Berkshire Hathaway Annual Meeting 2026 Transcript

Read the full Berkshire Hathaway Annual Meeting 2026 transcript. Find a full verbatim transcript of Greg Abel’s stage premier at the Berkshire Hathaway Annual Meeting with Vice Chairman Ajit Jain, Katie Farmer (BNSF), and Adam Johnson (NetJets / Consumer).

Follow Tilman for more insights

Follow Tilman for more insights

Easily discover all the topics of the Berkshire Hathaway Annual Meeting 2026 transcript by clicking on the table of contents:

- Opening Remarks & Business Update (Section 1: Berkshire Hathaway Annual Meeting 2026 transcript)

- Executive dialogue & Shareholder Q&A (Section 2: Berkshire Hathaway Annual Meeting 2026 transcript)

- Afternoon session & operational review (Section 3: Berkshire Hathaway Annual Meeting 2026 transcript)

- Closing remarks & tributes (Section 4: Berkshire Hathaway Annual Meeting 2026 transcript)

Opening Remarks & Business Update (Section 1: Berkshire Hathaway Annual Meeting 2026 transcript)

[00:00:00] Greg Abel: Good morning and welcome to Omaha. I want to welcome all our owners—our long-term owners and those that have recently become shareholders. Again, thank you for joining us in Omaha for the meeting. Obviously, we are very excited by this, and I want to also touch on the fact that we have many people here just experiencing it for the first time, so it’s just great to be together.

The first thing I want to touch on is that we had the video highlighting an incredible 60 years. The one thing I did note that we’ve traditionally had was a movie which included the credits that came with it. We’ll have a few other videos that I’ll touch on later, but we did have an exceptional producer and executive producer for this piece, and I want to make sure she is acknowledged: Susie Buffett. Thank you, Susie. And then the director who has always done the movies for us, Brad Underwood. Thank you, Brad.

Now, we have a great day planned, and it’s really all around our owners. It’s our culture, but most importantly, this is our owners’ day, our owners’ weekend. We have an exceptional group of owners, and we’re just passionate to be here. We will communicate a variety of things around Berkshire, our insurance operations, our operating subsidiaries, and Berkshire as a whole. But what we really treasure is the engagement with our owners and shareholders and the questions that come, so thank you. I really appreciate it.

To touch on this morning’s structure, we have three sessions that we’ll cover over the morning and early afternoon. The first session will include some pleasantries here, and then we’ll move directly into a formal business update. As we move into the second session, I’ll have Ajit Jain join us here on stage, and we’ll take any questions in a traditional question-and-answer period, rotating between our shareholders in the arena stations and Becky Quick. Then that session will wrap, and we’ll move to a third session where we will be joined by Katie Farmer, who has been the CEO of BNSF Railway for the past five years, and Adam Johnson, the 10-year CEO of NetJets, who also recently took on an incremental role managing the consumer products, services, and retailing group. They will join us for a traditional Q&A period.

The only thing I would say that is a little incremental or different from past meetings is that throughout this morning we’ll have three different videos associated with our core operating companies. The first one will be from GEICO, narrated by Nancy Pierce, who became the CEO of GEICO in December of 2025. She’s a long-term veteran with a wealth of experience. We’ll also have a video on NetJets narrated by Adam, and a video narrated by Katie on BNSF. The fundamental purpose of both having these managers join us on stage and introducing the videos is that we have an exceptional team at Berkshire. The depth of management is very deep across our numerous subsidiaries, and this provides an opportunity for you as our owners to learn more about those businesses and the leaders that head them.

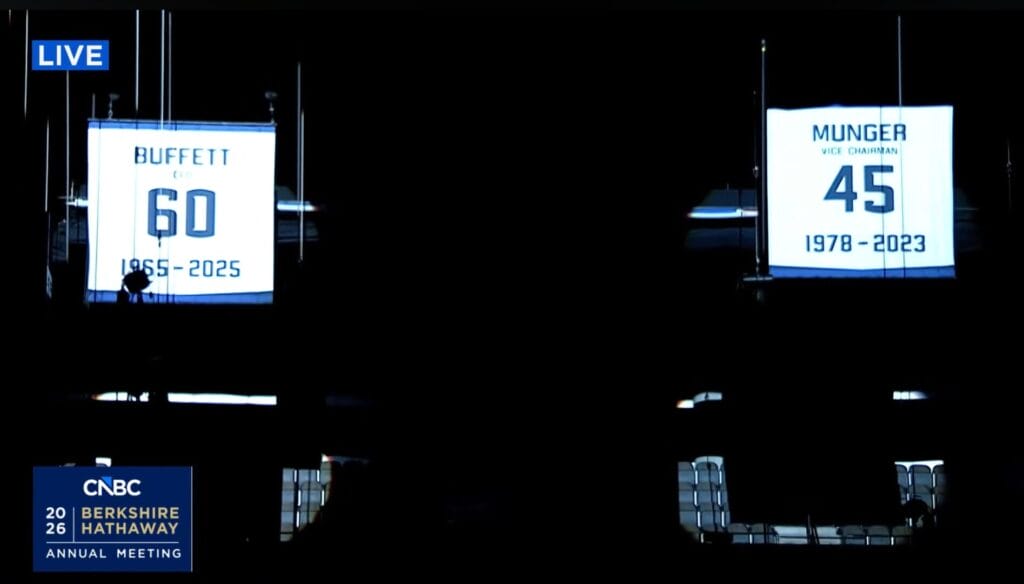

Retiring Warren Buffett’s Number 60 Jersey

[00:05:14] Greg Abel: Let’s move to the formalities now. I’m going to introduce our directors alphabetically so they can acknowledge our shareholders with a wave: Howard Buffett, Susie Buffett, and our Chairman, Warren Buffett…

Warren, we have a little surprise there for you. If you look up to the right in the arena, you’ll see a jersey and a number. We are formally retiring your jersey. Worn appropriately, it is number 60 for your 60 years as our CEO of Berkshire Hathaway. Equally, it is being placed right beside Charlie Munger’s jersey, number 45, representing Charlie’s 45 years with Berkshire as our Vice Chairman and your treasured partner. It’s reflective of a great partnership, and I’m happy to report both those jerseys will remain in the rafters for the years to come. Thank you, Warren.

Warren Buffett’s Address: Apple and Tim Cook

[00:10:29] Warren Buffett: Thank you. Yeah, this is not my show today, but there are two anniversaries that we’re celebrating today. One is the fact that the board has had what I will generously call a refreshment, which they voted, and you couldn’t have made a better decision. They did it unanimously. It surprised all the board when I announced it last year, except for Susie, and that decision has been 100% successful. Greg is doing everything I did and then some, and he’s doing it better in all cases. He’s the right person, so that decision we score 100% on.

But there’s another anniversary today that I’d like to spend just a minute telling you about. About 10 years ago, we made a commitment to essentially move 10% of the total resources of Berkshire Hathaway. We turned it over to another person who was not that well known at the time, and we did that by spending roughly $35 billion buying stock in Apple Corp. We were going to have that under management—essentially turning that money over to the management of Apple to make Berkshire look good, and without any work by us, which is our preferred way of operating.

I would like to report that 10 years later, several things have happened. One is that the $35 billion—counting dividends, realized appreciation, and unrealized appreciation—has turned into $185 billion pre-tax. And I didn’t have to do a damn thing! We are very big around here on having other people do the work and us collecting the money, so that has been a great success. We look at marketable securities as being fractional stakes in businesses; that doesn’t mean we hold all of them forever, but Apple remains our largest holding by far.

Apple is observing an anniversary themselves; within the last week or so, they celebrated their 50th anniversary. Fifty years seems like a long time, but Apple feels like a very new company. When Tim Cook went into the top position at Apple, he succeeded Steve Jobs. Everybody in America knew Steve’s name, but not many people knew Tim’s name at the time. Apple had experienced a roller-coaster ride where the two Steves started in a garage 50 years earlier, Steve was thrown out for a while, came back, did marvelous things developing products, and then had an untimely death. Everybody wondered who was going to manage Apple when Steve wasn’t around, and only a very small percentage of American investors had even heard of Tim Cook when he took over about 14 years ago.

But when we made our investment and turned over 10% of Berkshire’s resources, we were turning it over to Tim. As I say, he has turned that into $185 billion pre-tax. Tim has announced that he is retiring as well from Apple—an announcement made over the last couple of years—and so I think it’s appropriate if Tim Cook would take a bow and our shareholders would say thanks to him. Tim is right down here by me.

How would you like to step into the shoes of Steve Jobs and come through with a record like that? It’s one of the true miracles of American business management. So, anyway, thank you, Tim, and I’m going to turn things back over to Greg.

The Bedrock: Corporate Culture and the Salomon Test

[00:38:52] Greg Abel: Tim, on behalf of our shareholders and owners here, we echo everything Warren said. You’ve truly been a global ambassador around the world for American business, thank you. And Warren, thank you for taking the mic. I am reminded I have a Cherry Coke here in your honor, peanut brittle in Charlie’s honor, and that center seat on stage remains open.

Now, we’ll get into the business update. It really started with the annual letter to our owners and shareholders at the end of February. As we transitioned, I wrote a letter to our 400,000 employees touching on culture and values. The purpose of that letter was to highlight that our bedrock was not going to change. It had never changed under Warren for 60 years. Aspects evolve, but our core culture and values do not change. They are the absolute foundation of Berkshire.

One of the values we often touch on here is integrity. There’s no better example of Warren’s remarkable demonstration of that than when he testified before Congress in 1991 as the Chairman and CEO of Salomon Brothers. I like to call it Berkshire’s Anthem, and I want to make sure we have the opportunity to see that video clip today.

That anthem is embedded in Berkshire. It’s a great reminder for our CEOs and our 400,000 employees. I remind them of this every year, sending a letter in the first quarter asking them, as they run their businesses and make daily decisions, to apply that simple newspaper test that Warren highlighted. Ask themselves whether they are willing to have any contemplated act appear the next day on the front page of their local paper, to be read by their spouses, children, and friends, written by an informed and critical reporter.

Segment review: Insurance Underwriting, Float, and GEICO

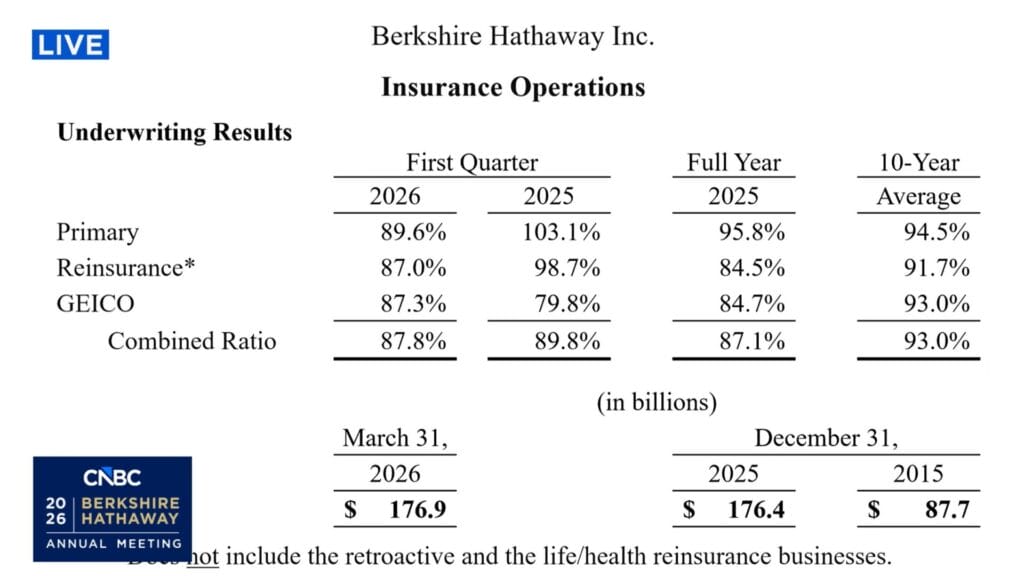

[00:24:43] Greg Abel: Moving to the formal update on our numbers. We issued our 10-Q this morning along with the related press release. I’ll start with our insurance segment. When we discuss insurance, we have two core objectives at Berkshire: we want to underwrite at a profit, and we want to increase our float.

To look at the insurance jargon and numbers, our 10-year average combined ratio is 93%. To give you a little color: if we receive a $100 premium associated with a policy, that 93% represents the total costs incurred—including writing the premium, commissions, and the loss reserves we set up. The remaining 7% (or $7 on every $100) is our pre-tax operating underwriting profit. Within that 93%, roughly $23 represents administrative expenses. The other $70 is effectively what goes down into float. When you see our float growing, we take that capital, hold it, and earn on it over the years until claims show up. For personal or small commercial lines, that $70 gets paid out typically over a 3-to-4-year period. It is a highly valued part of Berkshire that creates immense long-term value for our owners.

If you look at our current first-quarter 2026 underwriting results, primary and reinsurance achieved combined ratios of 87.0% and 89.6% respectively. The amazing thing is there’s an ‘eight’ in those numbers, significantly outperforming our 10-year average. What is driving that? A very benign catastrophe environment. The last time a major hurricane made landfall in the United States was 19 months ago. This benign environment means more capital is flowing into the industry, leading to a softening market. As the market softens, if we cannot realize the proper premium for the risk, Ajit and our underwriting teams will consciously choose to write less premium. We insist on underwriting at a profit.

Moving to GEICO, where we are fortunate to have Nancy Pierce leading that team. They achieved an exceptional combined ratio of 87.3% in the first quarter, yielding over 12% in operating underwriting income off every dollar of premium. Four or five years ago, the GEICO team stepped back because they felt they weren’t getting the proper price relative to underlying risk. Over the last four years, they worked incredibly hard to segment customers and correct that balance. That general premium firming happened across the auto insurance industry, which led to unprecedented customer shopping activity across the auto space.

Nancy and her team are focused on balancing three key metrics. Yes, we have to get the price-to-risk right. But the second piece is retaining our valued customers. The third piece is growing GEICO, measured by policies in force. Comparing Q1 2026 to the same period last year, GEICO’s policies in force grew by 2%. Meanwhile, our number one competitor, Progressive, just announced that they grew their policies in force by 11%. Our team fully acknowledges that it’s not going to be easy to restart the growth engine, but customer retention and structural growth remain clear operational objectives for 2026 and 2027.

Segment Review: BNSF Railway Operational Improvement

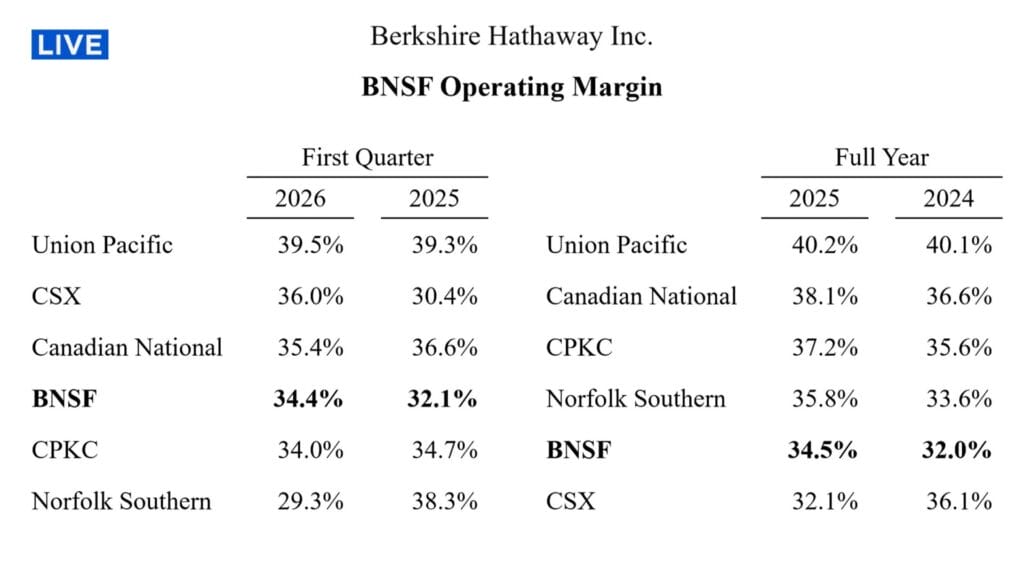

[00:57:46] Greg Abel: Now let’s move to our non-insurance businesses, starting with BNSF Railway. BNSF operates 32,500 miles of track in the West, moving core commodities that touch every industry in the country. While first-quarter results show some nominal improvement, we recognize we have a tremendous amount of work to do. We must improve operationally on the ground—in our yards, moving our cars quicker, and improving efficiency.

We have to recognize exactly where we stand relative to our industry peers. Looking at the six Class 1 railroads operating in the US, last year BNSF ranked fifth out of six in efficiency. The good news is that in 2025, our operating margin improved to 34.5%, a 250 basis point (2.5%) improvement. On a nominal basis, that was the largest margin improvement across all five of our peers. In the first quarter of 2026, I can report we moved from fifth to fourth place, maintaining our efficiency gains. However, our team would be the first to say there’s a lot more to be done. To achieve where Union Pacific sits as the industry leader with a 39.5% operating margin, it will require a fundamental step change in how we approach our railroad operations. A key driver of that step change will be technology.

Technology Transformation and Narrow AI Framework

[01:02:19] Greg Abel: Approximately four years ago, during an operational review at GEICO, I observed a technology transformation taking place. It became obvious that technology was going to be a core part of solving their pricing and customer segmentation challenges. We quickly realized this transformation was highly applicable across all our non-insurance operations.

What does this technology transformation mean? First and foremost, we recognized that Berkshire must become a *builder* of technology rather than just a *buyer* of technology. Historically, our subsidiaries bought disjointed commercial applications or software software packages that remained completely disconnected from our underlying core systems, preventing us from accessing and leveraging our data. We set out to simplify our infrastructure, build proprietary internal solutions, and secure clear, direct access to data. We transitioned senior technology leadership from GEICO over to Berkshire Hathaway Energy and BNSF Railway to drive this. We changed our resource base, aggressively hiring software engineers and developers to build bespoke outcomes.

When I asked our tech team how Artificial Intelligence fits into this, they emphasized that AI is a massive piece that sits directly on top of our simplified systems. However, we are well aware of the broader societal risks associated with unchecked AI. Within Berkshire, we don’t call it general AI; we refer to it strictly as **Narrow Artificial Intelligence**, and we manage it via three rigid governance principles:

- Human Involvement: We maintain strict human-in-the-loop governance. Our senior managers, operators, and employees are directly involved in reviewing and implementing any recommendations generated by the technology architecture. Human judgment is never abdicated.

- The Safeguard Constraint: We enforce a constraint on our data sets. If we ask an AI application for an operational recommendation now, and then ask it the exact same question 30 minutes later, it must deliver the exact same logical outcome. If it does, we know the safeguard is working and the underlying data set is strictly constrained. When the next day’s operational data updates the system, the answer will update marginally, but if we tell the system to ignore today’s data and look only at yesterday, it must return the identical answer.

- Additive Commercial Value: We do not execute AI for the sake of AI. You can spend an immense amount of money in this area. We insist on knowing exactly what operational challenge we are trying to achieve and whether there is a clear, additive value proposition for the business.

We are applying this Narrow AI framework at BNSF to optimize our expansive rail network, which moves over 750 trains a day across 28 states. We view Large Language Models fundamentally as ‘Large Logic Models’—advanced computation engines used to solve complex logical hurdles and drive operational excellence across the entire Berkshire franchise.

Plus COMMUNITY

Discover the Plus Investing community

The Plus community is a great resource for professional investors. Members get support to grow their business and careers, are easily able to connect with other investors and can share ideas and join in-person events.

Berkshire Hathaway Energy (BHE): Data Center Demand & Wild Fire Liability

[01:11:58] Greg Abel: Moving to energy, where technology represents a massive catalyst. A primary, core input for the massive AI data centers and hyperscalers being built across the country is reliable, base-load energy. Berkshire Hathaway Energy has a tremendous opportunity right in front of it to fulfill that demand, but we will do it in a way that is structured properly for our states and our customers.

This isn’t new to us. In Iowa, we serve just under 50% of the state. Because of our historical infrastructure buildout, Iowa has an immense concentration of data centers, with four of the world’s largest hyperscalers building there. Today, data center demand accounts for 8% of our peak utility load in Iowa. While other utilities across the nation are talking about data center opportunities and hoping to reach a 5% to 10% load threshold over the next five years, we are already at 8% and possess visibility to grow that by 50% or more over the next five years. Crucially, we enforce a strict core principle: these hyperscalers must bear their full structural infrastructure costs. We will never transfer that capital burden onto our retail utility customers. Because we’ve managed this properly, MidAmerican’s utility rates remain an exceptional 45% below the national average.

Our pipeline network is experiencing similar structural growth. BHE’s pipeline footprint touches and moves 15% of all natural gas consumed across the entire United States, which provides a massive advantage as natural gas generation is added to stabilize the national grid.

However, the utility sector is not without significant challenges. We are experiencing severe strain on what I call the **regulatory compact**. Under this historical compact, Berkshire deploys billions of our owners’ capital into long-lived utility infrastructure, and in return, the states grant us a balanced, fair return relative to the operational risks we assume. That compact is being severely stressed by inflation and wildfire liabilities in the West. We experienced devastating wildfires in Oregon in 2020. While we fully acknowledge causation and responsibility where our equipment contributed to fires, we faced a massive class-action lawsuit against PacifiCorp, including one specific fire where an independent Oregon Oregon Forestry Department report explicitly stated that PacifiCorp did not cause or contribute to it.

We took a very firm, disciplined position: first, we would not deploy additional Berkshire capital to fund speculative, unmitigated liabilities; and second, we would aggressively challenge that legal liability verdict. In April 2026, the appellate court completely reversed and remanded that liability verdict, resetting the legal proceedings back to ground zero. This is an exceptional outcome that allows us to recover $1 billion in security we had previously posted and completely resets the legal stage. We will continue to work closely with legislatures in Wyoming, Idaho, and Utah to enact sensible wildfire legislation that rebalances the regulatory compact and protects deployed capital.

Follow Tilman for more insights

Follow Tilman for more insights

Industrial Manufacturing (PCC, IMC, WW Steel) and Clayton Homes

[01:21:13] Greg Abel: Moving to our manufacturing, servicing, and retailing group. Our industrial manufacturing segment is anchored by a very powerful metals group comprising three businesses. First, Precision Castparts (PCC), acquired ten years ago in 2016, continues to be run expertly by Mark Donegan. Second, International Metalworking Companies (IMC), an extraordinary global toolmaker acquired in 2006, run by Jacob Harpaz. Today, the aerospace industry is experiencing massive structural demand. Boeing recently reported an 11% increase in quarterly plane deliveries, with a highly similar ramp-up occurring at Airbus. Because the operational efficiency of modern jet engines is so great, commercial airlines find it far more profitable to buy new planes and retire legacy aircraft rather than overhaul old fleets. This has created a massive 10-year industry backlog, driving record demand for PCC and IMC. In fact, PCC has become IMC’s number one global customer, creating excellent internal commercial alignment. Third, our 2022 acquisition of Alleghany brought along WW Steel, a premier structural steel fabricator run by Rick Cooper, famous for engineering the structural steel infrastructure for the Las Vegas Sphere.

In our chemical sector, we have Lubrizol, LSPI (which produces a drag reduction agent that dramatically maximizes pipeline oil throughput), and OxyChem. We closed the OxyChem transaction on January 2nd of this year for $9.5 billion. It is a spectacular addition of invaluable commodity chemical assets that cannot be replicated.

In our building products group, Clayton Homes remains our bellwether. Due to elevated interest rates and consumer budget strains, manufactured housing units sold across the industry were down approximately 10%, and site-built homes dropped 5% to 7% last quarter. However, Clayton is capitalizing on this environment by aggressively driving affordability via our innovative **CrossMod** homes.

A CrossMod home is 70% constructed within our highly efficient manufacturing facilities. The home is then delivered to the lot, where our site builders execute the remaining 30%, adding standard neighborhood roof pitches, garages, and foundation treatments to secure street appeal. We can deliver a beautiful, site-built, two-bedroom family home, completely finished *including the lot*, for $249,000. Furthermore, our traditional single-section manufactured homes can be delivered for just under $35,000. We are actively enabling consumers to achieve the American dream affordably, and I am incredibly proud of Kevin Clayton and his team.

Balance Sheet & Financial Metrics: The $380 Billion Net Cash Pile

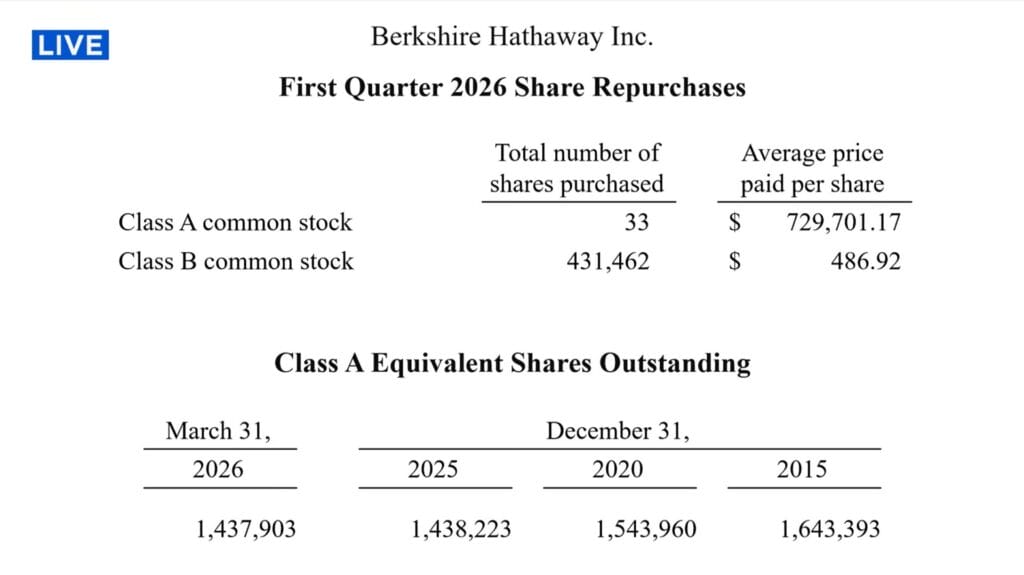

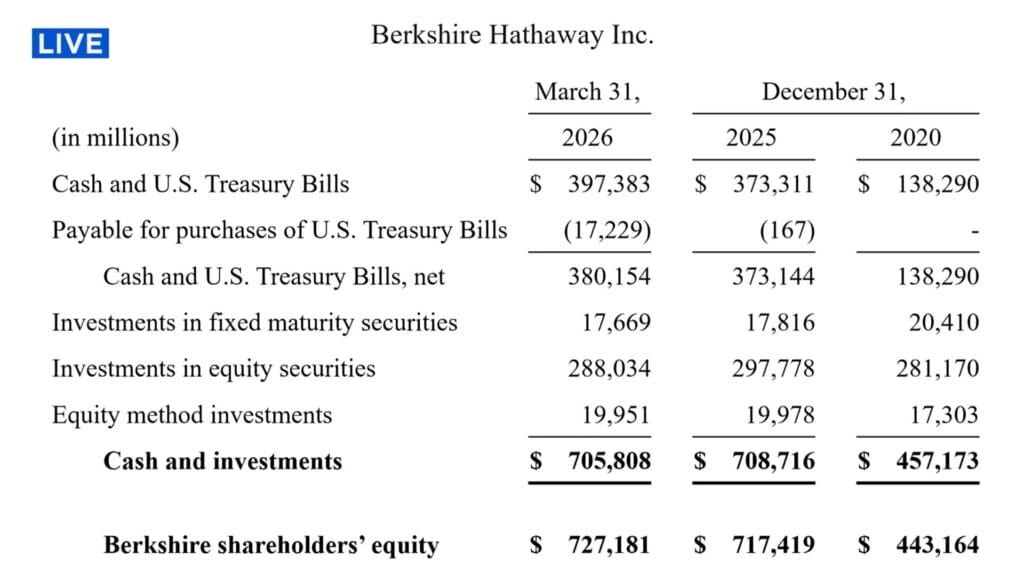

[01:34:50] Greg Abel: Let’s review our balance sheet and capital allocation activity. In the first quarter of 2026, Berkshire repurchased $235 million of its own stock. As we have often stated, we execute share buybacks only when our intrinsic value—conservatively determined—exceeds our current market share price. Warren and I review this dynamic continuously. There are multiple ways to calculate intrinsic value, whether via an adjusted premium over book value or by revaluing our operating subsidiaries from historical cost to current market value. For example, BNSF remains recorded on our books at our original historical purchase price, which sits at a fraction of its true intrinsic value today. We view our intrinsic value through a simple lens: we calculate our net cash, our short-term US Treasury bills, and our equity portfolio marked-to-market, and then add the long-term, 10-year economic prospects of our wholly owned operating subsidiaries, factoring in how effectively we can redeploy the cash flows they generate.

If you look at our gross cash and short-term US Treasury bills, the headline figure sits at $397.4 billion. However, we want to communicate this transparently: that figure includes $17.2 billion in short-term payables for US Treasury bills that we purchased right at the end of March, where the cash settlement occurred immediately in the first week of April. Therefore, adjusting for those settled payables, Berkshire’s **net cash and short-term US Treasury bills position stands at $380.0 billion**, reflecting a net increase of $7 billion during the quarter.

Our total cash and investments sat at $705.8 billion at the end of the quarter, down marginally from $708.7 billion at year-end. To break down the underlying cash flows: Berkshire generated close to $10.5 billion in net operating income and cash flows during the first quarter. We deployed just under $5.0 billion in capital expenditures across our operating companies to reduce operational risk and pursue sustainable growth. Finally, as noted, we deployed $9.5 billion in cash to fully close the OxyChem transaction. It was a highly successful quarter, and our balance sheet remains an impregnable fortress.

Executive dialogue & Shareholder Q&A (Section 2: Berkshire Hathaway Annual Meeting 2026 transcript)

Ajit Jain on the Tokyo Marine deal

[01:25:47] Greg Abel: I want to welcome Ajit Jain to the stage. Ajit, you executed an exceptional strategic transaction with Tokyo Marine in March. I would love for you to expand on the structure of that transaction and the long-term relationship you’ve built with their leadership.

[01:26:16] Ajit Jain: Thank you, Greg. Tokyo Marine is the largest non-life insurance company in Japan. They have been in business for over 100 years and are universally regarded as a premier blue-chip institution in the international arena. They are clearly number one in Japan, with an impeccable reputation. Being in the insurance business for many years, Berkshire has tried year after year to establish a meaningful relationship with them. It was never easy because the primary advantage Berkshire brings to a partnership is our massive capital capacity, and Tokyo Marine was consistently cash-rich and did not require capital partners.

However, given the limited structural growth within Japan, they have spent the last 8 to 10 years expanding overseas, capturing most of the low-hanging international fruit. They remain hungry for non-Japanese international commercial lines. Last year, we had the opportunity to sit down with them and discuss in general terms what our two firms could achieve together. Following that initial conversation, things moved rapidly, and in March we finalized a transaction containing three distinct legs:

- First, we made a simple equity investment, writing a check for $1.8 billion USD to acquire a 2.5% equity stake in Tokyo Marine.

- Second, they possess a highly profitable property-casualty book of business. We structured a quota-share reinsurance agreement where Berkshire takes a direct slice of that business, compensating them for their origination and administrative efforts, securing a highly profitable stream of business for several years down the road.

- Third, we established a long-term strategic agreement. It is not spelled out in exhaustive detail, and normally I am highly concerned about open-ended agreements. But Tokyo Marine is a first-class company. They remind me of that famous phrase J.P. Morgan used decades ago: ‘Doing first-class business in a first-class way.’ That is Tokyo Marine. We have a general commitment to coordinate globally, find international insurance opportunities, and optimize operational structures. I expect this will serve as a powerful springboard to move both companies to the next plateau.

[01:31:04] Greg Abel: Thank you, Ajit. It’s an exceptional transaction and a true long-term relationship. It reminds me of our five other Japanese equity investments; we value the financial stakes, but we see long-term strategic relationships developing across them. I fully support everything you’ve executed.

Warren Buffett deep fake question: Why hold Berkshire long-term?

[01:31:42] Station 1 (Deepfake Video): Hi, my name is Warren from Omaha. I’ve recently undergone a significant change in my role, and I have a not-insignificant portion of my net worth tied up in Berkshire stock. I’ve been telling people I have no intention of selling a single share. My question is simple: I’m 95 years old, I’ve got nothing but time and Cherry Coke, and I want to know, so I can tell my fellow shareholders, why should they hold their Berkshire shares for the long term? Anyway, Greg, take it from here…

[01:32:23] Greg Abel: Well, ‘Warren from Omaha,’ that is a very astute question. As we discussed, our culture and values are the absolute bedrock of Berkshire, which created our incredible asset base. We have our elite insurance business led by Ajit, backed by unparalleled capital capacity. We have our non-insurance subsidiaries where we are aggressively pursuing operational excellence. We have our equity portfolio, and we have our net $380 billion cash and Treasury bills.

That cash pile serves two critical purposes. First, as Warren and Charlie have stated and as I reinforce: *we do not intend to be beholden to anyone.* That is how we manage Berkshire, and that is how we will always manage Berkshire. Second, that asset creates a unique opportunity to deploy significant capital across our operating units or public equities when market dislocations occur. Because we are a decentralized conglomerate, we can move capital seamlessly and tax-efficiently across our entire footprint, moving cash from insurance to railroads or chemicals in a highly tax-advantaged manner.

We are a unique conglomerate because we live by the fact that we completely hate corporate bureaucracy. Arrogance, bureaucracy, and complacency—the ABCs of corporate decay—will kill a company, and we will never allow them to creep into Berkshire. Ajit is our biggest fan on this; he reminds me constantly, and I treasure it. We define success by ensuring that Berkshire endures in its current form, operating consistent with our core business principles to generate long-term value for our shareholders.

*(Note: As the deepfake video concluded on the arena screens, the simulated Warren Buffett picked up a telephone and stated, ‘Excuse me, I need to take this, someone may want to sell me their business. I hope it’s an elephant.’)*

As you all picked up, that was a highly sophisticated deepfake video. It was generated with zero input from Warren—no voice recording, no photoshoot. It utilized entirely publicly available digital information to replicate his exact actions and voice. That is exactly what we are dealing with today when we think about protecting Berkshire. Deepfakes and cyber attacks are a massive, sophisticated risk that our teams manage every single day. We take cyber risk extremely seriously, utilizing advanced technology to constantly monitor and protect our franchise.

Underwriting cyber risk: ‘How bad can bad be?‘

[01:39:13] Greg Abel: Ajit, before we take our first live question, you’ve spoken many times about cyber risk within our insurance operations. Could you share your thoughts on our current underwriting approach to cyber insurance?

[01:39:42] Ajit Jain: We worry about cyber risk at two levels within our insurance operations. First, there is a tremendous, fashionable global demand from businesses seeking protection against cyber incidents. Berkshire has been deliberately, consciously slow to enter this class of business as an underwriter. The primary reason is that I find it exceedingly difficult to discover any meaningful method to accurately assess and model aggregate exposure. Underwriting models claim to have it under control, but there is nothing I can comfortably hang my hat on. When Berkshire assumes any major risk, the very first question we ask ourselves is: ‘How bad can bad be?’ With cyber risk, we cannot answer that question with the degree of certainty we require.

Second, because cyber has been a highly popular product over the last several years and there haven’t been catastrophic, systemic cyber insurance losses yet, underwriters have generated short-term profits. As a result, an influx of industry capital has driven cyber insurance premiums down. We absolutely hate entering any line of business where pricing is actively soft and coming down. So, we are comfortable sitting on the sidelines. The day will undoubtedly arrive when prices harden, and Berkshire will have a fairly significant role to play in cyber insurance. Separately, as a large corporation, we face internal cyber perils; we consistently exceed all regulatory compliance standards to protect our internal systems, though one can never be completely categorical about cyber security.

Follow Tilman for more insights

Follow Tilman for more insights

Human judgment vs. AI tools in underwriting

[01:42:20] Becky Quick: This question follows up on AI, coming from Billy De Ross in Ardsley, New York: ‘In an era of increasingly complex risk models and AI tools, where does human judgment still provide Berkshire a competitive advantage?’

[01:42:54] Ajit Jain: AI is exceptionally fashionable right now, with companies jumping into the space across both insurance and non-insurance operations. If AI becomes the complete reality that is currently being projected, it will undoubtedly be a massive structural game-changer. However, what we are currently observing is AI functioning primarily as a productivity tool—an effective mechanism for reducing routine administrative labor costs and executing repetitive tasks. I remain highly skeptical that AI will reach a point anytime soon where it can replace human judgment or make complex trade-offs in pricing risk or settling complicated insurance claims. That reality is still years away. If you are counting on AI to tell you which stock to buy or sell, I do not believe that is going to happen.

[01:44:02] Greg Abel: Ajit and I were discussing this exact dynamic with his underwriting team a few weeks ago. His team immediately pointed out that while they monitor cyber risk, they are actively utilizing technology to maximize efficiency in writing and managing internal code. From an underwriting standpoint, technology allows us to scale our capabilities. Historically, our traditional underwriters might have had the capacity to deeply analyze the five largest risks in a portfolio; today, utilizing advanced computation tools, we can secure a rapid, comprehensive view across 15 additional risks, allowing our human underwriters to exercise human judgment on a much wider set of opportunities.

Distinguishing patience from action

[01:44:53] Station 1 (Livia from Irvine, CA): It is my honor to see both Mr. Buffett and Mr. Abel today. My question is: as a young investor navigating uncertainty and rapid technology change, I often struggle to balance patience with action. How would you personally distinguish between the two?

[01:46:22] Greg Abel: I believe one of Berkshire’s greatest structural strengths is our extreme patience and our absolute discipline when allocating capital. Opportunities will always surface over time. Having patience doesn’t mean opportunities don’t exist today, but it means you must resist the urge to deploy all your capital or spend your money rapidly. Cash is an asset that provides an exceptional opportunity when a true value proposition emerges.

We evaluate opportunities through strict principles: we must thoroughly understand the business, its structural opportunities, and its risks. We insist on a clear, understandable view of what its economic prospects look like over a long-term, 10-year horizon—not just the next quarter or the next year. We approach our investments with the mindset that we will own them forever. Finally, we must have complete confidence in the capability and integrity of the management team. If an opportunity fulfills those benchmarks, but the current market price does not offer a margin of safety, we say no. We are never anxious to deploy capital into subpar opportunities. But when our principles are met, we will act decisively, quickly, and with significant capital.

[02:01:06] Ajit Jain: Insurance, much like investing, is a game that strictly requires patience, and it is exceedingly difficult to get professionals to sit back and do completely nothing. When I recruit underwriters, my explicit modus operandi is to tell them right up front: ‘Your core job description is to say no.’ You will be bombarded with broker deals day in and day out, but your structural base case must be to say no. Every now and then, you will encounter a deal that hits you like a 2×4—it will be screaming money. That is when you bring it to me, and we make an immediate decision to execute.

All kidding aside, it is highly difficult to sit there and do nothing while everyone else in the industry is buying, selling, and being wined and dined by brokers in London. But the true test of being successful in insurance, and fundamentally in investing, is the absolute ability to say no.

[02:02:20] Greg Abel: That is beautifully said, Ajit. It applies perfectly across all our operations. It reminds me of an acquisition we executed where we faced a challenging legal deposition. The opposing counsel asked, ‘How would you describe Greg Abel as a manager and a CEO?’ and our operator responded, ‘Well, all he ever says is no.’ I take that as a major compliment. Part of elite management and disciplined investing is the willingness to say no, despite the intense external urgency to act.

Afternoon session & operational review (Section 3: Berkshire Hathaway Annual Meeting 2026 transcript)

Katie Farmer on BNSF efficiency turnaround

[00:00:15] Greg Abel: Welcome back to the afternoon session. Katie, during our morning segment, I highlighted to our owners that BNSF’s operating margin historically lagged our peers, ranking fifth out of six railroads last year. We’ve moved to fourth place in Q1 2026, but closing that performance gap completely requires a step change. With 35,000 employees spread across our rail network, how are you leading the organization to execute that operational turnaround?

[00:01:24] Katie Farmer: Thank you, Greg, and thank you for the opportunity to speak with our owners today. We absolutely recognize that it is critically important for BNSF to run a highly efficient operation, secure a competitive cost structure, and aggressively close the profitability gap between us and our competitors. We have an exceptional leadership team in place that understands the absolute importance of aligning all 35,000 men and women of BNSF around the strict execution of operational excellence. We generated solid progress in 2025, and that momentum continued through the first quarter of 2026, but we know we have substantially more work to do.

To break down how we are driving this: it centers on operationalizing and institutionalizing specific efficiency gains. First, we focused heavily on improving our single-car carload network. BNSF runs multiple rail networks: we have our intermodal network, our unit-train bulk networks moving agricultural products and coal, and our carload network, which handles non-unit single cars. That carload network is highly asset-intensive, requiring immense operational focus and consuming vast amounts of resources. Anything we execute to maximize the velocity of that single-car network frees up capacity, optimizes resources, and allows us to handle identical or greater freight volumes using fewer total assets, which translates directly into expanded profitability.

A practical example of this structural improvement occurred in the first quarter of 2026: BNSF handled a higher total volume of freight cars compared to the first quarter of last year, but we executed that increased volume using **260 fewer total locomotives**. That achievement delivers a highly consistent, reliable service product for our customers while drastically lowering our operating costs. We are spending an immense amount of time ensuring that operational discipline is embedded across our network.

The second critical lever is our technological transformation. We are collaborating directly with our new BNSF Tech organization to achieve the next step change in efficiency. We are successfully reducing the time freight units dwell inside our terminals and maximizing overall train velocity. We are actively attracting elite data scientists and operations research experts, placing them directly alongside our rail operators in our Network Operations Center. We are building and leveraging **digital twins**—highly sophisticated computational models that allow us to simulate our entire railroad operations before we dispatch trains onto the physical tracks. We are deploying predictive ETA algorithms for our customers, which allows them to optimize their supply chains and enables BNSF to turn its rolling stock far faster. Finally, we are aggressively attacking our largest structural cost buckets, achieving a historical first-quarter record in fuel efficiency. This fuel efficiency reduces our cost, shrinks our environmental footprint, and maximizes our competitiveness against over-the-road trucks.

BNSF and autonomous trucking: Regulatory bottlenecks

[00:16:52] Station 5: Katie, as Greg highlighted, BNSF’s profitability lags its competitors. With eventual technology advancements in autonomous driving, over-the-road trucking costs will continue to drop. How will BNSF maintain its competitive advantage against autonomous trucks and new technology?

[00:24:57] Katie Farmer: BNSF possesses the largest domestic intermodal franchise of any railroad in the world. Backed by our unique, decades-long relationship with J.B. Hunt, we have been highly successful at converting over-the-road truck freight onto our rail network, executing more freight conversions than anyone in the industry, so we know exactly how to compete with trucks. Regarding autonomous technology, it represents a significant opportunity for us as well. Railroads operate on a completely closed-circuit, proprietary network, which provides an inherent structural advantage when deploying autonomous systems.

We previously invested billions to implement Positive Train Control (PTC)—a highly sophisticated safety overlay that monitors and controls train movements digitally. Historically, operating a train required a five-person crew; over time, technology allowed us to reduce that safely to two people on the vast majority of our trains. As autonomous trucking technology continues to evolve—such as the recent autonomous truck pilots operating along the I-45 corridor in Texas—railroads must be permitted to innovate at an identical pace. To maintain our structural competitive advantage, we require a modernized regulatory framework that supports railroad innovation and allows us to safely leverage automation to optimize crew sizes. We are focused on driving that operational discipline, capitalizing on technology, and securing the regulatory flexibility required to out-compete over-the-road trucking.

Adam Johnson on reversing subsidiary underperformance

[00:26:49] Greg Abel: Adam, you took over NetJets as CEO a decade ago when the business was underperforming, facing billions of dollars in internal debt, and Warren had explicitly stated in his annual letter that NetJets was his toughest mistake, warning that it would have faced bankruptcy without Berkshire’s backing. When you think about managing subsidiary underperformance, how did you completely restructure that business and return it to market leadership?

[00:28:25] Adam Johnson: To give our owners some context: NetJets is an incredibly complex, ad-hoc, unscheduled aviation business. While commercial airlines fly to perhaps 50 or 100 heavily structured airports, NetJets operates flights across thousands of global airports in 150 different countries. I returned to NetJets as CEO on June 1st, 2015. On that Monday afternoon, I gathered our core management team into a room and asked a simple question: ‘How many people in this organization truly understand the operational and financial bookends of our business?’ The answer I received was deeply concerning—far too few people possessed a comprehensive view. It became obvious that to reverse underperformance and rebuild our culture, we had to eliminate internal information silos. We established a strict rule: if I understand exactly what you are executing in your department, and you understand exactly what I am executing in mine, we will achieve great things together.

During my preparation for my very first formal Berkshire board meeting, I was incredibly excited. I had put together a extensive presentation focused heavily on aggressive growth metrics and commercial expansion. Greg Abel pulled me aside in a highly constructive, teaching manner and said, *’Adam, why don’t you pay $1 back to Warren first, and focus entirely on getting your debt down?’* That was a profound, defining management lesson for me, and I took it completely to heart. We immediately shifted our focus, put our blinders on, and aligned the entire company around two unyielding metrics: uncompromising safety and exceptional service.

Warren bought NetJets in 1998 after being a customer since 1995, and he recorded a core operational video for our employees that we still utilize today, emphasizing that he demands safety and he demands service. By keeping our organization strictly within that alleyway, executing with intense discipline, we completely paid back our billions in debt, returned substantial cash flows back to Berkshire Hathaway, and secured our position as the undisputed global leader in private aviation. Only within Berkshire can you feel like the new kid on the block after 30 years with the company, and the unconditional support we receive from leadership when delivering news—good or bad—is completely unmatched in corporate America.

Since taking on the presidency of the consumer products, services, and retailing group in December, I’ve utilized our aircraft to visit our other 31 subsidiaries. I was initially concerned because many of these excellent CEOs had reported directly to Warren for decades. But my concerns were quickly allayed. These leaders possess immense intelligence, energy, and integrity. They don’t know the names of every shareholder in this room, but they know exactly what you expect. Today marks the 30th anniversary of Warren writing Berkshire’s Owner’s Manual, which serves as our absolute business bible. Our CEOs understand and live that manual. Across those 32 consumer companies, the average age since founding is an extraordinary 88 years. Only 0.5% of American businesses survive past 80 years. Five of our companies were founded in the 1800s. When I called those CEOs to discuss the bouncing ball of recent import tariffs, they told me, ‘Adam, we’ve been dealing with tariffs for over a hundred years.’ Our businesses possess an incredible ownership and stewardship culture, and we are completely committed to executing for Greg and his team.

Follow Tilman for more insights

Follow Tilman for more insights

The conglomerate model and exit earameters

[00:40:21] Becky Quick: This question comes from a shareholder who wishes to remain anonymous: ‘Is there any future circumstance that you could envision Berkshire divesting businesses or being broken up? If so, what are those circumstances?’

[00:40:55] Greg Abel: That is an excellent, frequently discussed question. We have always highlighted that specific, narrow circumstances exist where Berkshire may no longer be the optimal permanent owner of a business. First, if a subsidiary faces deep, systemic labor issues that we cannot resolve over a prolonged period. Second, as I articulated in my annual letter, if an operation creates severe reputational risks that we are completely unwilling to let Berkshire or our owners experience. If a business’s culture or evolution compromises our core integrity, it does not belong in the Berkshire family; it may function as a fine business for someone else, but we will not own it.

Third, if an operating unit becomes structurally unsustainable and is no longer capable of generating operating cash flow for our shareholders, we must execute serious decisions. If another operator can run it more successfully for the customers and employees, we will evaluate a sale; otherwise, if it faces continuous, unmitigated losses, we would wind it down responsibly over time while seeking the optimal path for the employees and customers. We take our obligation to properly deploy capital extremely seriously.

A perfect, real-time example of this is our recent announcement that we are selling a portion of PacifiCorp—specifically our utility operations in the state of Washington. PacifiCorp is a complex utility operating across six different Western states. Washington State implemented highly aggressive, localized clean energy policies that began having a severe, adverse impact on the underlying utility costs of our consumers across the other five states. We worked incredibly hard to establish a balanced multi-state compact, but it was not materializing, and our other states were being forced to bear structural costs that weren’t theirs. We consciously decided that this model was broken for our owners and our customers. We exited the Washington asset, finding an excellent purchaser who fully supported and could execute that state’s localized policies. This transaction reflects an evolution; when we acquire a utility, we tell regulators our commitment is forever, but it must reflect a balanced relationship that works. If it is broken, we will find a superior path for Berkshire.

To address the second part of the question regarding breaking up Berkshire Hathaway or spinning off asset blocks: **absolutely not**. We are a conglomerate, but we operate as an exceptionally streamlined, hyper-efficient conglomerate. We do not maintain centralized corporate management layers, we do not have bloated human resource groups, and we do not have corporate committees directing our businesses on how to manage their customer relationships or operational decisions. When Adam assumed his expanded presidency over 32 companies, I explicitly informed him that he would receive zero corporate staff support in Omaha or within his team; his operators step up and assume that responsibility directly. Most traditional corporate conglomerates end up bogged down under massive, bloated corporate overhead costs that completely fail to add value to the underlying operations.

Our conglomerate structure works beautifully because it is entirely free of corporate bureaucracy. It provides a massive, unmatched structural advantage: it allows Berkshire to move immense capital across completely different operating groups in a highly tax-efficient manner. Other companies cannot execute this. BNSF is a perfect example; it generates substantial annual operating cash flows and distributes large dividends up to the parent company. We can review those funds and decide whether that capital is best deployed funding capex in another operating subsidiary, purchasing public equities, or, if no juicy opportunities exist, parking it safely in short-term US Treasuries. Our conglomerate structure operates with immense effectiveness, and we have zero intention of ever divesting asset blocks or breaking up Berkshire Hathaway.

Closing remarks & tributes (Section 4: Berkshire Hathaway Annual Meeting 2026 transcript)

[01:00:04] Greg Abel: We have reached the conclusion of our meeting. I want to extend my deepest thanks to all our long-term owners, our new shareholders, and everyone who traveled to Omaha for this experience. We deeply enjoy this annual engagement. Pulling this massive event and exhibit hall together requires an extraordinary effort, and I want to formally thank our coordinator, Melissa Shapiro. Thank you, Melissa.

Finally, I want to pay tribute to our long-standing CFO, Mark Hamburg, who announced that he is retiring in June after an unbelievable career. Mark has served as Berkshire’s Chief Financial Officer for 34 years, and when his advisory year concludes, he will have completed 40 years of service with Berkshire Hathaway. Mark wears an immense number of hats in this company—he acts as our corporate secretary, oversees annual meeting logistics alongside Melissa, and holds an invaluable repository of Berkshire knowledge. To replace Mark, we had to hire both a new CFO and a General Counsel—it literally took two professionals to replace him! Mark, thank you for your incredible, permanent contributions to Berkshire. Warren has highlighted your excellence, and I can only echo his praise. Thank you so much.

Thank you again to our owners for this remarkable weekend. We remain passionately committed to protecting Berkshire’s culture, executing with absolute risk discipline, and building long-term value for our shareholders. Thank you, and we look forward to seeing you all back here in Omaha next May.