Bolloré: Music Streaming & African Growth at the same time?

Music streaming is a very popular investing topic for some time now, but if investors in streaming companies (i.e. Spotify) are best placed to participate in the music streaming value creation is not yet clear. Investing in the African growth story is older and was hyped time and again. The discussed company might be a good opportunity to participate in both trends with limited downside risk via a French company – Bolloré SA…

This is not investment advice. The authors does currently own shares (economic interest) in mentioned companies. Please see our disclaimer.

First time I read about Bolloré SA (Bollore) was in an article from Vitaliy Katsenelson, who is one of my favorite value investing writers. Since I (as a shareholder) knew about Tencents mentioned acquisition of a stake in UMG and I share the long-term view that streaming services will only get more important in our lives I read Vitaliys article carefully and decided to take a deeper look…

Before publishing this post, I discovered other bullish opinions on Bollore. Most of these articles tell a similar story to Vitaliys post, but some are much more number focused. They claim that the number of shares outstanding is effectively much lower than usually indicated by commonly used financial data providers like Bloomberg etc.

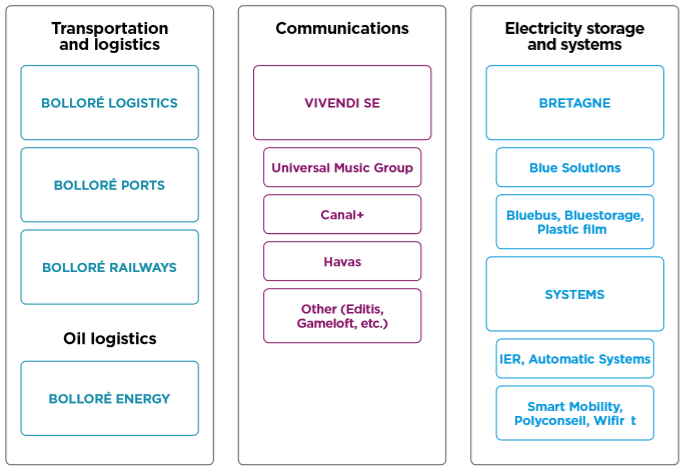

Bolloré SA is an € 8 bn market cap French conglomerate listed on Euronext Paris under the ticker BOL FP. Its activities are organized in the following three segments Transportation and Logistics, Communications and Electricity Storage and Systems.

Bollore is publicly traded but compley. It is majority controlled by the Bolloré family, via Financière de l’Odet SA, itself listed on Euronext Paris with a current market capitalization of €4.5 bn (ticker: ODET). The controlling family could in fact provide a rare long-term perspective, creating above average shareholder returns. With a Bolloré as CEO at the company, I believe the owner perspective can surely be assumed (Bollore 2019, p11).

A dividend yield of 2% is indicated for Bollore, currently. The P/E seems pretty high with 37x (fwd P/E 19x), but probably understates the true value (and structure) of the company. Read why …

Bolloré: Company Operations

Understanding Bollore is not easy. To begin with Bollores operational segments might make sense! Additional challenges are the asset structure as well as the reporting structure. Bollore uses different ways to present the various business activities (brands vs financial reporting structure) creating additional confusion for (potential) investors. It surely does for me. If you do not give up on the way, we will take a look at the shareholder structure and a complicated web of corporate structures. But let’s start with Bollores operations …

Transportation and Logistics

The Transportation and Logistics segment (TaL) operates four business lines (brands) in synergy, with a strong focus on Africa. Bollore claims to be ‘Africa’s largest transportation group’ after investing € 4 bn in 40 years. This network could indeed enable the group to offer better services and earn above average margins from customers. (1) Bollore ports operates 21 ports globally, 17 of them on the African continent. (2) Bollore logistics is a leading international provider for supply chain solutions with a strong presence in Africa. (3) Bollore Railway is a railway construction and operation specialist in Africa. (4) Bollore Energy provides transportation, distribution and storage services for oil products in France and Europe. The African operations should provide possibilites to invest high amounts of capital and build a strong network, enabling the company to earn high profits. It is quite unlikely that someone will build a second railway/port next to an existing one from Bollore. Additionally it is not unlikely, that commerce in Africa will grow in the decades to come (true that is said for a long time!).

M&A activities support the below medium term goal (anorganic growth strategy). In 2018 (p20), Bollore acquired a majority stake in Global Solutions A/S, a Danish transportation and logistics operator, strengthening its global network.

The Group’s medium-term goal is to become one of the top five logistics companies worldwide.

Business report 2018, p12

The internal financial reporting continues to be based on the groups geographical organization.

The transportation and logistics industry faces several risks, potentially leading to lower volumens and rates in the short to medium term: global pandemic, trade war. Deglobalisation and nationalization trends are potential longer-term risk factors but until now I do not believe that to be too likely (politicians talk…).

Doing business in Africa is always a double-edged sword, it seems to me for a long time. It is a widely held opinion that there are potentially vast growth opportunities doing business on the continent (you can read three weekly dispatches on a great blog here for free). But the opportunity comes not without its risks on the continent (war, unstable politics, etc.). To get exposure to Africa via a French company might not be the worst idea. Reuters reports about allegations that Bollore corrupted officials to win port concessions in West Africa. Taking all this into account, the business activities in Africa probably deserve a risk discount on the one hand, but a higher valuation accounting for the fact that African economiese are expected to grow stronger than the world economy on the other hand.

The financials of the TaL segemnt seem rather attractive to me.

Electricity Storage and Solutions

The Electricity Storage and Solutions segment or ESS is active in a whole range of activities built on its historical research of films for capacitors. This research was used to develop its Lithium Metal Polymer or LMP (solid state) battery technology and other activities around it. The ESS segment is split in two sub-segments (divisions) Brittany and Blue Systems.

Brittany is the first division within the ESS segment. The Brittany devision includes the following activities. Bluebus produces all-electrical buses in France. So far, 400 buses are in operation globally, but political action could drive demand much higher in Europe, I guess. Bluestorage sells energy storage solutions (read huge batteries), so far mostly in France and South-West Africa. The regional focus makes sense to me. They probably leverage connections in Africa to meet demand for (rural) off-grid solutions. So far, only 30 installations are deployed globally, but further growth in Europe and Africa is not too unlikely I guess. Plastic Films produces films for capacitors and other electrical components. Additionally, the activities of Blue Solutions are subsumed under the Brittany division.

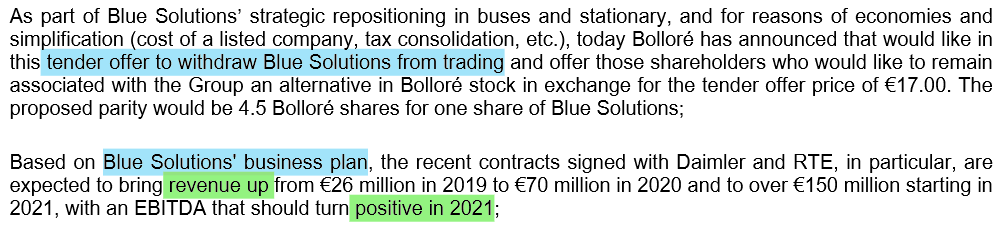

Blue Solutions is a part of Brittany and is was listed since 2013 under the ticker BLUE FP … and will most likely be delisted in June 2020. Bollore will pay a price of € 17 per share (shareholders can choose to receive ~4.5 Bollore shares instead of cash), indicating a market capitalization of € 495 m for the company (see presentation). Blue Solutions forms the foundation within the Brittany devision. It developed the battery technology that they claim ‘has many advantages in terms of safety, energy density and performance without being sensitive to external temperature conditions‘. The investments in R&D have yet to pay off, but, the timing for the delisting might be a hint to a more profitable future (if you want to interpret it that way). I believe the delisting makes strategically sense. (you might want to listen to Damodarans opinion on strategic acquisitions)

Blue Systems is the second sub-segment. It ‘offers an ecosytem for optimising the flow of people equipment and data‘. Blue Systems‘ designs and manufactures pedestrian, vehicle and passenger access systems (Automatic Systems), it manufactures electric cars (Bluecar), made available through (Bluecarsharing) in France, Italy, London, Singapore, and it provides for-hire electric shuttle bus services (Blue Station).

Blue Systems includes even more activities. EASIER provides a ‘comprehensive range of products for airports, airlines & public transportation projects‘. These are used on private property roads, train stations and airports for example.

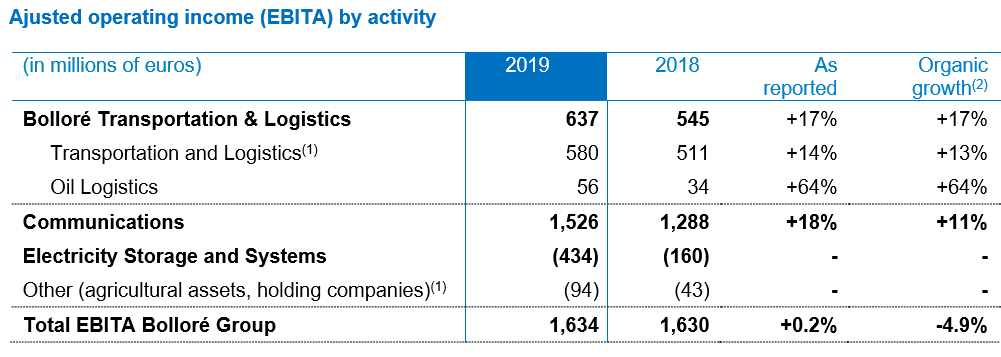

ESS segment is unprofitable. The overall financial ESS segment results are still negative. In 2019 ESS contributed an adjusted operating income (EBITA) of € -434m (after -160m in 2018) driven by impairment losses of € -319m, to a group EBITA of € 1,634m (1,630m). This negative results imply that true asset prices (likely some positive value) of ESS might not be reflected in Bollores market value, currently. ESS’ operating results are negative for a long time.

Blue Solutions could turn positive in 2021 based on its Ebitda metric. This strongly supports my believe that Blue Solutions has a positive asset value. The market capitalization is about € 500m based on the takeover offer of € 17 per share. It traded for ~300m before the takeover offer, based on a price per share of € 10. Sales are still low, but 1,700 registered patents indicate a (high) positive asset value. R&D expenses in 2018 were € 50m, according to Business report 2018, p36.

Bolloré´s communications arm

The trophy assset is Universal Music Group. UMG is 90% owned by Vivendi (controlled by Bolloré SA) after a consortium around Tencent Holdings Ltd. bought a 10% stake for $ 3.4 bn with the option to buy a further 10% stake for the same amount until Jan 15, 2021. According to Bloomberg, Tencent could help targeting the Asian market. Warner Music (WMG US) was priced similar to the transaction for its IPO in June, based on an EV/Ebitda multiple of c. 24x (as of June 19, this has expanded to a forward multiple of ~26.4x).

With current treaming trends in our minds, it is quite easy to imagine strong revenue growth for UMG for years to come with expanding profit margins. Late 2019, Vivendi reported high double digit growth of +23% for UMGs subscriptions and streaming revenue.

Vivendi again is fully consolidated into Bollores financials since April 2017. According the 2019 urd (p147), Bollore owns 27.06% of Vivendi SEs equity as of Dec, 2019. This stake translates to a market value of € 6.5 bn. Vivendi plans to monetize further minority stakes in UMG, representing a clear catalyst for Vivendis market valuation. Vivendi is buying back considerable amounts of shares.

Because of French rules that grant double voting rights to established shareholders, Bollore effectively controls Vivendi.

Vivendis other business units besides UMG are active in television and cinema in France and international markets (Canal+), consumer/brand relationships (Havas), mobile games (Gameloft), live entertainment (Vivendi Village), hosting and broadcasting of video content (Dailymotion) and French publishing (Editis). Some perform better than other, but Vivendis value is clearly in UMG. So I do not bother to think about the other businesses too much.

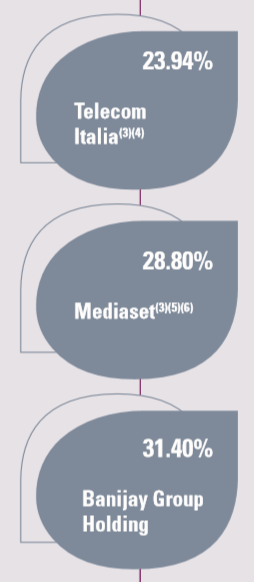

The Vivendi portfolio consists primarily of shareholdings in Telecom Italia (23.94%) and Mediaset (28.80%), currently worth several € bn and held by/through Vivendi.

Vivendi SA might well be undervalued currently on its own. Its market capitalization (as of June 9, 2020) of € 26.8 bn and financial net debt of 4 bn, as of Vivendis consolidated financial statements 2019, p19 result in a € 30 bn EV. If UMG (based on the Tencent transaction) is worth 30 bn alone (equivalent to m cap + net debt), we get Vivendis other business units ‘for free’. Most notably its portfolio of listed non-controlling equity interests (incl. Telecom Italia), Canal+ and Havas. In fact, only € 704 mn (or 62%) of 1,132 mn of positive segmentational CFFO is generated from UMG. I conclude that it is easy to argue for an undervaluation of Vivendi.

Media and telecoms businesses within the Communications and Media segment include CNews a free daily newspaper, Bolloré Telecom owns and operates 3.5 GHz frequency licenses in France and Wifirst (sold in 2019) offered WiFi as a service.

Bolloré Portfolio

The Bolloré portfolio is composed of direct shareholdings in Mediobanca, Socfin, Vallourec and Bigben Interactive, according to the business report 2018, p 44. Bollore indirectly holds shares in Telecom Italia and Mediaset via its Vivendi shareholding portfolio.

Standalone Financial Position

Bollores standalone financial position is reported for 2019 on pages 270f, in my understanding. Based on this numbers I will build my SOTP valuation.

I calculate a standalone net debt of € ~1 bn for Bollore SA. This results from ‘Total Debts’ of € 5.9 bn minus 4.8 bn of ‘Other Receivables’ and 130m of Cash. According to Note 4 (p280), the majority is from current accounts due within one year.

Valuation

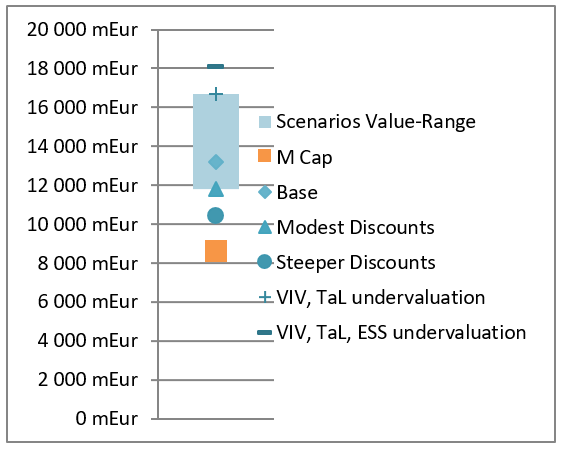

My base case scenario makes use of current market valuations as of June 16, for Vivendi, Medio Banca, Socfin, Vallourec and Bigben as well as Bolloré SA. The transportation and logistics or TaL segment is valued at an assumed multiple of 12x estimated Nopat of € 445.2 m (2019 Ebita of 636m and an est. tax rate of 30%) resulting in a value of € 5,342 m. For ESS, I assume a value of € 1 bn (and I could be totally wrong here). I calculate a NAV of € 13,175 m vs an unadjusted current market cap of 8,591m for Bollore, indicating a discount of 34.8%.

Other scenarios take into account a potential undervaluation of Vivendi (1.3x), lower values for the Bollore portfolio, lower or higher multiples for TaL (8x to 17x), and values for ESS from 300m to 1,500m as illustrated below.

The obvious catalyst for a higher pricing of Vivendi SA is a listing of UMG (like Warner Music). Monetization of other assets could also be beneficial. Any material repricing of Vivendi should directly benefit Bollores pricing. Reaching either profitability for the ESS segment or selling it should result in an uplift of operating profit and could result in higher valuations as well. Cash can be deployed in Bollores Africa business.

Web of Crossholdings

Red flags or tremendous upside potential? is the question to ask… After reading the Bollore post from Bireme Capital carefully, I wanted to look once more at the detailed, complete and very complicated company structure. When searching for it, I found an interesting article from The Economist (my favority newspaper, if you hit a paywall, look for a tip in my Blogroll). The detailed structure (many footnotes included) is to be found in the 2019 urd, page 298. (colour coding makes sense further down, next gallery…)

All this cross holdings, do indeed support the claims of Bireme Capital that many shares are effectively like treasury shares hold (in)directly by Bollores stakes in other companies. In 2015, Carson Block (Muddy Waters) also talked about this on Bloomberg, describing a ‘very opaque corporate structure’ as a reason that investors do not understand Bollore — I agree. This could be a godd reason for the undervaluation! At that time, Muddy was long Bollore, but that seems not to be the case anymore. GreenWood investors presented a similar thesis in 2017 and still likes Bollore in 2020. And finally I found Woodlocks blog post with a comparable thesis (sharecount from 6:17).

This perspective gives rise to substantial upside potential but also introduces substantial risk in the form of complexity and uncertainty. I.e., the 35.9% stake of Bollore in Sofibol, translates in an effective stake in Bollore SE of 12.6% (35.9% x 55.4% x 63.5%). With the three [pink] stakes in ‘parent’ companies (Omni, Fin V, Sofibol) alone, I calculate an effective ownership of Bollore in Bollore of 14.9%. This takes not yet into account many more stakes.

Bollore might effectively own 36% of its own shares according to my calculation. This would result in a gross overstatements of share count and market cap as presented by common financial data providers. Lowering the true current market cap by one third in any SOTP valuation results in much more higher discounts to NAVs.

This structure brings huge complexity and uncertainty with it. Governance issues are obvious. Several businesses depend on ‘government goodwill’. Corruption allegations against Bollore (executives) were filed based on activities in Togo and Guinea. Such practices could be needed to preserve that government goodwill and to do business in some countries. It surely adds a risk factor.

Imagine actual cashflow streams when Bollore pays a dividend. The cash would flow through many accounts for some time and some of it would ultimately return to Bollores own accounts (if paid out to shareholders every time).

At this point you have to decide which way to go, I believe… On the one hand, you could say ‘I do not like this opaque corporate structure‘. Nobody knows what amounts of debt is owed by which company, complexity and uncertainty are just too high and you pass… This would not be a wrong decision and for sure, it is the easier way to go. It might even save you some trouble down the road. On the other hand …

Believing in the dramatically lowered share count Bollore represents the opportunity to invest in a company with appealing businesses at a huge discount to estimated NAV values. Taking into account the fact that underlying assets are most likely undervalued, increases the upside yet again. Further believing that the companies are run for the long-term benefit of common shareholders other than Bolloré family members gives us an investment case with tremendous upside potential that you may find hard to resists. Below you find the SOTP scenarios from above with the additional data-point ‘m cap, adj’ in a light orange. The true economic adj. market capitalization could well be somewhere between the two orange squares, depending on many more details of all the entities (net debt, some costs, etc.).

Summary and Decision

Bollores corporate structure is nothing short of opaque and could well be the argument for you to dismiss Bollore as an investment. Otherwise, it could be the reason to provide us with the opportunity to buy into attractive businesses.

Many assets seem undervalued, most of all UMG, owned through Vivendi. A monetization of UMG with the streaming story intact, a breakeven of the ESS segment and a humming TaL segment as well as value creation taking place inside of Vivendi are the building blocks of the upside case.

Investing in Bollore SA is not without risks as explained above, but I like the estimated risk/reward proposition based on my above analysis. I placed limit-buy orders for an initial position and hope to buy a bit cheaper in the next days …

I built a small initial position on June 18 for € 2.89 and 2.85. Bollore is another investment based on a net asset value or SOTP valuation. In general I prefer DCFs, even though I like the (estimated) risk/return proposition of Bollore and might well build a higher stake over time …

I hope you enjoyed this guest contribution post about Bolloré SA. Do you agree with my assumptions and methods used for the analysis? If you liked my article just… like it 😉

Best, s4v

(from searching4value)