast concrete structures, and concierge medical services, just to name a few. Doing so day after day, week after week, month after month, year after year, serving our customers dependably and reliably over time both fulfills our purpose and builds value. There are no shortcuts. There is no finish line. The journey is the destination.

Second, the Markel Group serves its associates by emphasizing culture, autonomy, decentralized decision-making, respect for expertise, and opportunities to build long-term careers. We want associates to come here and stay. We want them to tell their family, friends, and their personal networks to join us as well. We seek to create a home that attracts people with equal parts of talent and integrity. We cherish the relationships that we build throughout your company.

Third, the Markel Group serves its shareholders by focusing on building the long-term value of each share you own. We want shareholders to relentlessly compound their savings and build wealth, and we have a long-term record of doing so. From 1986 to the present, our stock price compounded at roughly 15%. That compounding record puts us in the upper tiers of public companies, and it has been true for decades, not just the last few minutes. That compounding has put kids through college, funded retirements, and created the ability to give and contribute to communities and create good.

Personally, I grew up in the shadows of Philadelphia, the center of Quakerism in the US. As the old joke around Philly says, “The Quakers came to America to do good, and they did well.” So is Markel. I want to thank you as fellow shareholders for helping us continue this path, which does so much good for so many.

Well, that all speaks to why we exist. In a few moments, Simon, Andrew, and I will tackle the question: how are we doing? We’ll review some specific financial measurements to describe that part of the answer. We’ll also talk a bit about our future and the opportunities we see. As is always the case, I think it’s important to remember that the numbers are the output. The input is the Markel Style and our system. Living our values and serving each of you each and every day is how the magic happens. That is the system and the process which underlies our financial performance. We run Markel with the mindset of a good farmer. A good farmer farms for the next generation, not just the current crop. We’re building your company for forever and right now. I’m grateful for the chance to help build Markel. It’s a joy to do so.

Before I turn over things to Matt Johnson, give me just a minute to say a word or two about Matt. There’s so much to say about Matt that I’m going to limit myself just to words that begin with the letter C. First off—and we’ve got a picture of Matt getting ready backstage—creative. Matt is creative in every possible way. He sees into the future and imagines possibilities ahead of the rest of us. Connector: he connects people and ideas all around the Markel Group. He has done so throughout our insurance and ventures businesses, and he has done so all around the world. COVID: Matt played a critical role during the times of change and reconfiguration driven by COVID. He helped so many of us figure out how to operate in a different way and to be able to continue to productively go about our work. Consultant: recently, Matt stepped back just a bit from his non-stop pace as a full-time associate of Markel and took on the role of consultant to remain connected and to continue to help us craft and tell the story of Markel. I’m so grateful for all that Matt has done over so many years. With that, please welcome Matt Johnson to the stage, and enjoy this video about this year’s Markel Style winners.

Follow Tilman for more insights

Follow Tilman for more insights

The Markel Style Awards (Markel Reunion 2026 Transcript)

[00:16:54] [Video Presentation – Style Awards Introduction] Videos tracking historical company documents and introducing the core philosophies of the Markel Style are shown.

[00:18:09] Matt Johnson: All right, how is everybody doing today? They didn’t tell me they were going to do that video setup, so I feel like it’s payback for all the times I put these style award winners’ faces on the jumbotron. Thank you very much, Tom, that means quite a lot.

It is my honor to present to you this year’s winners of the Markel Style Award. Every year we give this award to people who embody the values of the Markel Style with their actions and not just their words. Our winners were selected from the more than 22,000 people who are part of our family of companies. We think it’s important to celebrate them because they represent the best of who we are and what we can be. As I read through the names of this year’s winners, I’ll stop along the way to tell a few stories to illustrate the caliber and character of these individuals. Are you ready to meet the winners of the Markel Style Award? All right then, let’s do it.

The first group of winners: Zach Bell, Kate Gardner, Ruben Otero, Stacy Pridmore, Alysia Furbert Adams, and Jamie Siki. Over 20 years ago, Jaime worked at a daycare that shared a parking lot with Markel. She had been in that job for about eight years and was looking for more opportunity in her career. It just so happened that one of the parents at the daycare was a woman named Kimberly LeFortune. Is Kimberly here today, by the way? The astute among you will recognize that name because Kimberly won a style award last year. She was so impressed with Jamie at the daycare that she started printing out open job positions to encourage Jaime to apply. Jaime eventually did, and she got a job in the file room in 2005. She has been promoted multiple times since and she now leads a team of underwriting support specialists. That is the spirit of teamwork.

[00:20:15] Matt Johnson: Next group: Jess Richardson, Keith Hill, Claire Willet, Nick Gibson, Matt Scott, and Janette Anselmo. You haven’t even heard her story yet, and there is already applause! Janette went into healthcare to follow in the footsteps of her grandmother. When she got out of college, she went to work for an anesthesia practice. She really came to like that company and its culture, but a few years later, that company was acquired by a private equity firm. There were layoffs, leadership changes, and restructures, and the company eventually became a shell of what it once was. As this was happening, Janette was actually earning her MBA. It was a professor in that program who connected her with what would become her dream job. She got the opportunity to lead a small concierge medical practice in Charlotte, North Carolina called Signature Healthcare. For the next 15 years, she and the team built that into an incredible organization.

Then Janette got a call last year that she didn’t necessarily want to receive. She heard from the owners of Signature that they were considering a sale to a company called PartnerMD, which was part of a large global corporation called Markel Group. Janette feared the worst. She feared that a deal like this could kill the culture that she and the team had worked so hard to create over all those years. But it really wasn’t her decision to make. Janette took a meeting with Zach Smith, who is the CEO of PartnerMD. Zach said all of the right things, and at the end of the meeting, he promised her that PartnerMD would take care of what she and the team had built at Signature. Despite her apprehensions, Janette moved mountains to make that deal a success, and she did not lose a single person through that transaction. You can look at this and say Zach and PartnerMD kept their promise, and Janette, you kept your promise too. Both organizations are stronger for it. That is the spirit of teamwork.

[00:22:28] Matt Johnson: The final group of winners: Alan Pilcow, Nikolai Stoyoff, Nate Wells, Jock Maro, Billy Mosby, and Isaac Dunston. Last but not least, Isaac. Isaac was working as a server in various restaurants after he graduated from high school. He did that for a few years until a family friend who worked at Markel told him that he might want to apply for a job with the customer service team. Isaac did and he got a job in the call center, despite the fact that he actually didn’t really like talking on the phone at the time. But he stuck it out with that job, eventually led a team in that call center, and now he’s an underwriter in our personal lines business. We love a story like this because one of the pillars of the Markel Style, as Tom said, is the idea that when you join one of our companies, you join a place where you can reach your full potential.

When you want to know what Isaac is all about, there is so much more to the story. For that, we need to go back to 2018. Isaac lives in Waukesha County, right outside Milwaukee, and he was alarmed to see that more and more people were struggling financially. He wanted to help out, but he only had about $200 to give, and he couldn’t find an existing organization providing rapid, direct financial support to neighbors in need. So Isaac decided to do something about it. He started his own nonprofit called Simply Helping People. It was based on the relatively simple premise that you could pair generous donors directly with neighbors in need. That’s what they’ve been doing since 2018.

Let me tell you just a few stories about the work they’ve done. A woman going through cancer treatment needed help covering basic expenses, and Simply Helping People provided a grant. A family had a kitchen fire and needed help getting back on their feet; Simply Helping People provided a grant. Another neighbor hit a deer, only had liability coverage, and couldn’t fund the car repairs to get to work; Simply Helping People provided a grant. And this last one is a uniquely Wisconsin story: a woman’s car was hit by a snowplow. Luckily she was okay, but the car was not, and she needed help covering expenses. Isaac’s organization provided a grant. A year later, Isaac gets a phone call from that same woman. She says, “Hey Isaac, are you still doing that nonprofit thing?” He says, “Yeah.” She says, “Well, I’ve been saving for the last year, and I’d like to pay that money back.” And that’s what she did.

As Isaac was telling me these stories, I became immensely grateful that people like him exist because they show us what’s most important in life: simply helping people. That’s what the spirit of teamwork is all about, and that’s what these people do every single day. Please join me in congratulating this year’s winners of the Markel Style Awards.

Financial Performance and Segment Reviews (Markel Reunion 2026 Transcript)

Group Consolidated Financial Performance Review

[00:25:41] Tom Gayner: At this point, we’ve got some updates with slides, and Andrew, Simon, and I will go through a few things to give you an update on our financial performance over the last 15 years. Brian is here to answer any tough questions that none of us are prepared to do, and we might just call on him anyway.

First off, here is the disclosure statement that happens at the front of any financial presentation or conference call—the SEC equivalent of the Miranda warning. Anything we say can and will be used against us, but please don’t do that. We’re giving you the forward-looking disclosures. We had a contest where we were going to offer somebody the chance to read this to everybody, but nobody chose to participate, so you’ll just have to read it for yourself.

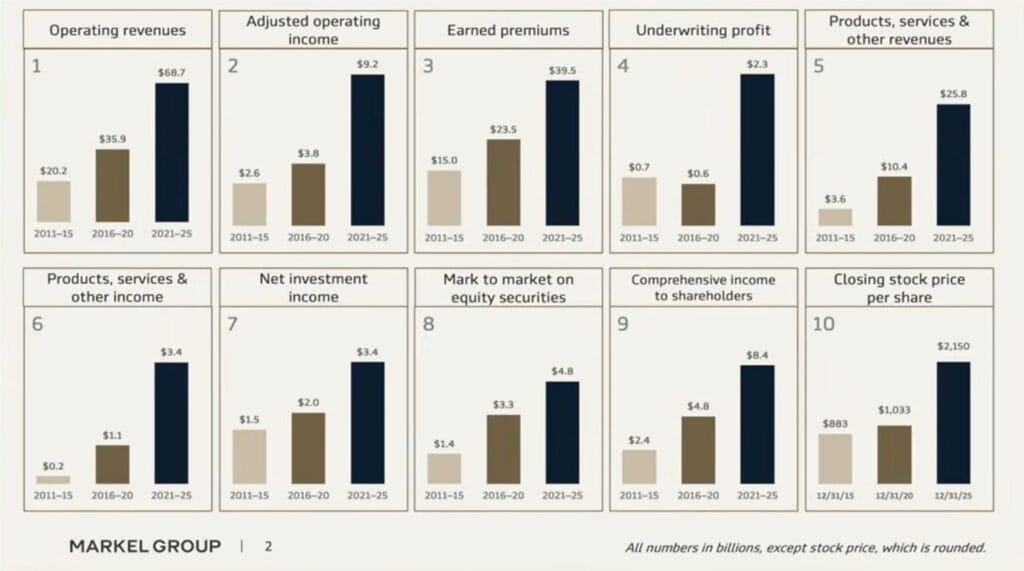

We’ll go into the slides. One of my colleagues noted, “Gosh, this is a busy slide, and boy, there’s a lot of stuff up there,” wondering how much time I was going to spend talking about it. In the annual report, I talk about five-year buckets, and we talk about being a long-term company all the time. I think five years is sort of the minimum amount of time required to tell whether people really know what they’re doing or are good at their job. You have to give people time to let them do the job you’ve asked them to do. On page four of the annual report, in the letter there, I talk about five-year buckets. This chart and these numbers are exactly from that letter.

There are 10 boxes within there, all the way through 10, and I’m going to talk about each of them. Before I ask for a few minutes of your time, there was one little math computation I did when I was thinking about this. This represents 15 years of time at Markel. Let’s just say we have 22,000 people and they work 2,000 hours a year. 15 times 22,000 times 2,000 is 660 million man-hours of time being represented on this single slide. If you wouldn’t mind just giving me about eight minutes out of those 660 million man-hours, I’d deeply appreciate that.

- Box Number 1 (Operating Revenues): Over the years, you can see that in those five-year buckets, the revenues have gone from $20 billion to $36 billion to $66 billion. Let’s just say it goes from a number to a bigger number to an even bigger number. It’s accurate and directionally correct, which is one of my hallmark phrases. That represents billions of dollars of votes from customers who are choosing to do business with us, buying what we are selling them in terms of products and services. There’s nothing we can do without starting with customers buying from us.

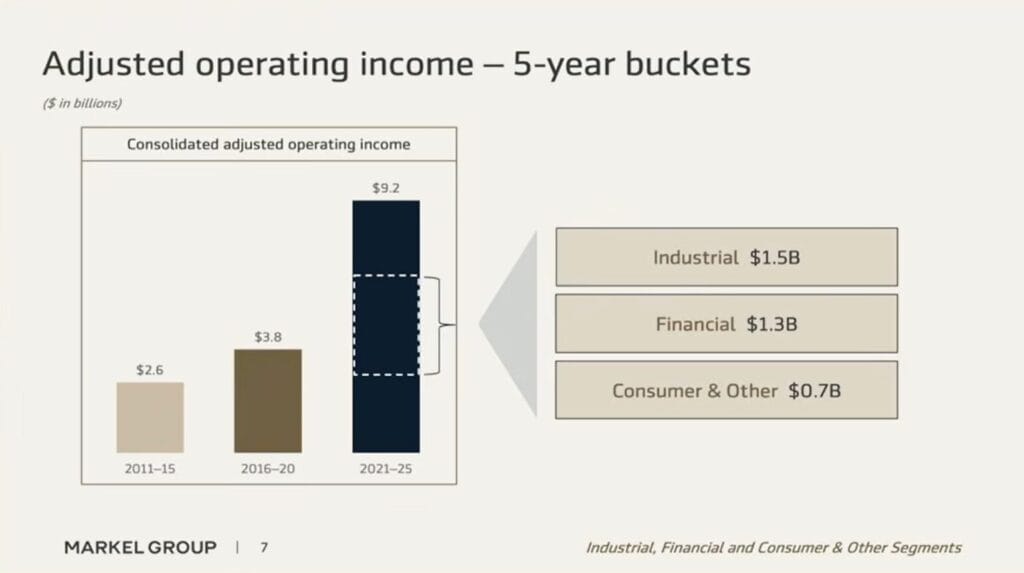

- Box Number 2 (Adjusted Operating Income): This is where it starts to matter—the adjusted operating income that we’ve earned from those revenues and sales. You can see it has gone from $2.6 billion to a bigger number, to an even bigger number. We’ll break down that slide in a little bit.

- Box Number 3 (Earned Premiums): Our core legacy business is insurance. Breaking down the total a little bit to the earned premium numbers, you can see the premium growth that has happened in those five-year buckets over the years. Again, it shows the same delightful pattern of a big number, a bigger number, and an even bigger number.

- Box Number 4 (Underwriting Profit): This is where it starts to get interesting. You can see in the first bucket (the 2011 to 2015 timeframe), there was $700 million of underwriting profit. In the next five-year timeframe, there was $600 million. That is lower, despite the fact that premiums went up significantly. That was a foul period for Markel. As I cited when we first talked, we are not perfect. We’re human. We make mistakes and get off track sometimes, but we’re honest about that. We recognize it, figure out what we need to do differently, and then go about the hard business of correcting it and making it better. We always want to communicate candidly with you, and I think those five-year buckets convey very important information.

- Box Number 5 & 6 (Markel Ventures Revenue and Income): For products, services, and other revenues, the Markel Ventures set shows an amazing growth story from a small number to a bigger number to a much bigger number—a very rapid rate of growth. Looking at box number six, the products, services, and other income came along at an even faster rate of growth. Andrew will break that down for us in a moment.

- Box Number 7 (Net Investment Income): One of the features of the Markel Group is that as we operate the insurance business and other operations, they produce cash. That cash gets invested into high-quality fixed-income securities and equity securities, producing a recurring stream of interest and dividend income. You can see the same pattern emerging of a big number to a bigger number to an even bigger number.

- Box Number 8 (Mark-to-Market and Equity Securities): Tying this back to box number two where we use the word “adjusted”—Andrew helps me out with a lot of due diligence issues. Whenever we see a presentation or slide that has the word “adjusted,” what he does is “de-adjust” it and go back to the original world. What were we adjusting for in that adjusted operating income? We were taking out the short-term volatility that happens in the equity markets on any given period. But you can see over longer periods of time—and five years is long enough—we’ve made good money investing in equity securities. Again, the total returns show a big number to a bigger number to an even bigger number pattern.

- Box Number 9 (Comprehensive Income to Shareholders): Netting all of those things together, you get comprehensive income to shareholders going from $2.4 billion to a meaningfully bigger number.

- Box Number 10 (Market Value / Share Price): This concludes with share price performance. With some time delays and short-term volatility, the market generally figures it out. When we make more money, the value per share of stock tends to recognize that over time with some lags, as seen in the long-term rate of growth in the share price.

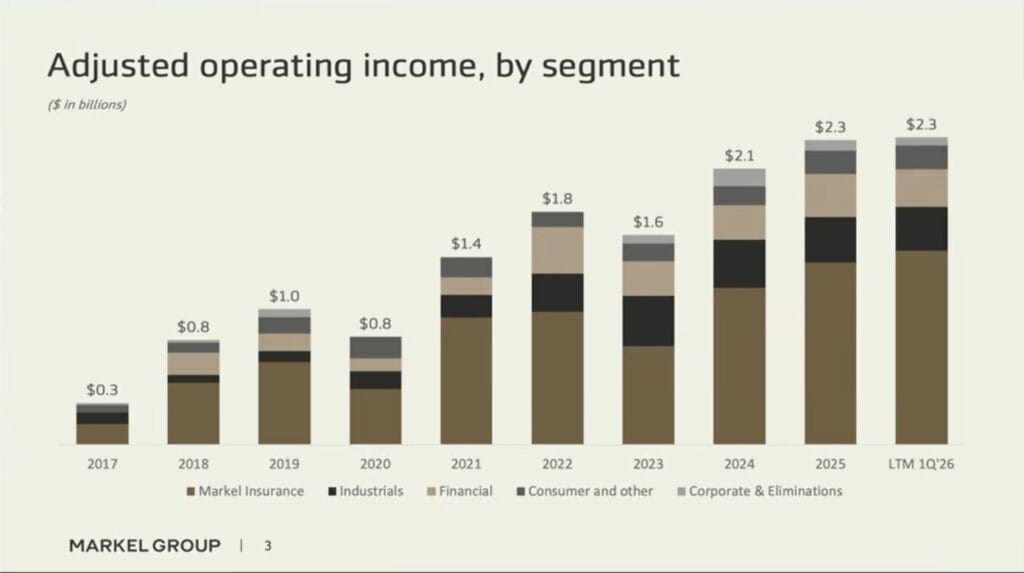

[00:32:50] Tom Gayner: As I said, I do want to dive into the adjusted operating income, and the point I want to make here is the degree to which the diverse collection and array of businesses we have was really quite helpful. You can see the insurance segment (the lower bar) from 2018 through 2020 was flatter to down a little bit. It started going up in ’21, but during that six-year era, we really didn’t have a breakout or the up-and-to-the-right patterns that we would normally hope to see in our insurance operations. Simon will talk about that in a minute.

While that was taking place, the other businesses—the Ventures set of businesses—were growing quite nicely. Not only did they contribute income and cash, but they also contributed resiliency and the ability to take a long-term view of things. They gave us the ability to make the right long-term decisions, to not take shortcuts, and to do things the right way. It’s much easier to do that with a full bank account than an empty one, and the resilience and diversity that comes from the array of businesses we own is seen clearly there. What you’re also starting to see as we go into ’24, ’25, and ’26 is that we are back on track. Simon will talk about what’s going on in the insurance business and things that have changed under his leadership, but it’s certainly getting to a pretty good place, and we’ve had continued growth in the Markel Ventures collection of businesses as well.

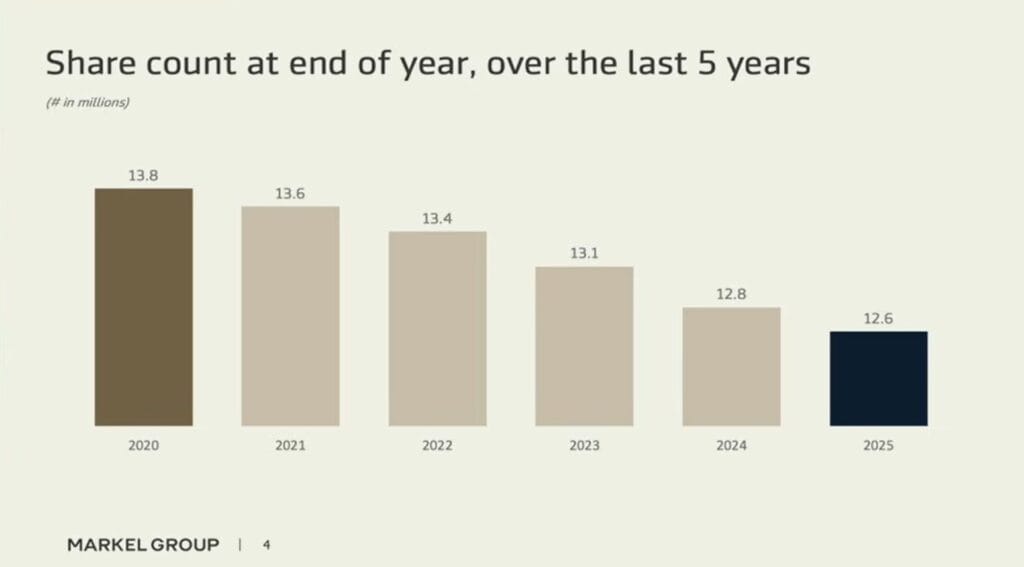

[00:34:16] Tom Gayner: By the way, all of those good things that are going on financially are about building the intrinsic value of each share of Markel stock that you own. Over the course of the last five years, we’ve bought back about 10% of our shares because we allocate our capital to where it has the highest and best use, as best we can find it. We are able to fund the organic growth of our existing businesses, be they insurance or non-insurance. We’re able to make acquisitions of insurance and non-insurance businesses. We buy publicly traded securities, which you saw reflected in the growth of net investment income and the value of the portfolio. We also pencil out the math to see how our stock is trading relative to what we think the value is. As you’ll see, actions speak louder than words, and we have repurchased about 10% of our shares at this point.

[00:35:11] Tom Gayner: How did all this happen? What are the components that made this reality come to be?

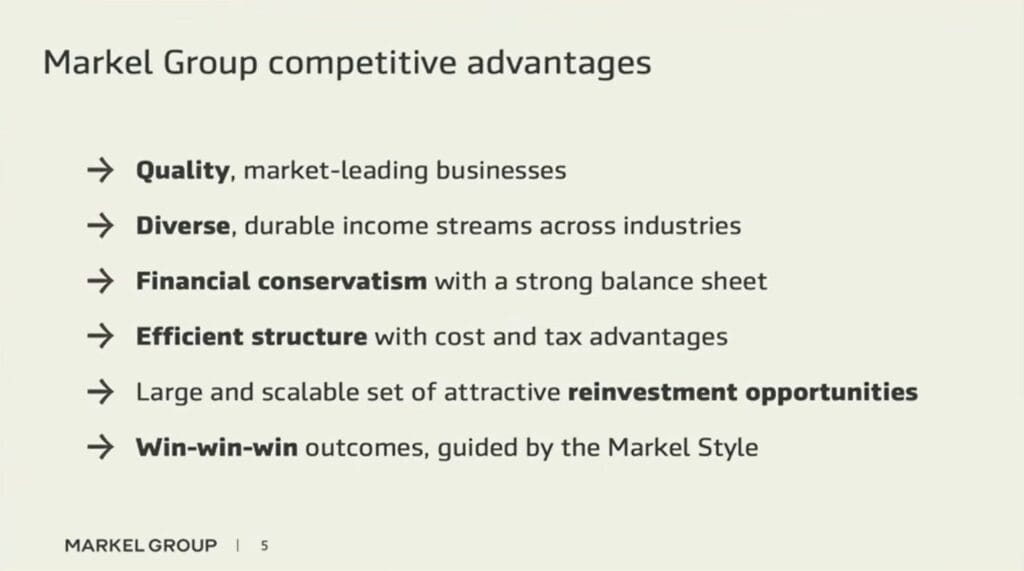

- Quality Businesses: These are market leaders. Simon will talk about his dream of building one of the world’s premier specialty insurance companies; it’s a spectacular business. The array of businesses within Markel Ventures—the leading grower of indoor houseplants, the leading car carrier trailer manufacturing business, trailer flooring, industrial gases—are all leading businesses in the niches they operate. They persistently serve their customers and associates well and compound value over time.

- Diversification: We have an array of these businesses. At any given time, one business is going to be doing better than another. Different economic cycles will apply to different businesses at different points in time. By virtue of the fact that we have fingers in a lot of different pies, there’s always plenty of pie, and that’s a good thing.

- Financial Conservatism: We operate in a fiercely conservative way. We don’t excessively lever the balance sheet. We keep the debt low, and again, that aids us in keeping long-term time horizons and thinking about things in a long-term way, rather than being under the gun of a current interest bill or an upcoming debt maturity.

- Efficient Structure: I think this is extraordinarily important and it’s one of the reasons why Markel has done so well and will continue to do well. There are three levels of very important cost savings—two of which you can see, and one of which is not immediately visible but is real nonetheless.

- Tax Efficiency: When we make money anywhere in the world in any business, we pay the tax on that. That is the appropriate thing to do as law-abiding citizens. However, if we distributed that money out in the form of dividends to you as a taxable shareholder, you would pay another layer of tax. By keeping the capital inside the business, we pay one level of tax at the corporate layer, allowing us to invest full after-tax proceeds, as opposed to taxable shareholders who would be reinvesting after another layer of tax. That is a very important structural advantage to the architecture of the Markel Group at large.

- Cutting Out Fees: We cut out a lot of fees. If we distribute capital and then need to get capital back from Wall Street intermediaries when we have a new idea, those intermediaries can’t and shouldn’t work for free. There are a lot of fees and commissions attached to moving capital in and out of an organization. As the old ads would say, we cut out the middleman and pass the savings on to you. That’s a vital level of cost efficiency.

- Explicit Reporting: Andrew highlighted this point to me and he’s exactly right. Every penny of what we spend in terms of management salaries, employee compensation, and incentive compensation flows explicitly through our income statements each and every period. By contrast, if you look at a private equity-backed organization, oftentimes some of the biggest chunks of management compensation don’t come year-by-year through the income statement; they come when the business is sold via an exit payout or bonus. Those expenses never actually flow through the operational financial statements of those companies, making it a hidden difference. Those costs are still real and absorbed implicitly by the investors. In the case of the Markel Group, you’re getting explicit reporting of everything it costs to run your business, which creates a huge tailwind of efficiency to help compound your capital.

- Reinvestment Skills: By virtue of the fact that we’ve operated in both insurance, non-insurance businesses, and public markets for decades—almost a century—we’ve developed the skills and abilities to reinvest that money and put it to work at good rates of return over time. Finally, in keeping with the Markel Style, it’s truly a win-win-win system where our customers win, our employees win, and our shareholders win.

With that, let me turn it over to my partner Andrew to break things down in those five-year buckets a little bit more in the realm of Ventures.

Markel Ventures Segment Review

[00:40:02] Andrew Crowley: Appreciate it, Tom. Can we hop to the next slide?

(Graphics shown on screen: Markel Ventures segment table from the 10-K, showing Adjusted Operating Income and Total Capital by segment: Industrial, Consumer, and Financial. Chart/Graphic Marker: 00:40:07 to 00:43:52)

I will say, while we’re switching over here, in Tom’s defense on the numbers, I’ve never seen such big numbers show up so small on a screen. Despite seeing billions and billions, they were quite small for us up here on stage, though a little bigger for you all behind us. Tom talked about being directionally correct. One of the things that I think we work through over time is that I like to be maybe a little more magnitudinally correct. One thing I noticed in the five-year buckets as they went across is that from the middle bucket to the most recent bucket, on average, those figures doubled or more than doubled. For those financial minds in the room, you know the rule of 72 and can quickly see that represents mid-teens compounding over that period. That’s a really, really strong number, adding some magnitude to the direction.

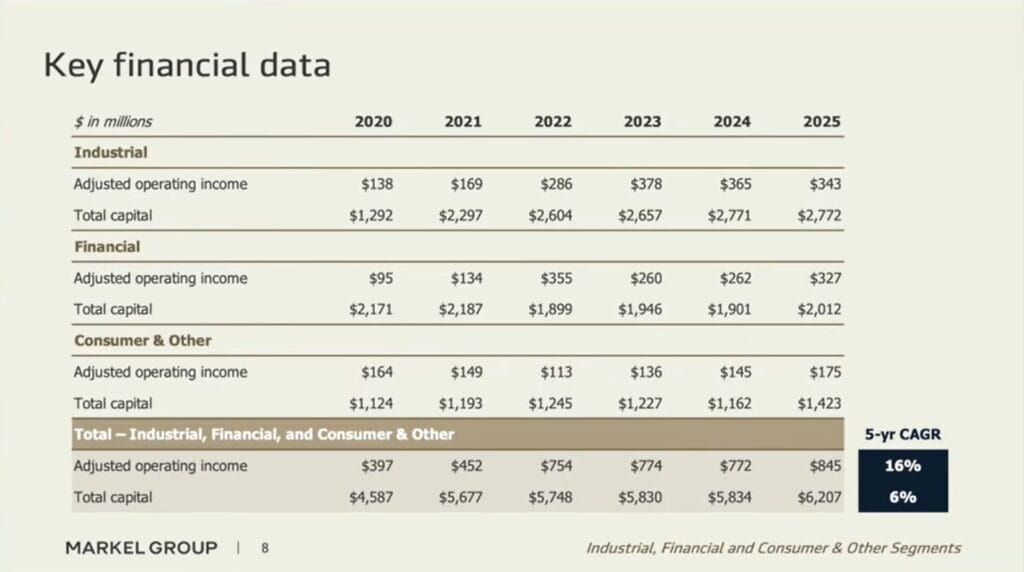

Where are we going to spend a few minutes now? My role at Markel is predominantly oriented to the businesses we report to you through our industrial, consumer, and financial segments in our updated financial disclosures. I want to take a few minutes and talk about some of the patterns I see, particularly related to performance, that you can track in the information we share. We’ll look at the performance over the last five years, talk a little bit about why and what the key elements to that performance are, and then discuss why I think this is systemic—this isn’t just a recent phenomenon, it is built into the DNA of Markel Group. On this slide, you see the consolidated adjusted operating income that Tom showed earlier, along with the total numbers for each of those divisions.

We talk a lot at Markel about relentlessly compounding your capital over time. My early training in finance pointed out something that holds true in any timeframe: growing earnings at a rate that is at or above the rate of capital growth is a strong indicator of your ability to increase returns on capital and thus shareholder returns over time. It’s a lens that when we’re underwriting a new business or looking at our own existing operations, I always want to stare at.

On the screen here, you’ll see an excerpt from the KPI table that we put in our most recent 10-K. Thank you to the team that helped pull that project along and update our disclosures; it was a heavy lift, but the valuable information is right here. What you see is adjusted operating income by segment as well as total capital by segment. In the bottom row, you’ll see the three segments added together. Next to that, you see a five-year CAGR, which shows that the earnings power of these businesses grew 16% per year on average over the last five years. Capital, on the other hand, grew at 6%. That ratio is about two and a half to one. Earnings grew at a rate two and a half times the rate of capital. Without doing a whole lot of math, that tells me that we’re doing significantly better today than we were five years ago. It’s just a simple way to keep track of that discipline over time. It won’t happen every single year and it may not always happen to that magnitude, but it’s something we’re really proud of our businesses for achieving.

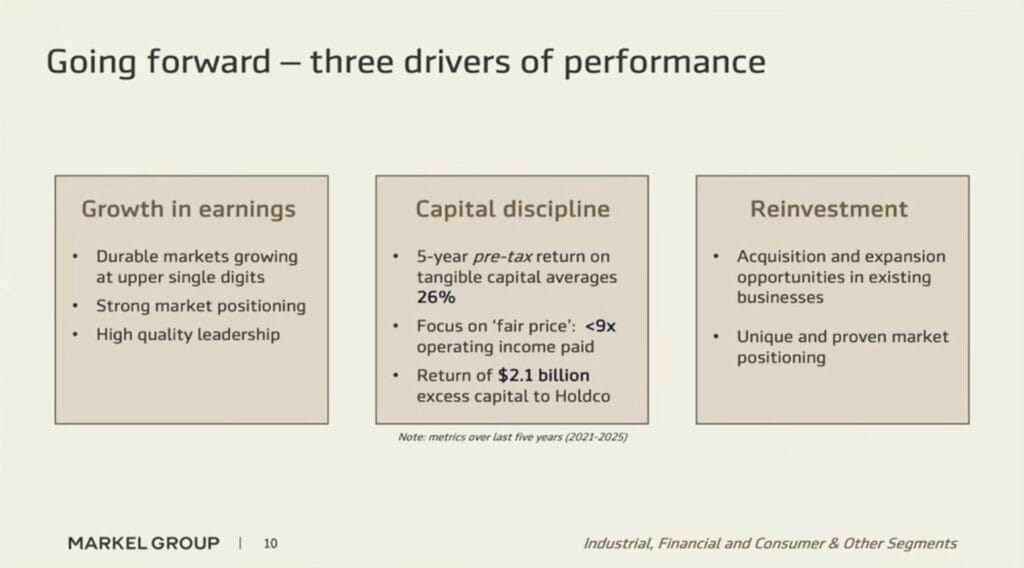

[00:43:53] Andrew Crowley: Let’s talk a little bit about what drove that. First thing is you have to grow earnings; you can’t just do that by decreasing capital. There are a lot of ways to think about earnings growth, but one area where we provide information is around the organic growth of the businesses in our family. It’s a question we get a lot. Tyler Brown and I have a healthy debate about the value of organic growth, and at the end of the day, there is immense value in understanding if the core businesses at Markel Group are growing natively. If you looked at all the numbers in that grid and took an average annual organic growth rate, you’d see it was 8% over the last five years. That’s a big number. In any one period, you might see a specific segment grow 15% and you might see another segment shrink 3%—that’s the natural behavior of unmanipulated businesses rather than artificial constraints put in place to hit short-term targets. But averaging 8% organic growth over the last five years is excellent.

The next point is capital discipline, and this is something that our system is designed to help our leaders maintain. We constantly talk about large capital decisions, excess cash, where that cash sits, and whether it’s truly needed to run local operations. Every business within our family is well-capitalized, but they also generate a lot of cash. When that cash isn’t needed in that individual business, the goal is simple: send it up to the holding company. Everything that we do about capital allocation requires the generation of cash and the ability to redeploy it centrally. Over the last five years, businesses across these three segments generated even more cash than this, but they sent $2.1 billion net back up to the holding company. It’s a fantastic number.

Just growing earnings and having capital discipline still isn’t enough; we still have to find intelligent ways to put that capital to work. To put one number out there, over the last five years, we’ve invested $1.3 billion into acquisitions. Just doing acquisitions blindly isn’t enough—you have to pair all three of these things together. When you ask how in the world we grew capital at such a small fraction and earnings at such a large fraction (two and a half times the rate over five years), these are the three key operational elements.

[00:45:45] Andrew Crowley: They’re not just a feature of the last five years. Let’s talk about what’s behind that and why I think it will continue.

- Durable Markets: On growing earnings, Tom mentioned this in his commentary around our system. Our businesses operate in durable, essential markets that are growing at low-to-mid single digits natively, but they grow consistently over time. Anytime we talk about a business in our family or look at a prospective acquisition, the first thing we ask is: does it have a structural headwind or tailwind? Is the wind going to be at our back, or are we going to be fighting every day just to stay in the same place? We are very blessed to have businesses operating in a host of markets that possess secular tailwinds, whether it’s fire protection, specialized agricultural products, concierge medicine, or industrial services.

- Market Leadership: Second, our businesses are market leaders. It’s nice to have that little blue ribbon saying you’re the market leader, but what does it actually enable pragmatically? It enables structural cost advantages, pricing power, innovation at scale, and the ability to recruit and retain incredible talent, some of whom you’ve met today. There are so many structural advantages that come with market leadership. We have a strong desire to lead the niches we’re in, and our businesses do a great job maintaining that edge.

- Incredible Leadership: I was at a university not too long ago—there’s actually a student in the room from that class, and I hope he doesn’t mind me sharing—but we were talking about leadership. One of the comments from a prior case study was that Apple is such a good business it could be run by a ham sandwich. I don’t know that I would call Tim Cook a ham sandwich; I think the guy is probably one of the top five CEOs of the last 20 years, and his predecessor was up there as well. Our businesses are absolutely not run by ham sandwiches. These are incredible leaders. I get choked up thinking about it. You got to see Simon earlier, and you all got a lot of laughs from Ross. I wish I had Ross up here now, it’d be a lot more fun. Kyle, and I could go on and on. We’ve got many leaders in the room, but these businesses are well-run by great people, and this system natively attracts them. Anytime we have to make a leadership change or someone retires, we hold our breath. We worry about who’s next and whether we can keep it going. What I can comfortably tell you is that over the 15 years I’ve been here, every single time we go through a transition, we get stronger. This system is built to attract high-quality leaders.

- Capital Returns and Pricing Discipline: Look at pre-tax returns on tangible capital. What it really means is if you rip out the non-cash purchase accounting intangibles when we buy a business, how is that business performing on its inherent operational capital? Over the last five years, that number averaged roughly 25% to 26%. That’s a remarkably strong number. When we reinvest capital organically, we’re reinvesting at a high rate of return. We always focus on a fair price. Tom always talks about our four lenses, and fair price is the fourth lens. Fair price means that when you walk away from the negotiation table, you’re excited but you’re also a little uncomfortable, and so is the seller. To quantify that discipline, over the last five years, when we’ve made an acquisition, the aggregate multiple has been less than nine times operating income. That’s in a world where private market prices have continued to skyrocket. We’ve maintained our discipline, seeking high structural quality while remaining absolutely disciplined around price. As mentioned, we returned $2.1 billion of cash to the holding company, and we’ll continue to do that over time. If cash is useful in a business, let’s keep it there; if it’s not, let’s move it up so we can reinvest it elsewhere.

- Deal Flow and Reputation: We see a massive number of opportunities. It’s a real privilege to have you all as aligned partners, to have the leaders of our companies, and to have a select group of intermediaries who share high-quality proprietary ideas with us. Over time, we might review 500 opportunities in the course of a single year, and that structural deal flow is an important part of our ability to discern what constitutes an elite home for your capital. We’ve been at this for 21 years on the Markel Ventures side. That’s not that long compared to the near century of Markel Group’s history, but in the middle-market corporate world, it’s a reasonable amount of time. I think we’ve proven to have a completely unique, highly differentiated model out there. It’s not for every seller, but there are founders, leaders, and families who look to us as a unique permanent partner. When that’s the case, we’re set up for structural success. I want to stay focused on that and continue to perpetuate our reputation in that area. It’s an intangible asset that doesn’t show up on the balance sheet—Brian won’t let us capitalize it—but I do think we’ve got a wonderful model that will help us keep going over time.

With that, I’ll hand it over to Simon.

Markel Insurance Segment Review

[00:50:41] Simon Wilson: Thanks, Andrew. It’s fantastic to sit up here and look at some of those numbers. A lot of the things that you guys have been doing across the broader group have given me the structural opportunity over the last year or so to be able to make some of the hard operational changes that we’re going to talk about in this next section.

On to insurance. I can feel people on the edge of their seats in this auditorium. This is a phrase that we kicked off the year with in 2026: we call it “Building to Win.” I like it because it really captures the essence of our actions. Every single decision that we’ve been making over the past 12 to 15 months has been intentionally designed to build an organization—or rebuild an organization—that can go out into the marketplace and start winning at a high level again. Everything I’m going to talk about today centers around those concepts of building and winning.

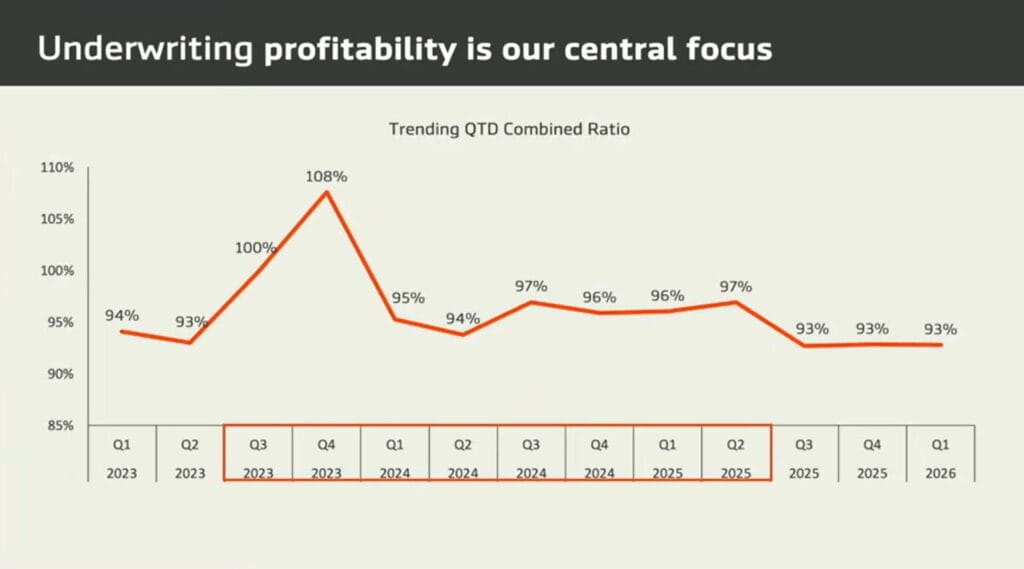

At the very core of my job within this organization and this system is to produce consistent, predictable underwriting profits. Without that gold standard at the center of what we’re doing here, the entire compounding engine doesn’t work to the degree that it should. I did this in Omaha last year, but I want to be completely honest and transparent with people about where we’ve stood over the last three years or so of underwriting. You can see that boxed off on the screen—this is our combined ratio over time on a quarterly basis. For those of you who follow insurance, the lower the score, the better. If you’re over 100, you’re actually writing at an underwriting loss. You can see in that period from Q3 2023 to Q2 2025—so a full two-year period—we were pretty marginal, at times loss-making within the insurance business.

There was a lot going on underneath the covers there. It wasn’t that specific period of time that was natively the problem; the seeds were sown long before that in many respects. A lot of what we have had to do to get back to consistent underwriting profitability is really hard, grinding work on our portfolio risk management. Let me share just a few things that we’ve done on that underwriting portfolio:

- In the casualty business in the US, we’ve significantly reduced the proportion of construction risk that we’re underwriting.

- We’ve decreased our average line size quite significantly across the board to limit volatility.

- We have completely exited our public D&O (Directors and Officers) underwriting in the US, which was roughly a $200 million line of business.

- We completely came out of Collateral Protection Insurance (CPI), which was an operational misstep.

- We have completely exited Global Reinsurance (Global Re).

Now, a lot of those decisions that we made at the time were correct economic ones. But if you go talk to brokers about lines of business that you’re now stepping away from—lines they heavily relied on you to underwrite—that is not a popular thing to do. It’s hard yards to go and execute those restructurings. But this is not a popularity contest; it’s a profitability contest, and that’s really important for our teams to understand.

As we’ve seen the improvement in the recent quarters—the last three quarters have actually been slightly sub-93% in each quarter—we can see the green shoots emerging from those difficult decisions that we had to make over the course of the last 18 months. It’s hard yards. For those of you on the insurance side of the business in the audience, that work was worth it and it will continue to be worth it. We have to keep going and producing these types of results for another three quarters, and another three quarters after that. I think we’ll get our “halo effect” back that Tom talks about quite a lot if we continue to consistently execute results like this.

You can do some good portfolio management by cutting things, and often that’s required—it’s like pruning in a garden. But you cannot cut your way to greatness. You have to do things to rejuvenate organic growth in an organization and to become a market leader again.

[00:54:26] Simon Wilson: Last year, I sat on stage and I talked a lot of talk. I was saying these are the things that we’re going to do, talking about P&Ls, reorganizing, and getting rid of complex matrix structures. Over the last 12 months, I think the team has really walked the walk, and I’ve picked the big six structural milestones that actually happened:

- The dreadful four-dimensional matrix structure in the US—which meant every single decision we were making on the underwriting side had to be done by an expansive committee—is gone. There is now detailed clarity on exactly who is responsible for what.

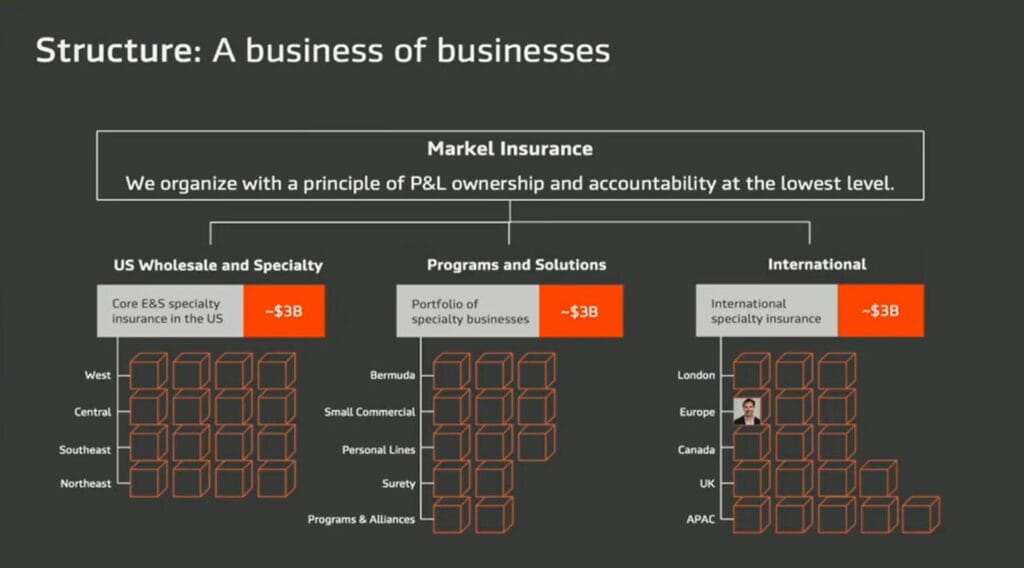

- We reorganized the entire global business into three clean divisions: Wholesale and Specialty, Programs and Solutions, and our International business. Each of them is led by a terrific leader: Wendy Hower, Alex Martin, and Andrew McMillan, respectively.

- Under those three divisions, we’ve established 14 business units, and every single one of those 14 business units has its own distinct, accountable P&L and a leader that sits squarely on top of it.

- All of our financial reporting and management information—thanks to massive efforts from Brian and his team—are now perfectly aligned to that new structure.

- The incentive compensation of the leaders who drive that new structure is now directly tied to those distinct P&Ls.

- We stepped away from the loss-making Global Re business, which represented $1.2 billion worth of gross written premium. Concurrently, 80% of the 2,200 people who used to work for the central, corporate part of our organization have now been decentralized and embedded directly into those 14 operational business units. They are now close to the business, close to the customers, and going to work every single day with winning on their minds. This massive amount of organizational change, on top of the portfolio changes, sets us up fantastically for 2026 and beyond.

[00:56:21] Simon Wilson: Let’s talk about a few core concepts and pillars that are going to drive our success over the next three to five years, and it all begins with strategy. In strategy, there are just two questions that you need to care about: the first is where to play, and the second is how to win. For a long time in the insurance business, we were fiddling around with lots of different things regarding where we wanted to play. But our heartland—the place where we built this business—is in specialty insurance. That is a $700 billion to $800 billion marketplace globally. We write $9.5 billion of that total. There is ample road to run in the space where we can make a structural difference, and we should be completely confident in attacking that space. By the way, that market tends to grow every single year as well; it’s not a zero-sum game. There is plenty of opportunity there, and the grass is not greener elsewhere.

Once you become comfortable in where you’re playing, the question then is: how do you win at that game? I feel passionately that there are four things above all others that differentiate a winner from the also-rans:

- Customer Focus: A complete obsession over customers. If we can’t outcompete the standard marketplace, business will never transfer to the specialty marketplace. We have to offer solutions to our customers that others cannot.

- Market-Leading Expertise: That unique value comes from deep expertise. We need to put together teams of people who are absolutely focused on their specific niche of our industry and are complete experts in it. We create these specialized “Navy SEAL teams” because people in this industry buy deep expertise and rely heavily upon it.

- Speed: Speed is utterly critical. The structural ability to make underwriting decisions at ground level close to the customer at speed will win you business nine times out of ten in this industry. You have to eliminate corporate bureaucracy. The decision-making autonomy which we’ve pushed down into the divisions as a result of the new structure, paired critically with modern technology, is what will drive that speed to market.

- Trust: Finally, this is a trust game. People are buying a piece of paper that promises them we will be good for our claim in the event of the worst happening. Consistently doing the right thing in both claims management and the way that we act with our customers is absolutely tantamount to success. You do those four things well within specialty insurance, and you’ve got a heck of a good chance of building an incredible business.

[00:58:54] Simon Wilson: Strategy is one thing, but how do we structure ourselves? It’s simple in my mind. I talk about building blocks—a ground-up mentality that Tom talked about earlier. We’ve got Markel Insurance at roughly $9 billion, split a third, a third, a third into our three major divisions. Underneath that, you’ve got the 14 P&Ls. Within those 14 business units, the business gets broken down even further by those business unit leaders into highly specialized lines. Every single one of those blocks has people, products, technology, and customers sitting around them.

Those leaders who sit in those blocks—that’s where the magic really happens in this specialty business. There’s a picture of one individual on the screen, a guy named Esteban Manzano, a man we sent out to Madrid back in 2005 to go build a business from scratch. The wonderful thing—my favorite meeting of the whole of 2025—was when Tony Markel and I got on a plane and went around Europe. Tony had never been to our office in Madrid. Tony was able to walk into our office with his name above it—he looked quite pleased about that, Tony—and see 80 Markel associates in a $65 million business operating at a combined ratio sub-90%. Tony had never even been there before. The guy that drove that was Esteban and the team he built around us. If you took any one of the blocks you see in front of you, there’s a story equivalent to Esteban’s within each and every one of them. It is a wonderful story of being able to build a business piece by piece. If we decide to add a new block in here, it works seamlessly within the system and structure we’ve created.

Technology and Artificial Intelligence (AI) Implementation

[01:00:57] Simon Wilson: I am certain that we’re going to have a ton of questions about technology and AI, so I’ll keep my comments very brief at this stage. There are three levels of strategic bets that you need to make on AI and technology in a business of this global breadth:

- Transformational Bets: I believe we can build brand-new businesses completely from scratch within Markel Insurance in the next few weeks that can transform the way we provide services and transact business in certain aspects of the specialty market. We can go ground-up from scratch and create a completely new operational model.

- Reimagining Existing Divisions: We can structurally redesign the business divisions we already have. In areas like Financial Institutions in the US and Transactional Liability over in London, we have completely reimagined how we provide our insurance business through the use of AI, building workflows from the ground up.

- Continuous Quick Wins: Finally, there are hundreds and hundreds of incremental optimization opportunities to improve our business 1% every single day via quick wins.

I’d just like to turn over to a video so the people making these quick wins happen can talk directly to you and give you a flavor of what’s happening with AI in Markel Insurance.

[01:02:16] Video Presentation – AI in Insurance

[01:06:25] Simon Wilson: All right, so there’s a lot going on around AI. That’s just a flavor, and I’m sure we’ll touch on it later during Q&A.

The final pillar that has truly been transformational over the last 12 months centers around culture. What we’re trying to do is take an organization which had become a little bit middle-aged—we had slowed down on grinding out new products—and really instill what we call a “Founders’ Mentality” across the entire organization. There are three elements of a Founders’ Mentality that are critical:

- Insurgency: The clear idea that what we are doing is just going to be fundamentally better than everybody else in the marketplace—a complete passion to deliver something superior for our customers.

- Customer Obsession: The fact that we obsess over and deeply understand our customers, meeting them exactly where they are every single day.

- Owner Mindset: We’ve heard that a couple of times. Every single dollar that we spend on these businesses feels like it’s our own personal money, and we are proud of the businesses that we’re building.

The second part of culture is simply beginning to win again. The idea that we come to work to win, rather than just to do work, is a critical cultural shift across the organization. Bureaucracy is the specific thing, more than anything else, that kills once-brilliant organizations. Our job is to stamp bureaucracy out wherever we find it, and that is a core cultural aspect of how we run this business.

Finally, pure joy and enjoyment. I hear laughter in the air more than I have in a long period of time, and I hear deep ambition in every corridor that we walk down. You put the strategy alongside the structure, the intelligent use of new technology, and people really wanting to be part of this organization, and you put some laughter in and amongst that—I think we find ourselves in a position now where we can really take this organization to the next level and place ourselves back as the preeminent specialty insurer on the planet. Thank you.

With that, back to Tom.

Follow Tilman for more insights

Follow Tilman for more insights

Shareholder Question and Answer Session

[01:08:35] Tom Gayner: Simon, thank you. Thank you all. This is a delightful time when we get to share the progress that we’ve made, and I hope you can feel the sensation of joy that we’re finding in getting things back on the right track. Time for Q&A. We’ve got three spots from which to take questions: Zone 1, Zone 2, and our own Tyler Brown over there with submitted questions. You’re more than welcome to ask any question that you would like; we’d love to hear from you and have a discussion. If you would be so kind as to tell us who you are and perhaps how long you’ve owned Markel shares when you are recognized, and then proceed with your question. With that, Zone 1.

How does management respond to the recent public letter from Jana Partners advocating for the sale of Markel Ventures?

[01:09:20] Shareholder (Jeff Stacy, Toronto): Thank you, Tom. My name is Jeff Stacy. I’m from Toronto, a longtime Markel shareholder. I just want to start by thanking you and your colleagues for putting on such a terrific reunion; it’s just an amazing forum to learn more about our company. So congratulations and well done. My question is about the recent letter from Jana Partners to the Markel board. I read the letter very carefully, and it strikes me that because Jana is so public in stating their views, it’s easy to get the impression that they represent the majority of Markel shareholders. I think the reality of the situation is much different. Speaking for myself as a longtime shareholder, I think it would be a huge mistake to sell the Markel Ventures unit. Personally, I like the permanent business economics and the cash flow diversity that it brings to Markel. I’ve spoken to many other shareholders, and I haven’t found a single one that supports the notion that selling Ventures is a good idea.

The other issue that Jana raised was around share repurchases. It seems to me that there’s more common ground between Markel and Jana on that issue. Markel has been buying back shares, as you showed in your presentation, for a number of years now, and you’ve publicly stated that given the current share price, you would expect that robust pace to continue. I will just say that tender offers can make sense in many situations, but they’re also costly, time-consuming, and they often result in low take-up rates and higher prices being paid than a slow, steady, methodical compounding purchase of shares in the open market. Even on this issue, I find the approach you’re already taking more compelling than what Jana is suggesting. While I accept that Jana has the right to advocate for any course of action they want, as does any Markel shareholder, I think the time has come for them to recognize that they don’t represent most shareholders, and their views are contrary to what most shareholders want. For them to continue advocating with this approach is just a time drain and a distraction for management. My question is simply: would you care to comment on this?

[01:12:41] Tom Gayner: I think I prefer hearing you comment on it, Jeff! No, thank you very much, I appreciate the thoughts. To be fair, when Jana first raised the issues, I happened to have been in New York City at the time. I was in a meeting, and my phone started buzzing quite a bit. I excused myself, looked at my phone, and said a bad word.

I called those folks and noted that they make their actions public without telling us first or giving us a call beforehand because they have their own agendas and things they’re trying to achieve. I mentioned that since I happened to be in New York City, I’d be happy to meet with them and discuss this face-to-face, offering to be at their office by 2:00 PM the next afternoon. I did. I was advised by my advisors and counselors to go in and be “listen only, listen only, listen only.” I went into this meeting, and for the first 45 minutes, I would give myself an A, maybe an A+, on being listen-only. I probably slipped to maybe a B+, or maybe even a B or B-minus as we got into the last 15 minutes or so, because there were some factual things where I just wanted to ask, “Where did you come up with this?” or “Where did you come up with that?” to make sure we agreed upon the baseline facts.

I also noted at the same time that they raised a lot of legitimate issues. We talked about those five-year buckets and how bureaucracy had crept in, as Simon would say, and that we had lost our way a little bit. That was a fair criticism, and I acknowledged that then and say that right now. However, we had already started to take steps to make that better, and we were working hard at it.

I will share a story with you which my wife tells me not to do, so of course, I’m going to do it. In that conversation, I asked if they had executed insurance-related investments before, and they really hadn’t done much in the insurance space. We talked about the unique accounting and time sequences involved. If we sell an insurance policy, we collect that premium on day one, but we accrue and earn that premium over the course of a year, and normally it’s at least two years before you really get a true accounting indication as to how well that particular book of business is performing. The kinds of underwriting restructurings that Simon is doing right now and the operational corrections we’ve implemented take time to clear through the financials. I used the phrase “green shoots” when discussing our recent combined ratio of 93%, but there’s a lot more plural to come behind that “s.” I was just trying to have an accounting conversation, which people love having by the way. I said, “No disrespect here, Simon, but if we had Jesus Christ running our insurance business, it would still be two years before we knew for sure if he knew what he was doing or not yet. So give the guy a break. Give him some time.”

I think the core difference and the core way in which we see the world differently—and it’s not natively right or wrong, it’s just different—is that Markel is a long-term company. We are coming up on a hundred years of history. People invest their entire lives in this company. I have shareholders come up to me and say, “The biggest chunk of my net worth is in Markel stock.” That is a heavy responsibility, and it’s a responsibility I take very seriously. There is an epic amount of trust that has been placed in us by investors and our colleagues; it’s our own life story as well. When you think about things in the permanent time horizons that we do, the pace at which we repurchase shares is subject to a lot of other moving parts—what deals are we seeing, our desire to maintain dry powder to execute on opportunistic acquisitions, and our structural ability to answer the bell for the next round of the fight over and over again, no matter what happens to the macroeconomic environment. Our financial conservatism and methodical pace are reflective of that commitment to make sure that we continue to compound the value of your company forever and right now. But thank you for the question. Zone 2.

What is the outlook for insurance float growth following the exit from the reinsurance business?

[01:17:13] Shareholder (Joey Opin, Richmond): Hi Tom, my name is Joey Opin and I’ve been a shareholder since 2019. I’m based out of Richmond. Thank you again for holding such a wonderful event. Andrew answered my first question during the presentation, so I’ll go with my backup. This question is for Simon and Brian. How should we look at the future of float over the next few years after exiting the reinsurance business? Should we expect it to accelerate as more resources get funneled into specialty, and Markel Insurance doubles down on its bread-and-butter core business? Thank you.

[01:17:50] Tom Gayner: I nominate Costanzo.

[01:17:52] Brian Costanzo: Yeah, thanks for your question. I think you’ll see two different dynamics going on there. First, we put the Global Re business into runoff. When we do that, we stop writing new premiums, so that specific line stops generating new float. However, the reserves sit there for a long time. We’ve got about $3 billion of reserves attached to that business, and those are longer-tail reserves. That float is going to sit on the books for a while and continue to be invested in the securities that we hold.

On the other side of the equation is what Simon talked about—all the organic growth strategies that we have and how we redeploy that capital into our other specialized business units. That’s where you’ll see the secular growth in the float coming in the future. The structural ability to grow in those 14 P&Ls will allow us to continue to accumulate float and compound it, but at significantly better combined ratios and better returns on capital. At the end of the day, the two operational metrics that we’re looking at on a day-in, day-out basis are: what’s our combined ratio (how much are we making on underwriting profits), and how efficient are we with the capital that we’re deploying to generate those underwriting profits? The changes in the financial disclosures we made to highlight Return on Equity (ROE) as a key metric reflect that focus. That’s near and dear to everything that we do and it’s core to how we manage the business every day.

[01:19:14] Simon Wilson: One point I would offer on that is that we obviously stopped underwriting the reinsurance business, and as Brian says, it’s now in runoff. We continue to actively look to draw a permanent line underneath that reinsurance book if the right structural transaction comes across the table. If we can execute a loss portfolio transfer (LPT) reinsurance policy or an adverse development cover (ADC) at the right economics, we will likely take that so we can release the encumbered capital and move on with our growth strategies. That area of capital optimization is something we discuss on a very frequent basis. Thank you, Joey. Mr. Brown.

Has the retirement of Warren Buffett changed management’s thinking regarding the large investment position in Berkshire Hathaway?

[01:20:02] Tyler Brown: All right, I was going to begin with a question about Omaha because, for the first time since 1991, we didn’t have our Omaha brunch, which would have been naturally where a lot of shareholders would have gotten some of your perspective on Berkshire, and we had some questions to that effect. I wanted to give you the opportunity to answer Scott Chapman’s question: has the retirement of Warren Buffett as CEO changed your thinking about the large allocation to Berkshire Hathaway, and do you feel constrained by the large unrealized capital gain in that position?

[01:20:33] Tom Gayner: Well, thank you. I’ll start with the end: being constrained by the large unrealized capital gain position. May the Lord smite me with such a curse! We will worry about those kinds of high-class problems as much as we possibly can and would love to do so. That massive unrealized gain directly contributes to the tax efficiency that we talked about earlier. If you look at the equity portfolio in total, at the end of the first quarter, the unrealized gain was a little north of $8 billion, and it’s probably more than that today. That represents roughly a $2 billion deferred tax liability on our balance sheet. That means there is $2 billion of interest-free capital working on your behalf as shareholders, for which our cost of capital is exactly zero. That is an awesome, asymmetric advantage.

I think that total dollar number of unrealized gains is probably the second highest of any public company in the country. It’s stunning that this little business that grew out of Richmond, Virginia now has the second biggest unrealized gain of any company in the country—obviously with the largest one being Berkshire itself. It’s a high-class problem. If the underlying economics were ever such that I was concerned we should sell it anyway and give up that tax advantage, we would do it, but we would always do it thoughtfully, calculating whether reinvesting “80-cent dollars” into something else is wiser than leaving “100-cent dollars” compounding where they are. Sometimes it is, so we’re very open-minded.

In terms of the brunch out there, we decided we would trade the Omaha brunch for the Richmond barbecue. I didn’t know it was going to be 100 degrees literally for the barbecue, but we did want to shift the focus and emphasis to Richmond because things are changing out there.

To the first question regarding our view on Berkshire Hathaway: I think it remains a wonderful investment. I think it will continue to be a good investment. It is highly diversified, low cost, and very well run. Greg Abel will do a fine job. In the course of time, it reminds me of a parallel: if you think about JPMorgan, it’s a great company that is over 150 years old. If most of us had to take a bet on naming the first chairman ever of JPMorgan, we could probably come up with the winning bet: JP Morgan. I think there are a lot of people who can also name the current chairman and CEO of JPMorgan—Jamie Dimon, a very public figure and well-known business leader. But there were a lot of executives who served in that role between JP Morgan and Jamie Dimon, and I don’t know any of their names off the top of my head. I think a lot of us would struggle to come up with those names. But they were seasoned, professional executives who were highly qualified to do the job, and the underlying institution compounded. I think the case we can expect with Berkshire for a long time to come is that it is a major, substantial, well-diversified business that will be well run by a talented team of professional executives. There will never be another Warren Buffett; he is one of a kind. But the good news is that’s not what Berkshire needs at this point. What Berkshire needs are talented executives to run the operational businesses, and they have them. Zone 1.

If you had a silver bullet to eliminate one competitor, who would it be?

[01:23:47] Shareholder (Raith, Richmond): Zone 1. My name is Raith, I am from Richmond, and I’ve been a Markel shareholder for five years. I have a small question, and I will be happy if all four of you can answer. It’s not an original question—I was reading The Davis Dynasty, and Shelby Davis senior used to visit insurance companies and ask this specific question: “If you had one silver bullet to shoot a competitor, which competitor would you like to shoot?”

[01:24:19] Tom Gayner: I am not going to even allow my colleagues to answer that question! I don’t like to be dictatorial or top-down, but I’m going to say that. We are fiercely competitive and we want to win, and there are times where we see people doing things or saying things about Markel that sort of gets under our skin, and so be it. But positivity is important, optimism is important, goodwill is important, and grace—trying to meet people halfway in a positive way—is essential. We’ve been through a time period of operational adversity and some challenges, but at the end of the day, focusing on shooting competitors is handing over your agenda to somebody else and letting external forces control the way you feel, and that’s a mistake.

I love Matt’s story about the Simply Helping People nonprofit—identifying a tough situation where you can help somebody directly, and then that goes so well that the recipient starts helping back, and a positive daisy-chain reaction is set off. We are not about the business of shooting other people. We have shot ourselves in the foot from time to time, and we are stopping doing that. So we are putting the guns down and running our own business. I told the colleagues they can’t answer, but I see Simon micro-expressions over there.

[01:25:28] Simon Wilson: I’m going to say one thing. Often people think about competitors through the lens of, “Let’s get rid of them.” I don’t think like that. Some of our competitors have done brilliant things to outcompete us which we can learn from. If you just put your head in the sand and say, “I just hate the other guy,” you miss the point completely. Competitor feedback and competitors outcompeting you in an area can be a gift if you’re playing a long-term game. Figure the game out and outcompete them. I think that’s what we’re trying to do now; we’ve shifted our cultural focus. Don’t worry, Tom, I wasn’t going to name anybody.

[01:26:03] Andrew Crowley: I was going to say, if you had asked me that question at 12:15 PM right after Coach Cook was done talking at the forum, when I was ready to run through a wall, I probably would have answered it! I’ve at least had a few hours to calm down now. I feel like I have to say something, even though you can see how well the dynamic of “the colleagues are not going to answer this” is working.

Our friends at Costa Farms have a great phrase around this. They are incredibly kind people, but they are die-hard competitors, and what they talk about is: “We want to promote that competitor to a customer.” At the end of the day, what they really mean is we want to execute so well on quality and cost that they buy our plants instead of trying to grow their own. The notion of competition is that you earn the results you get; you don’t demand them. You don’t sit back and engage in self-victimization. If you’re going to beat the competition, you do it because you earn it. I think the leaders of our businesses think about that every single day: how do they earn the right to win? Iron sharpens iron, absolutely. Zone 2.

Follow Tilman for more insights

Follow Tilman for more insights

How is Markel assessing and underwriting increasing climate-related risks and social inflation?

[01:27:07] Shareholder (Jovanna Ikner, Green Century Capital Management): Hello, my name is Jovanna Ikner. I am from Green Century Capital Management, and we have been investors in Markel for about five years now. My question is for Mr. Wilson in particular. Given the importance of Markel’s insurance business to investor returns and the company’s focus on long-term profitability, how is Markel assessing the potentially increasing exposure of certain lines of its businesses to physical risks, including increasingly severe and more frequent climate-related disasters?

[01:27:40] Simon Wilson: Thanks for the question. I’ll take the property question as you’re touching on there, but I might pivot as well to casualty, because there are structural things happening in the US legal economy that we should be highly mindful of as well.

It is clear that there are certain catastrophic events which occur frequently. What is absolutely clear on windstorms in the southeast of the US is that as and when they do make landfall, the total insured value of the property that has been built in that particular part of the world is exponentially more expensive than it was 10 years ago, and clearly 20 years ago as well. So we have to be mindful that those incidents happen, and we’ve seen Category 5 hurricanes that haven’t made landfall that could have been catastrophic if they did. What we’re doing from an insurance standpoint on property cat (catastrophe) exposure is that we are actually relatively limited in the total aggregate amount of property cat business that we write. We do have some cat-exposed risk—some energy installations in the Gulf of Mexico and some specialized properties up and down the Florida coast—but we are not overly indexed on that particular line of business, and we buy quite substantial reinsurance protection for it as well.

We do believe these physical risks are changing, and I think wildfire is something that is a very significant issue for us as well. All the modeling that we do in our property book and all the reinsurance that we buy are highly thoughtful in terms of establishing what’s the maximum probable loss (PML) that we would be prepared to stomach from an incident like a major windstorm or a wildfire, and we trade strictly within that capital bound.

The area that actually concerns me significantly more than property is the casualty problem. In property, you can model things mathematically and you know exactly where your physical exposure is and how much the replacement value of that exposure will cost you in the event of a storm. What is far harder to gauge is the casualty pricing problem, driven by what people call “social inflation.” The US legal system is absolutely unbelievable at the moment—and I say that as a Brit.

Let me give you a pragmatic example of this. There was a road traffic accident caused by one of our insureds who rear-ended a vehicle in front of him, causing really sad, severe injuries to the person driving the car in front. There was no doubt whatsoever that our driver was responsible for that, and a prompt payment needed to be made from a claims perspective. Historically, looking at our deep data in this area, quite large claims of this nature would typically settle for between $10 million and $20 million, depending on the venue and the specific arguments of the case. We offered $11 million to settle the claim. The plaintiff’s attorney demanded $19 million. We moved to $12 million; they stayed at 19. We offered $13 million; they said 19. We offered $14 million; they said 19. Okay, let’s take this one to trial because we’ve offered and offered and we don’t seem to be making progress. It goes to trial. The jury returns a verdict of $200 million! You’re sitting there saying, “What the heck just happened?”

Depending on the specific geography where these trials are occurring and the jury selection dynamics, you are seeing these absolute “nuclear verdicts” come out of nowhere. Now, that $200 million verdict was subsequently reduced down to around $100 million in a post-trial motion, but you’ve still gone from an actuarial expectation to something that is 5 to 10 times what the data indicated it should be. That is happening increasingly because specialized legal firms and private equity litigation funding see the opportunity to profit from this kind of legal adventurism, throwing a wall of capital at the system to literally take insurance companies to court and sue them. We are doing a heck of a lot within our casualty business right now to structurally reduce our vulnerability to this social inflation problem, shortening our limits and decreasing our line sizes. That is the hardest undercurrent in our underwriting portfolio that we see at the moment. Some of the underwriting issues that I described in those middle years that we are coming back from were directly akin to casualty and third-party liability losses that we were beginning to see manifest. I think we’ve gotten significantly cleverer about how we underwrite around it at the moment, but this pervasive litigation environment across the country isn’t going away anytime soon. Thank you. Tyler.

What characteristics make a private business attractive enough for Markel to give up liquidity and hold it permanently?

[01:32:07] Tyler Brown: Moving to a question from John Marin, which speaks to the competitive position of some of the Markel Ventures businesses. He asked: “Many of the Markel Ventures businesses like Brahman or Costa Farms are businesses most investors would never encounter in public markets. What characteristics make a private business attractive enough for Markel to give up liquidity and hold it indefinitely?”

[01:32:31] Tom Gayner: I’ll take the first stab at this and invite Andrew to jump in as well. We’ve talked for a long time about the four lenses we use to select our equity securities:

- We want a good business that earns good returns on its capital and doesn’t use too much debt to do it (not overleveraged).

- We want management teams with equal measures of talent and integrity.

- We want businesses that have the demonstrated ability to reinvest capital intelligently or execute capital discipline through acquisitions or dividends.

- We want those businesses at a fair price.

That has been the consistent methodology by which we’ve selected publicly traded securities for 30 plus years. It’s the exact same methodology that we use to invest in privately held companies. Actually, in the case of a tie between a public stock and a private company, we would structurally lean towards the privately held company because that ongoing capital reinvestment decision remains under our direct control rather than being delegated to an external board. We like that.

[01:33:36] Andrew Crowley: I mean, we could speak business-by-business, and you would start to wrap your head around what we like about them practically, but looking at the structural concept of what you’re asking about, I’ll point out a couple of things that are embedded in our system. One is the notion of a corporate system that generates lower-correlated cash flows. We all appreciate that in certain macroeconomic crises correlations move towards one, but across normal cycles, having diversified cash streams is a healthy dynamic. When you own a minority share of a public company, you don’t control the cash flows—you can choose to sell the shares, but that triggers a tax event. By having these private businesses wholly owned inside our system, they generate cash on a daily basis that can be dynamically reinvested elsewhere by the holding company. That’s a huge structural advantage.