David Nangle, will Creditas be a ten-bagger for VEF?

I had the pleasure to interview David Nangle of VEF. Here you can find the full video of the interview and the transcript. This conversation is also available on the Good Investing Talks Podcast.

Introduction – David Nangle

[00:00:00] Tilman Versch: Hi, David. It is great to have you on for a talk about VEF, Vostok Emerging Finance, or is it just VEF now?

[00:00:08] David Nangle: It is just VEF, that is our new official name, a smaller punch to your acronym for what was a long-winded name, and thanks, Tillman, it is great to be here.

“VEF – The emerging fintech investor” – Why The?

[00:00:18] Tilman Versch: So, let us start with your website. There you have this very short phrase that describes you, and I want to wobble a bit along it. It is “The emerging market fintech investor”. Why have you chosen “THE”, as the first word in this phrase or not “AN” emerging fintech investor? Why are they so unique? And why “the”?

[00:00:40] David Nangle: Yes. Fair question. And there is nothing pompous about being “the” as in the only one, the greatest of the world, but there is a lot of investors out there in the world and the venture capital space and private equity space doing a lot of different mandates, whether it is country, regional, segments and some are broad-based. But what we found when we started five, six years ago, there was nobody approaching fintech, which is a long-term structural phenomenal value creation trend across emerging markets, which are the biggest, most populous fastest-growing markets across the world. So, when we went out the problem of building a portfolio of the best fintech assets across the emerging world we did not find any peers or comps doing what we were doing.

When we started five, six years ago, there was nobody approaching fintech, which is a long-term structural phenomenal value creation trend across emerging markets, which are the biggest, most populous fastest-growing markets across the world.

So, it is not that other people locally, in Brazil, were not investing in some Brazilian fintech companies or some global venture capital funds did not find themselves in an Indian fintech company. But there was nobody who had dedicated themselves to this mandate totally and purely. So, I think we were very comfortable taking on the mantle of “the” emerging market fintech investor. Maybe it is because we are the only ones. So, it was “the” only one of one. But I think that is why, you know, we were very happy in branding ourselves and calling ourselves that as opposed to there is 20 out there. And we felt we were the best, then shame on them.

Competition in the emerging markets

[00:02:12] Tilman Versch: Are you still as unique as you were five years ago or is there more competition coming?

[00:02:18] David Nangle: Look, we like to think we are unique. I guess everybody is unique, but no, I think given the five, six years later, given the trends and the opportunities in the space and more specifically the value creation that we have seen in emerging market fintech assets, the competition has come. And that is just a positive factor of we are in the right space reconfirms that we are in the right space, so to speak. Has anybody else turned up to do exactly what we do in a dedicated way? There is one, maybe one other out there, and we are we. But then there is a bunch of others on a regional and then global or whatever level.

Has anybody else turned up to do exactly what we do in a dedicated way? There is one, maybe one other out there, and we are we. But then there is a bunch of others on a regional and then global or whatever level.

So, not to move forward to other questions: But the beauty of venture capital versus investment banking, that I used to work in, is that it is not a zero-sum game. You can also invest more money in a company at an angel stage than a local seed firm in Brazil can invest. Then we can invest in partners of our own, and suddenly, six funds all benefit and win from the same growth trajectory of one asset. So, competition, collaboration, it is a lot more blurred in the world of venture capital versus the world of investment banking where it is a zero-sum, winner-takes-all, you-win-I-lose kind of thing.

So, competition, collaboration, it is a lot more blurred in the world of venture capital versus the world of investment banking where it is a zero-sum, winner-takes-all, you-win-I-lose kind of thing.

What is fintech?

[00:03:43] Tilman Versch: Maybe let us wobble along to the next word. It is fintech. Why fintech and what is so attractive about it for you as an investor?

[00:03:52] David Nangle: As a word, I think it is a word that has been used and abused over the years, and I just was not aware that it took me a while to get comfortable with it. But really all it is, is financial innovation and where the future of finance is going. You know, people tend to focus on the tech and kind of try fast forward “the banking is broken”, and “new banking is going to come”, and somebody is going to develop, refine that new banking and we are investors in that. But what we are finding is that it is an evolution of a story. And it can be tweaked. It can be at the front-end customer acquisition. It can be in the production of products. It can be at the backend. It can be country or region-specific or segment-specific. So, fintech is innovation around financial services and doing financial services and delivery of financial services in a better, more efficient tech-enabled way versus what was done in the past. That for us falls into fintech and in some markets.

Fintech is financial innovation and where the future of finance is going.

It can be very basic. It can be moving from a branch to a call center, which seems the old world, but just moving from that branch to the call center in some of the more frontier markets is taking that frontline out of the way. So, moving from paper to phone, now it is the phone to digital. It does not have to be the “tech tech” end of fintech. It can just be financial innovation and moving things forward. So, it is a broad-based area of fintech in terms of ideology, but also, it is broad-based in terms of segments. It is payments, credit, investments. It is a whole range.

It does not have to be the “tech tech” end of fintech. It can just be financial innovation and moving things forward.

Limitations of fintech

[00:05:25] Tilman Versch: But if you think about the financial sector: There is a huge interlink between the financial sector and nations and the state and regulation.

So, you have limits in the financial sector. So, are you limiting yourself as an investor if you are going to focus on fintech as you bet on a certain nation? Is that right? Or is that idea wrong? What is your take?

[00:05:48] David Nangle: No, it is not wrong. With what we find with fintech: There’s no one size fits all. So, if we are looking at fintech as an ideology in Brazil versus Egypt versus the UK: They’re totally different landscapes and playgrounds for us to invest our dollars in. And we have got to take all aspects of those markets into account. And that starts with a macro-level view. The old world – you know – size of country, wealth levels of the country, populus, demographics, age level, tech enablement, how penetrated smartphones and tech and internet are in those countries. Then you move on to the system of banking that exists today. Maybe it is a new world banking system, you know, the likes of Estonia, maybe it is an old-world banking system. Then you have got all the other new tech players are doing in terms of social media. E-commerce marketplaces are all muscling into financial services and have deep pockets and lots of monthly and daily active users.

I know you touched on the point around the regulator. What the regulator will let you do or not will not let you do, how enabling they are for fintech companies, how disabling they are for fintech companies. And all these aspects feed into how and where a fintech is at, in any given country who is driving that fintech evolution in some countries, I say it is the banks themselves, Russia. And in some countries, it was the new economy, giant social media, e-commerce- China. In some countries like Brazil, it is the new coming fintech companies. And in some countries like India, it is the government. In general, you never get innovation out of a government, but we did. And they all are the ones which are moving financial innovation in fintech forward.

We do not have a color-in by the numbers playbook for each country as we go. Each country is different based on all the moving parts that feed into how we think about the opportunity in a country’s size and scale.

And it just makes it so interesting that we do not have a color-in by the numbers playbook for each country as we go. Each country is different based on all the moving parts that feed into how we think about the opportunity in a country’s size and scale – what space we want to be in small business, consumer payments, credit, and when we want to be in it. So, it is fascinating as a top-down ideology, but the bottom up from each country is totally different.

Global spread of companies

[00:07:56] Tilman Versch: So, looking at your portfolio, on which we will really go into detail later: How many of your companies are successfully present in more than one country?

We love Brazil. Brazil is the number one fintech opportunity in the world today in our view.

[00:08:04] David Nangle: We like to think they are all successful, Tilman. But what we have is: We have 14 companies in the portfolio today. We are heavy neck-deep in Latin America. We got six in Brazil. And that is by design, not by default. We love Brazil. Brazil is the number one fintech opportunity in the world today in our view. And I have got two in Mexico, that is rolled on from being neck-deep in Brazil, next-door neighbor, investing with the same partners and in the same terrain, we have got two there. And we have just made our second investment into India. So, they are kind of markets where we are more than one investment in, but we will see Brazil dominate versus the others. We have been in two investments in Russia, Tinkoff – we are out of, and we have shown later…

[00:08:53] Tilman Versch: Which of the companies have the possibility to be in Brazil and Mexico or Brazil and Argentina or Russia and Poland as players?

[00:09:04] David Nangle: I think if we pull back more fundamentally, how we think about things: We love companies in single countries and financial services. You touched on the regulatory point. So, the regulator is different from every country. So, what tends to happen? A lot of startups tend to succeed within their own borders. And it is easier for a Polish person to succeed in Poland, a Russian to succeed in Russia, or a Brazilian person to succeed in Brazil versus Mexico. So, we tend to love single country scale play. Then most of our countries are, most of our companies are that. But specifically, to your question: Creditas is one, that is moved beyond Brazil now into Mexico.

We hate people running off to more markets when they have not succeeded in their own market.

But once again, it is of the base of strong success in its core market. We hate people running off to more markets when they have not succeeded in their own market. But Creditas to us is very front and center in that. Konfio can do something similar in Mexico. But then we have a couple of companies that are multi-country players and that is more like TransferGo in the remittance space. So, it feeds its model into many countries like Jumo, which is in mobile financial services and banking as a service in Africa. They are present in many countries. And then there is Revo that is taking the “Afterpay” business out of Russia, while still being in Russia, but they go from Russia into other markets of Eastern Europe. So, there are a few multi-country plays. But the singular country plays are the ones that we love because of their focus

[00:10:26] Tilman Versch: I wanted to do this in a video. What about cash??

[00:10:32] David Nangle: You should be doing euros. It should be dollars. Dollars are always better than Euros. They look better.

Cash from the perspective of a fintech investor

[00:10:39] Tilman Versch: Next time dollars then!

What is your take on cash? Is it kind of your enemy, if you are thinking about cash societies like Mexico, where still a lot of the transfers are done by cash? What is your relationship to cash as a fintech investor?

[00:10:57] David Nangle: Yeah. It is not so much the enemy, but it is the past. It is history. It is inefficient It is disease-ridden. It is costly. It is non-traceable from a feed into the gray and the black economy. So, you know, I think the war on cash is there for a reason globally. And it has been in some places led by governments because they want to digitize everything. So, this transparency in all movements of financial services, and that is good for managing the economy. And it is good for tax take and for fintech. It is great because it is digitized. You can understand that so you can score small businesses and individuals better, and you can give them better financial products because you can see all the transactions as opposed to not seeing the transactions.

So, I think the war on cash is a very positive one both from a government point of view and from a company point of view.

So, I think the war on cash is a very positive one both from a government point of view and from a company point of view. And the trend is clear global, that cash is a dwindling proportion of overall savings, spend and use in society. And that is a net positive for fintech. So, I did not, we are quite comfortable with the trend. It is positive for what we do. You know, I think with COVID it kind of got a step-change in terms of pace. As some countries like India were a bit more dramatic and they had a demonetization push. So, you get these kinds of step changes, but the gradual move is towards a cashless world.

[00:12:22] Tilman Versch: And that is an opportunity for you?

[00:12:25] David Nangle: Yes. Yes, it is indeed.

Exchange rates in the investment process

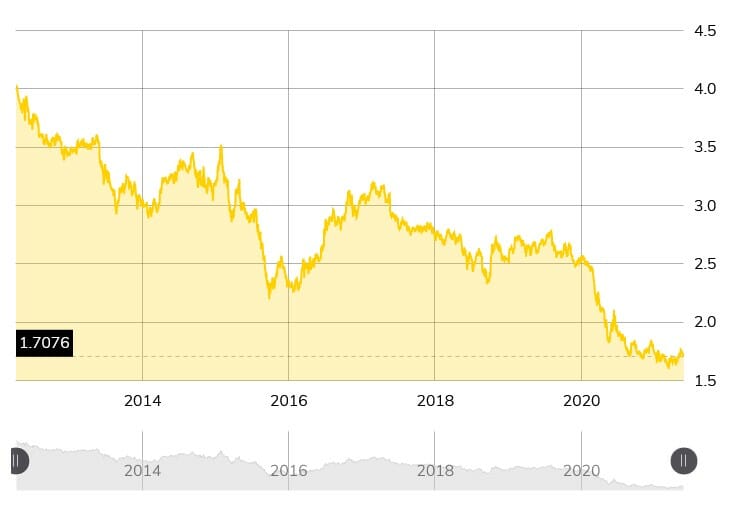

[00:12:28] Tilman Versch: Let us also look at currencies. You have a big portion of your portfolio in Brazil, and here is the chart of the Real to the Swedish currency, Real to SEK. How are you affecting this in your investments and how are you going about currency development? That does not look that good. And since I think it took from 2015 to today.

We are structural growth investors. So, we are looking to invest in the best companies in the highest growth markets in the structural trend that is fintech.

[00:12:59] David Nangle: Nope, we are very aware of the movements in the Brazilian Real. As we are in the Russian Ruble and the Mexican Peso and the Turkish Lira and many others. What we are at a core is: We are structural growth investors. So, we are looking to invest in the best companies in the highest growth markets in the structural trend that is fintech. These companies are growing in many cases, two or three x a year, and that compounds over many years. In the emerging markets, we get the headwinds of currencies whether it is in one fell swoop in any given year when the Egyptian Pound will move 50% and a Mexican Peso, or what it is gradually over time versus hard currencies like the Swedish Kroner or the US dollar where they will move five or ten percent per annum. What we are betting on and what history has told us is, that the structural growth of these winners will outweigh any currency headwinds that are coming their way.

What we are betting on and what history has told us is, that the structural growth of these winners will outweigh any currency headwinds that are coming their way.

So, we accept the currency headwind. I will not say we welcome it, but it is a fact of investing in these economies and what it does do: It keeps a lot of the competition away so we can find the best assets at the best prices. We can enjoy that structural growth story. Albeit we need to factor in those currency headwinds. Now, if you look at Turkey, which is a classic example, and you know, you bring up a chart comparing the Turkish Lira versus US Dollar over the last 10 years, and it is horrific. We made a 60% IRR on our iyzico investments, over a two-and-a-half-year period. And we invested when the tanks were on the streets. We invested whether they were, it was volatile, but it was a company that was doubling and tripling year on year. So that is one of the headwinds or cons and in our investment case. But once we are investing in the right companies, we tend to outgrow those headwinds.

I will not say we welcome it, but it is a fact of investing in these economies and what it does do: It keeps a lot of the competition away so we can find the best assets at the best prices.

[00:14:38] Tilman Versch: So how do you calculate the currency in your framework of valuing a company? Do you say: With the Real, it is like it goes down 15% a year, and the company can grow like 30% or 50%?

[00:14:57] David Nangle: Whenever we are making an investment, we always have a 30% – three, zero – IRR hurdle. And so, we are forecasting these companies out five, seven years, and we are looking to get a realistic, realistic exit on them, but we are, we are factoring in into our forecast, a 10% headwind on currency per company, per market, per annum. So, we are not getting out, you know, we are not trying to forecast the currencies per se, but we are just taking a 10% headwind into our models, which I think in emerging markets, we might get lucky. It might be flat. We might get unlucky. It might fall more. But it is a realistic headwind for building in a buffer.

Difficult emerging markets to invest in

[00:15:37] Tilman Versch: Thank you. So, the next point in your sentence on the website is the “emerging market fintech investor” or the “emerging markets”. Are there any emerging markets where you say as an investor, I could imagine going on holiday there, but do not invest?

[00:15:57] David Nangle: First, I love emerging markets. I love the size, the scale, the shape, the volatility. They are fascinating. They are never dull, they are the future, but the path is not linear in any way, shape, or form. It is a zigzag route to any kind of success. But where would I go on holiday, but not invest within the emerging world? That is a bit too hard, I guess.

Argentina, I am a big fan of Argentina as a country. But as an investment destination, it is a hard country, almost from a macro level, more so than a micro level. It is a country that has been in a difficult leadership macro place for quite a long time, but it is a country that I have been to, and it is phenomenal as a country both the Capital, the countryside, and the coastline. So, I would spend time there. I do not know if I would invest there as an emerging market and that is for me from a finance and family point of view.

Personally though, I like a bit of adventure. So, there are many emerging markets that I would travel to that I would not invest in, be that Belarus, Venezuela. But I would not bring the family and I would not bring the best dollars there.

Competitive markets

[00:17:10] Tilman Versch: And which emerging markets do you say: They are interesting. It is worth studying them. But the competition is way too strong that we could add value there.

China is an educational playground for everything tech and fintech, but where do we start as investors in that market? I just do not know.

[00:17:21] David Nangle: China, all about China. China is an educational playground for everything tech and fintech, but where do we start as investors in that market? I just do not know. Sitting in Europe with a small team we have managed to take on countries as big as Brazil, Mexico, and now India: Find their place. Find good partners and find good assets. I would not know where to start with China. There is so much to learn from that market.

Assessing risks

[00:17:50] Tilman Versch: I do not want to blame these markets, but with India and China: I had some interviews with other investors that said you must do work on the ground, be close to the people because there is a certain risk of fraud. How are you going about this risk in emerging markets?

[00:18:08] David Nangle: I would not put any single emerging market in that bucket. Every emerging market is a difficult country. They all have their own specific quirks, whether it is politics, geopolitics, rule of law, governance, transparency. They are all on a path to better, I would think, but they are all difficult terrain from an investor point of view. So, first and foremost, with us, it starts with the people that we are investing in. We are talking about the right people, ethical people, people you get to know over time. We do not rush into any investments and the journey professionals – they have spent time in worlds like a startup or a new economy or tech or also a little bit consultancy firm. We spend a lot of time with the people. Then we spend a lot of time with the “people around the people”. We are generally not the first investors in most companies. So, in India, we are investing with people like Sequoia, Accel, big investment funds in Brazil, that’s Kaszek and Redpoint.

We spend a lot of time with the people. Then we spend a lot of time with the “people around the people”. We are generally not the first investors in most companies.

People, people around the people. And then even after that, then the “legal” kick in. We have in-house counsel and out-house counsel, and a lot of these companies’ jurisdictions are outside their countries that are in Delaware or Cayman’s or Singapore, and then the “legal” kick in to save us from ourselves if everything goes wrong. But a lot of this is around the people. And then once we are in, we are board members. So, we are active investors. We are on the board of 12 out of 14 companies. As a team we are getting, you know, sometimes daily updates, weekly updates, monthly updates. We are on quarterly board calls. There used to be board visits. And, but obviously, COVID put a few headwinds on our travel in this period. But we get back to that and get back on the ground. And we have got a lot of venture capital partners as well, who are co-board members. So, a lot of work goes in that.

The lean setup of VEF

[00:19:50] Tilman Versch: On the active investor point: How scalable is your active approach? You have a very lean setup. I think it is seven people currently working at VEF. And, so there is a certain problem if you have more companies in the portfolio where you are active. Or is there still room to be active?

[00:20:07] David Nangle: There’s room to be active. I think what we have done very well is building the team with the size of the company, the size of our NAV, and our portfolio of assets. So, we just made a recent hire, Tilman, a guy called Carroll here in Dublin. So, we are up to eight people now as part of the team with a portfolio of 14 companies. We have got five people on the front end and hunting, gathering, working on investments. There is more that we can do with the team that we already have. So, I think we are a good size team to do more. Each person can be very active in five companies while also doing pipeline, while also doing all the other things that we do. So, there is a scale from there.

I think what we have done very well is building the team with the size of the company, the size of our NAV, and our portfolio of assets.

Choosing investments: Quantity vs Quality

[00:20:51] Tilman Versch: You mentioned the word ‘Pipeline’. How have you built the pipeline for ideas to bring interesting opportunities to Sweden and to you?

[00:20:58] David Nangle: It is nonstop in terms of the pipeline; it has become very busy in each of the markets that we play in terms of entrepreneurs and capital supporting them and companies coming through in each of the sub-segments in fintech and in broader insurance and in embedded fintech. So, I think year to date, we have looked at over a hundred companies and as this year alone as a team. Some are our first calls; some were not done because it does not fit or there is a second or third and we get into it. So, it is non-stop the pipeline. Some of it comes from our venture capital partners on the ground, in these markets and owners because we are the emerging market fintech investor, and there is not many of us. So, they tend to come at us. Others come from our founders who we know very well on the ground. And others we are just searching. We like certain spaces, and we do the work, and we try to get into it.

And we have a high bar. We look for a bunch of things in any investments and, you know, we have not found an investment this year that we have done yet.

So, I think the pipeline is not our problem in terms of quantum, but the quality is. And we have a high bar. We look for a bunch of things in any investments and, you know, we have not found an investment this year that we have done yet. We have done two investments this year, but they were from last year in terms of closing this year. So, we tend to do one, maybe two new investments a year. We are in no rush. We just sit back. We wait for the buses, they come, we watch them go by and when we find one, we like we try and jump on.

What kind of investor is VEF?

[00:22:20] Tilman Versch: So then let us move on. Let us try to touch the last word of your small sentence on the website: the investor. If you type in your website in a browser, it ends on VC. Is this really the kind of animal/investor you are? Or are you different from what we see?

We’re very fundamental VC. We do a lot of work. We do a lot of thinking.

[00:22:36] David Nangle: We’re very fundamental VC. We do a lot of work. We do a lot of thinking. We do not jump on a call with somebody and go, we love you. We love that idea. Take some money. We really analyze countries, segments, and opportunities. Then we find micro-level opportunities and teams, we do a lot of work on them. A lot of the time we let them raise money, seed, series A, we pass, we pass. Then series B comes along. We have seen them get to where they need to be and that is becoming organic and the right time for us to put capital in. So, we are investors, long-term investors. We are not traders, but we are very focused, very diligent in what we do. We have anti-FOMO. We do not mind missing stuff because it comes around and around and around, and we grab it when it feels right to us.

We have anti-FOMO. We do not mind missing stuff because it comes around and around and around, and we grab it when it feels right to us.

Timeframe

[00:23:37] Tilman Versch: So, in what kind of timeframes are you thinking in as an investor?

The beauty of our company and our investor base is we have permanent capital. We have forever money.

[00:23:40] David Nangle: The beauty of our company and our investor base is we have permanent capital. We have forever money. And premieres for a long time but you know, the way we see our companies in the countries that we are operating in is a long-term game. You are not going to build, you know, the Stripe or the Square, or the JP Morgan of Pakistan or Egypt in five years. It might be 20 years. And that might be 20 years, a 50% growth. And we want to be there for each of those years of that 50% growth, albeit every three or four years, you might get a currency move and you might get a step backward, but that is the game that we are in.

So, in Turkey, we were in and out of a company in two and a half years. We did not plan to b. We have got an offer we could not refuse. So, we did not. That was a good return. But looking at Tinkoff in our portfolio in the past, that is one that the Vostok group invested in back in 2005, and we only exited the final piece out in 2019. I look at something like Creditas or Konfio in our portfolio today. They are companies that I can see us being in for 10, 15, 20 years given the space that they are in and the scale of the opportunity, their track record of delivery. That kind of the hundred percent plus growth may become 50% may become 30%, but we want to be there to enjoy that journey.

Selling

[00:25:00] Tilman Versch: What is the reason for you to sell?

[00:25:06] David Nangle: First, there are a few things in that, Tilman. Like the diligence of return on capital. We are expecting 30% return. So, if there is an offer on the table that gives us 30% plus returns in IRR terms – we will take it seriously. Because that is our promise to shareholders. More importantly, I think, are the founders. The founders come to us, and they say: We want to sell. We back them. We are founder first. And that is what happened in iyzico. When the offer came, the founders came to us and said, this is something we would like to explore and maybe do. And as much as we want it to be there for longer, we were very happy to support them in their exit.

So, to keep a certain level of exits going as you go through the cycle is a healthy discipline to show the cash comes in as well as cash going out. And investors like to see that.

I also think it is good from a professional process point of view is to have some exits I will not say investing is easy, but investing is easier than getting money back. So, to keep a certain level of exits going as you go through the cycle is a healthy discipline to show the cash comes in as well as cash going out. And investors like to see that. But it is fundamental support of founders with founders on their journey once they are succeeding and I am looking to exit with them at the right time, IPO, or M&A.

Improvements over the past 5 years

[00:26:19] Tilman Versch: You’ve been five years plus with VEF. Where have you gotten better and where has VEF gotten better? And where do you still need to improve or want to improve?

[00:26:29] David Nangle: Yeah, we have got better at everything. You know, kind of thinking back, I do not know if you think back to your first interview, Tilman. But we think back to when we were raising money back in 2015. Would I have given us money then? I do not think so. People did. We are very grateful to our investors from the start, and they believed in us, they backed us. And, but we were raw. We had a long career in emerging markets and financial services. We knew these countries, these terrains, the old-world banks, the future of finance, as we saw it through Tinkoff in Russia. But we were still nascent, and we are young in our investments careers as that part of our career.

So, we have gotten better in absolutely everything. But for the most part, it is really on the investment side: Finding investments, the diligence in the investments working with our investments, growing up with our investments in terms of what works, what does not work, mistakes made, battle scars – which are the best ways of learning. Unfortunately, it is with capital depreciation when you make a mistake. But overall, our mistakes have been small – so far – and our wins have been big. So, net-net it has been a positive education journey as opposed to one of those investment education journeys, which ends up with a zero. And we all learned a lot from that, but we got a return. I think over the last five years we have been delivering 27% returns on average per annum while getting an education.

I think over the last five years we have been delivering 27% returns on average per annum while getting an education.

But where can we get better? I think we can still get better at working with our companies and help them. It is a real goal of ours to be the number one investor for each of our companies. And that just comes with time and experience, and you know, I think on the investment side, you can always get better: better at being quicker with our pipeline, more efficient, and finding the assets that we want.

Why did he join VEF?

[00:28:18] Tilman Versch: So maybe also looking back at 2015 or 2014, when you were asked to work at VEF: What made you take this opportunity?

[00:28:28] David Nangle: Yeah, look the forces coincided for me with VEF – or Vostok as it was. And I was in investment banking, working at Renaissance Capital in Russia. And then in London at an emerging markets Investment bank. And I was head of research and head of financials. I was nearly there for 10 years and loved every minute of it. It was an amazing place to work and an amazing bank and great people. But true, the work on Tinkoff Bank which I worked on as an analyst and in banking at Renaissance Capital, worked on the IPO and their exit. I got to know all about the top management team. They got to see the investors around our story, Goldman Sachs were in there, Vostok NAFTA, and Per Brilioth, who was the guy behind Vostok Nafta.

So, it is kind of like my ideology moving out of banking, into running a fund of some kinds that are classic venture capital or listed investment company to invest in future Tinkoffs cross-referenced with Per Brilioth on his timing, moving Vostok Nafta away from what was marketplaces on one side and some fintech on the other. So, the conversations became organic as opposed to Per approaching me and saying: “Come on board and do this” or me approaching Per and I should come on board and do that.

We just kind of got together and kept on talking through the Tinkoff process, through the exit, talking to some of the investors behind Vostok. And almost regardless, he came to the point where he was saying, I should come on board. We should split marketplaces on one side. Fintech on the other. We should build two separate entities. And we should raise capital around the fintech entity. That is a rebrand, also VEF and VNV. And off we go. So, easier said than done, but an amazing time opportunity meeting of minds in hindsight as it was a great thing to do at a great time. And I say that because we succeeded. Clearly, success makes you feel happy in hindsight.

Plus COMMUNITY

Discover the Plus Investing community

The Plus community is a great resource for professional investors. Members get support to grow their business and careers, are easily able to connect with other investors and can share ideas and join in-person events.

His motivation

[00:30:28] Tilman Versch: So, what has changed in the five years in your motivation after you started doing? Have the things that drive you changed?

[00:30:39] David Nangle: Look, the motivation was always long-term in nature. The older you get, the more long-term you get what your vision. It is bizarre but true. We are looking to build something special here over the term to have a portfolio of the winning and biggest and best fintech companies across the emerging world. That is something that is taking time and it can take forever cause innovation is constant and these companies can keep on growing to be the future of Barclays and HSBC and JP Morgan’s of their market in their specific spaces. If they are in our portfolio, we will grow with them. So, our goal, my goal is for this to be something of real size. Real special people say emerging markets financial services, the future of finance, they say, VEF. It goes hand in hand at the same time to continue to create shareholder value as we go. It is key.

Real special people say emerging markets financial services, the future of finance, they say, VEF. It goes hand in hand at the same time to continue to create shareholder value as we go. It is key.

We need to make money for our shareholders and deliver a great return. All with a growing ESG overlay and because the impact of what our companies do is very important as well. So, I think these are the motivations. It is about creating something. We are investing in companies who are themselves building businesses. While we ourselves are a startup building a business. We are a six-year startup. We have got eight people. We started with sub $100 million of NAV and market cap. And now we are $400 million of NAV and market cap. We had one investment at the start. We have had 16. We have got two exits. We are building our own startup story and we’ve kind of gone from an early seed stage series to series B or C stage. But there is a lot more to go.

It is about creating something. We are investing in companies who are themselves building businesses.

Views on retirement

[00:32:09] Tilman Versch: If this concept of retirement exists for you: Will we see you retiring at VEF?

[00:32:17] David Nangle: I do not like the word retiring. I am a worker. I like to work. I like to be involved, to be active, to grow, to travel. So, my presence and my foreseeable future is doing that at VEF. I am with a great team with great backers and great shareholders on a great journey. I do not see that changing in the future, it may take on other things. Things happen, life happens, you have got to be open to these things. But that is nowhere near my top processes at this point.

The relationship with VNV

[00:32:49] Tilman Versch: You already mentioned VNV. How would you describe your relationship? Are they the parent, the brother – someone else?

[00:33:00] David Nangle: Probably all the above: The grandfather, the wise uncle, the parents, the brother. I do not to know. Pick your family member. But they are our benchmark. That is where we have come from. That is where we were born. They had been doing it for a lot longer than us with a lot more track record, a lot more success. We live and learn from VNV, so I have only got good things to say about them and we just watch when we share a similar history, similar ideology. Whenever I get a question, and issue, something. We pick up the phone. Per Brilioth sits on our board. So, he is very directly involved in terms of influence, ideology. That is the history and that is the present and probably the future.

[00:33:47] Tilman Versch: What have you copied from them and where are you daring to be different?

[00:33:51] David Nangle: Daring to be different (laughs). Look, I think. Copying: We’ve had similar levels of success as in investing in the right companies that create value. That is key. And I think we are both founder friendly and founder first. And that is a similar ideology.

Dare to be different: Look, I think, individually where we are different people running different companies. So, I think they have gone to developed markets. We are staying pure in emerging markets. I do not like developed markets. Developed markets are too stale, too boring, too competitive. I have no interest in France or Germany, no offense, or the USA. It is all about Brazil, Pakistan, Egypt, Russia for us and at VEF.

So, I think they have gone to developed markets. We are staying pure in emerging markets. I do not like developed markets. Developed markets are too stale, too boring, too competitive

So, is that different? That is just our core focus. And that is one thing. Maybe on the team front – we have a bit deeper of a team, even though both teams are small and lean, I think ours is less lean. Is that daring to be different? Maybe a slight difference in ideology.

How is the competitive landscape?

[00:34:53] Tilman Versch: Competition was already a point. You did not say a lot about. So, how is the competitive landscape in the markets you are investing in compared to France, Sweden, Germany?

[00:35:04] David Nangle: It is less, but it is getting busier I would say. Because when we started doing this, there was nobody who is going to Egypt or Pakistan put investible dollars in. But they are now. I think Brazil, India, the bigger emerging markets are getting relatively hot. What we have probably found in the last 12 or 18 months is a few, few forces have collided: One is a very low-interest-rate environment globally. So, there is a lot more capital out there. Two is the fact that nobody’s traveling. So, everybody is on Zoom, and so places like Egypt and Pakistan look a lot less intimidating on Zoom than maybe they do in real life. So, we are getting investible dollars from places which normally would not be in these markets coming through. But these are waves and cycles.

The beauty of what we do is. When Brazil gets hot, we can invest in Mexico. When Mexico’ is hot, we can invest in Egypt. There is always a place that is less hot if the valuation is a key aspect of what you do.

The beauty of what we do is. When Brazil gets hot, we can invest in Mexico. When Mexico’ is hot, we can invest in Egypt. There is always a place that is less hot if the valuation is a key aspect of what you do. But also, you know, we are quite comfortable in our own skin in terms of what we do and our dedication to emerging markets and fintech. And it generally helps us get into the right investment opportunities – even if there is a lot of competition out there, which is turning up for the first time in these markets.

Skin in the game

[00:36:21] Tilman Versch: How much of your personal wealth is invested in VEF? You do not need to say a percentage, you can say it in some other measures or…

[00:36:32] David Nangle: Let us put it this way. Maybe it is half my balance sheets, or my net asset value is VEF. Give or take if you take a full suite of pensions and home. And I did not know how much my kids are worth, but when you put it all together. But I would like to think given the path that we are on, that my value in VEF will dwarf everything else, and that is the key.

Maybe it is half my balance sheets, or my net asset value is VEF.

I have got no other key investments. My only investment, my only focus is the main job. That is VEF. And I do think about VEF from a personal financial point of view, but that is not my prime. I think that is the output. And based on the function of delivering a great company and a great product and great shareholder value, then I will wake up one day and it will be worth a lot.

Compensation at VEF

[00:37:19] Tilman Versch: You already mentioned you have some news: You have person number eight coming to VEF. How is the team aligned with shareholders? How are they compensated with stocks?

[00:37:28] David Nangle: For VEF: It is a very much a core compensation package around cash salary and bonus and pension. But the upside is all stock. Long-term incentive plan: L-Tip. That is me and the broader team. Everybody is involved, and we all get a piece of it, and it is a five-year program, and it is all about creating value for the shareholders. And once we do that over the medium term in return, we will get our piece.

Buybacks

[00:38:00] Tilman Versch: What do you think about buybacks? What is your framework for them?

[00:38:03] David Nangle: They’ve got a place in an investment company. Similarly, we can put a dollar to work in a new pipeline company, so something totally new. We can put it to work in our current portfolio. So, following on and putting more capital into them, or we can buy back our own shares. What we are looking for is 30%, three, zero IRR, on every dollar that we put to work.

What we are looking for is 30%, three, zero IRR, on every dollar that we put to work.

So, you know, we haven’t had to do anything extensive on the buybacks to date because the share price has been in a good place, especially more lately in a good place and close to NAV, but going forward, if there was a massive dislocation in our share price and we were sitting on cash, the best thing we could do from a value-add for shareholders point of view is buy back our shares. So, there is a place for it, it is part of our investment thesis, but we have not had the opportunity to do something aggressive on that front yet.

Portfolio construction

[00:38:55] Tilman Versch: At this point, I want to close our looking at the small sentence you have on your website – with all the details of the different words. Now I want to move on to your portfolio, which is also a very interesting topic. When you think about your portfolio, is there any metaphor you are using or any picture you like to describe your portfolio with? Or how are you going about the construction, the framework of what is in your portfolio?

[00:39:24] David Nangle: I think the best way of answering that question is to talk about our view on concentration. We actively seek concentration. If we have a concentrated portfolio, it means we have found winners. So, when we find something like Tinkoff in the past or Creditas today. And we can see we are on the inside. We sit on the board or very close to these companies and we can see that they are breaking out and winning in their space. And especially when they are at a later stage, we try to get as much capital into them as possible.

And we can see we are on the inside. We sit on the board or very close to these companies and we can see that they are breaking out and winning in their space. And especially when they are at a later stage, we try to get as much capital into them as possible.

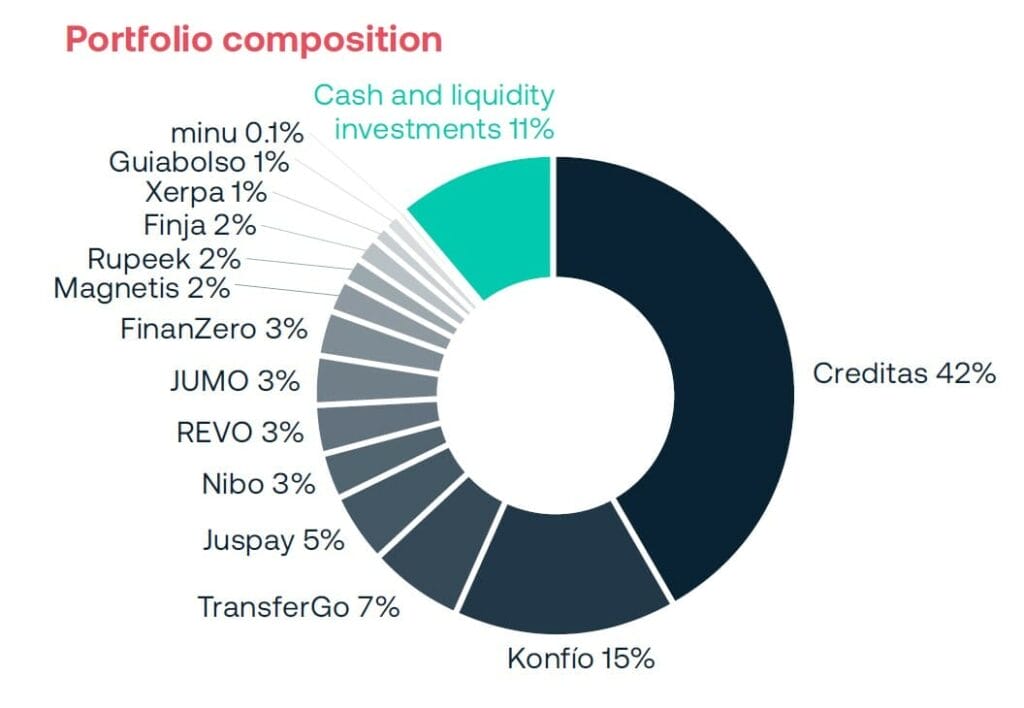

So, Creditas today is 42% of our NAV. And we are very happy for that to be 50%, 60%, 70%. Then we move to exit. We take capital off the table at some point. And we do it all again – in theory.

So, are we looking at a kind of portfolio theory or portfolio spread across different countries across different stages? No, we are not. We are looking for on a micro level, the best fintech company opportunities. We get them into the portfolio. When they are performing, we look to concentrate the hell out of them. And as we have in Creditas and that is, that is good news for us. So, that is how we think about things.

So, are we looking at a kind of portfolio theory or portfolio spread across different countries across different stages? No, we are not.

So, today we are Brazil heavy, and we are Creditas heavy – or LATAM heavy. Three, four years ago we were Russia heavy. Now in five years’ time, we might be India heavy. And that is geographic. And that might be company-based, but you know, we are quite open to that. And that is, that is the way we think about it.

Pain points

[00:40:54] Tilman Versch: What kind of pain points are companies you are investing in addressing?

[00:41:00] David Nangle: Well, it is around the price point. Especially in Brazil, the price points of all financial services are astronomically high. Yeah, payments can be 30 days and you can pay 3% to 5% to process payments, money market funds. You can charge 2% credit for consumer credits.

It can be a 100%. So, a lot of our companies are providing a) a better product, b) at a better price, which is not hard given the incumbents and their cartel. Also, for user experience, we see a much better user experience across most products and most of our markets. Then there is the aspect of the un-banked and under-banked. Jumo is providing financial services to people for the first time in Africa. So, you know, working with the MNOs and mobile operators and the banks on the other side. They are delivering a financial product to the owner of the banks.

And so is Konfio in Mexico, where small businesses are just under looked by the big bank. So, when it is a first product or a need for the product in wide-open spaces. What is a better user experience? Whether it is a better price point? We are talking about all those problems with different companies in different markets.

Replicating models of the developed market in emerging markets

[00:42:11] Tilman Versch: How much copying of concepts that work in the west can be found in your portfolio?

[00:42:18] David Nangle: We love a bit of copy-paste. Replicating is the easiest thing to do in the world – with a bit of local flavor. So, what tends to happen, Tilman, is in the developed emerging markets, a lot of models pop up that are very similar to the developed markets.

So, what tends to happen, Tilman, is in the developed emerging markets, a lot of models pop up that are very similar to the developed markets.

So, online payments or small business lending, some like Square or Stripe exist in the US or in Europe, I guess, N26 or Tink, or Klarna – these models pop up. They tend to compliment in Brazil or Turkey, more developed emerging with quite decent banking systems.

We did our iyzico in Turkey in the past online payments processing. That was very much the Stripe and Adyen model for Turkey. A bunch of Germanic Turks came back from places like Hamburg and Nurnberg moved to Istanbul, they are ex-Klarna, ex-PayPal, and they built the model. They are pretty much copying the Stripe or the Adyen model, but for a Turkish market.

So, I think in those markets, which are developed emerging: There’s a lot of copy-paste, replicated execution with some local flavor. And for us, when you get the right founders doing that, it is great. There is a good playbook there, and it is probably the quickest way we get the best return on capital.

Other markets and other models are very fit for purpose in the frontiers where it is very early stage, very cash dependent. And it is copy-paste, replicate and execute. So, Jumo is a totally unique model for a unique space in Africa, versus other things like Creditas in Brazil, which is, you know, very similar to what happens at Carvana or Rocket companies in the US or Konfio in Mexico, which is building like the Square Capital of Mexico. So, yeah, there are a lot of different examples there.

“Loss-making” investments

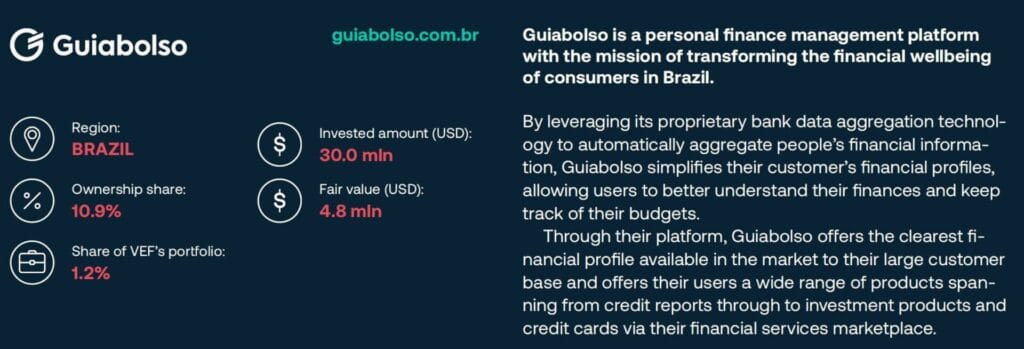

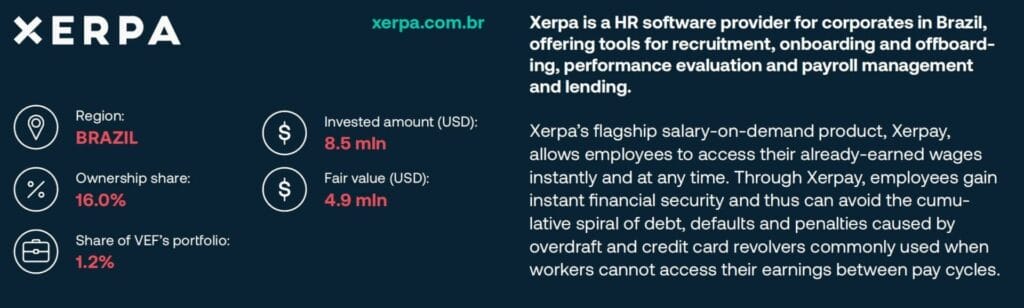

[00:44:02] Tilman Versch: You have some great investments in your portfolio, but as you said at the battleground investments, you learn a lot. And that is why I want to talk about the investments that still are below the initial investment. I hope I spelled them right. You can correct me then. And please do it. The investments are Xerpa, Guiabolso and Jumo. They are just a bit and sometimes even more below your initial investment. Why did the value decline after your investment in these companies?

[00:44:49] David Nangle: I will talk about all three. I am quite happy because it is people, they have all got stories where we have got a more conservative valuation, but they are looking good at this stage from these lower valuation marks. But, you know, Guiabolso is very much in the personal financial management or open banking space – very much like Tink does in Europe. But it was focusing on a B2C model, initially, and the B2C model was very hard to convert in Brazil. So, we spent a lot of time trying to, we had a lot of users, a lot of active users, middens, and we were just trying to convert that into a profitable revenue-based model. And it was very difficult.

We found that over a two to three years period. So, we marked that down aggressively as that model effectively was not working. And, but what we have found is that open banking is a big thing globally in Europe and now in Brazil. The regulators are forcing it and our technology is well placed for that. In the B2B open banking space, Guiabolso is front and center and you can almost see a second coming or a second wave or growth trajectory in that. But I think what that NAV mark shows to our auditors and to our investors is, you know, we are quite quick to mark things down for conservatism, if something is not working, as opposed to keeping valuations where there may be not justified at that point.

But I think what that NAV mark shows to our auditors and to our investors is, you know, we are quite quick to mark things down for conservatism, if something is not working, as opposed to keeping valuations where there may be not justified at that point.

I think Xerpa is one where it is in the salary advanced space. So, it is giving you employees access to your earned salary in advance of the end of the monthly payroll. And we invested in that in Brazil just before COVID. And it was just launching the product. So, we’ve kind of had a standstill – as Brazil has been in a standstill and human resource departments have been in a standstill for that window. So, it kind of took us a year delay. So, through COVID and with the currency and with Brazil, we just got more conservative because the model had taken a long time to really pick up and grow. And it is only starting now. So, it is kind of like we lost a year, but that brought in conservatism in valuation.

And the final one Jumo is one where: That’s really starting to hum now. It is really, the partners are starting to kick in. This is Africa, there is an element of credit. So, during COVID, we got very conservative – just in case – on that model. And, but now we are starting to come out at the other side. And I think you have seen the NAV marks of Jumo in the last quarter, but things are starting to come back in the right direction. And that is a function of how well the business is doing.

Evaluation process

[00:47:14] Tilman Versch: So how are you going about the NAV write downs? Or you just saying: Are they a sign the business is not working that good? Or how are you going about these re-valuations and the communication with your investors?

[00:47:29] David Nangle: We work very closely with our auditors: PWC. And we mark our companies to the last investment round. So, there is a big funding round. We marked them at that level and that is for a period of up to 12 months. And then after 12 months, we move to a market-to-market model, so a more fundamental realistic basis. So, for each of our companies, we have a financial model. We have a quarterly or annual valuation that we roll on a quarterly basis.

And if those companies are not performing versus when we initially invested, according to that plan, we happily mark them down to a new valuation based on how the markets are doing, how their peers are doing, multiples of the peers, how the currency is doing. As we have seen, the currencies can move against.

And if those companies are not performing versus when we initially invested, according to that plan, we happily mark them down to a new valuation based on how the markets are doing, how their peers are doing, multiples of the peers, how the currency is doing. As we have seen, the currencies can move against.

So, in many cases, we are moving things up in valuation over time. In some cases, we move things down to move back up. So, it is, it is kind of an iterative quarterly process, but it is very formal, very mathematical done by orders. And you know, we are quite quick to mark down when we feel a bit more conservative about them, as much as we are quick to move them up when they are on fire in a good way.

Can “loss-making” investments be turned around?

[00:48:33] Tilman Versch: Do you expect these companies to be a good investment or is there any risk that they might be a permanent loss of capital here?

[00:48:41] David Nangle: There is a few things. What we have marked out as the NAV today is the point: So, history is history. So, whatever we put into any company in the portfolio in the past is point one.

But the most important point for any day when we wake up is what we have in our NAV today. And that is reflected in our overall NAV, which is about $400 million, and reflected in how the market sees us on our market cap. So, we always ask ourselves from here today: How will this company do? Whenever companies are looking for capital: We ask them – as of this point, it is not historically – should we give them more capital for the buy they can create from here going forward?

So, all three companies are in a much more stable/positive footing in their journeys, versus when we took down their NAV marks. And a lot of that NAV mark movements was during COVID, conservatism, and they are starting to come out of that.

Investing time in certain companies

[00:49:37] Tilman Versch: How much time you, you said you are an active investor? How much time do you need to put in these marked down companies? How much time take for the winners in comparison?

[00:49:50] David Nangle: It is interesting. We do not really think of it as: Do we spend more time in our bigger companies and our smaller ones – that one that are increasing in NAV versus decreasing in NAV?

We have a portfolio of companies, who have got a team of eight different people, you know, aligned with each one and we work with these companies to help them out in any way we can, whether it is raising capital, modeling, decision-making, and we look to help them win at any point in their cycle. So, we do maybe on average, tend to spend more time with the bigger companies of our NAV because they will have more impact.

So, the more positive impact we can have on Creditas and a Konfio the more positive impact it will have on our overall NAV and hence our share price and for shareholders. But that is only marginal. And what we tend to find is that the bigger companies, because they have got to a stage where they are big, more professional, deeper, they maybe need less of our time for some of the smaller companies that are only small parts of NAV more of our time. So, it tends to evolve.

Creditas

[00:50:51] Tilman Versch: Interesting. So let us look at your biggest holdings. Creditas is really the biggest holding. I think it is 42% – at this size you have them in your portfolio now. What is your investment thesis for Creditas? And what do you expect in the next three years from the company?

[00:51:11] David Nangle: I am biased, but Creditas is a special company. And the beauty in our world is you come across one of these every so often. And when you have it, you know, and you just wrap your arms around it. Creditas – it starts with people; I go back to this point.

I am biased, but Creditas is a special company. And the beauty in our world is you come across one of these every so often.

The founder is a person called Sergio Furio. He is Spanish from Valencia, but he moved to Brazil with his wife at the time. He is ex BCG. So, he is a consultant, super logical, very energy driven, very methodical in his thinking. He has got an excellent team around them and some of the best investors in the region. And more importantly, he is playing into a scale opportunity place, which is secured lending in Brazil.

So, this is lending to people by using collateral against their home or against their car or against their payroll. So, it is lower risk lending in its nature. But what Brazil has is a very big unsecured loan book at horrific rates. So, he is lending to people at much lower rates, you know, bigger amounts, better economics and safer effectively.

So, instead of you going out and borrowing off somebody for 50% as a loan rate, you can borrow up Creditas and get for 10% if you put your home in a Brazil context. So, it is a good ethical ESG overlay what they do. It is a scale space. It is $500 billion existing unsecured credit in Brazil today. And that needs to be replaced by more longer-term secured credit over time.

The Creditas loan book is only about 300 $ – 400 $ million today. So, the thing where they can grow 2-3x a year for the next 10 years is very realistic, given their size and shape. Also, they are doing a lot more around the collateral of home, auto, and payroll, where they are getting deeper into these three ecosystems and providing more financial services around these kinds of products suite.

So, they were lending against cars. Now they are lending to buy a car. Now to do insurance for cars, you need a buyer buying and selling cars. So, there is a whole ecosystem going in around the car. And they are doing something similar at home. They are doing something like payroll. And as we talked about earlier, the moving from Brazil into Mexico. So, from one scale market into another. It is a company that was valued at $1.7 billion in its last investment round in Q4. It is on a path towards IPO, which we with the exits and transparency and pricing. It may raise more capital before it gets to IPO. We will see. But this is a company where we can see the predictability of compounding of value from a bigger base is very real. And that is something that gets us excited.

So, it is not always companies, which. “What is it yet? We do not know.”, or “How will it monetize?” or “What happens next year?” There is a real degree of forecast ability around the path that they are on – with some risks, always. But that is what excites us a lot, and we can see the value in this compounding. This is a 10 $ billion. It could be a 100 $ company in the making because they are a part of the future of finance in Brazil. They are on a very strong path towards it.

This is a 10 $ billion. It could be a 100 $ company in the making because they are a part of the future of finance in Brazil. They are on a very strong path towards it.

Potential risks for Creditas

[00:54:11] Tilman Versch: What are the risks you are seeing for Creditas?

[00:54:12] David Nangle: Most of the risk for a lot of our company starts at a country level, whether it is macro markets regulation. But specifically, for Creditas, I think this is one area in that banks could do well. And the banks…

Fintech exists because banks are just – well they are old world. They were asleep at the wheel, and they allowed for innovation to come in around them. So, I think this is an area where the banks have maybe some competitive advantages around the cost of capital, and they have a lot of the customer bases that they’re lending to currently in an unsecured format.

So, I think the biggest risk for Creditas is around the competitive aspect, but we have not seen anything too much there.

So, the banks must undercut their own revenue to give their own customers a better product at a better price point. But it is possible they could do that. So, I think the biggest risk for Creditas is around the competitive aspect, but we have not seen anything too much there. And it is such a big space that there is room for more.

Ideas for future developments for Creditas

[00:55:05] Tilman Versch: What will change in your ownership, if they do a successful IPO? Will you keep the shares in the VEF structure? Or will you carve them out to shareholders, or will you sell? What are your ideas?

[00:55:15] David Nangle: We are open. We are open to making the best decision to create as much value as possible. So, the fact that they are on a path towards IPO is super welcome. We welcome that. We support that. Will the IPO be next year? The year after? We do not know. It will be a function of the markets and when we are ready. When we get to that point in time, we will see how the company is doing, how we predict the future of the company, and what price the IPO is done at.

We could very easily not sell a share in the IPO and hold on for another five years. Or we could sell everything in the IPO because we think it has gone far enough or it was an IPO that everybody wants a piece of, and its price way too high. So, we would have to make decisions at the time. Most realistically is probably a case of taking X off the table in the IPO and holding Y for the journey thereafter. But there is plenty of time to get into that before we get there. I think in the meantime, what we want to see is: This company continuing to compound up in value. Our shareholders are getting closer to it, understanding it, that it is being reflected in our share price and everybody is happy.

Investment thesis for Konfio

[00:56:25] Tilman Versch: What is your investment thesis for Konfio?

But Mexico is a much more unbanked and under-banked market and cash first market, as you were referring to earlier.

[00:56:30] David Nangle: Konfio is an interesting one because the Mexican market is nothing like Brazil in terms of opportunity. It is a big market – albeit smaller than Brazil. But Mexico is a much more unbanked and under-banked market and cash first market, as you were referring to earlier. The opportunities we see in Mexico are more based around small businesses. I think as a small addressable consumer market in Mexico versus Brazil – very unbanked and under-banked markets. So, you are looking at classic fintech. We saw a lot of opportunity in the small business space where the big banks were focusing on big corporations and then microfinance has focused on very small corporations. So, we were looking for something in a small business space and in small business payments, credit, or ERP management information systems.

But they have an aspiration of becoming like what Square is in America or TAG and Stone are in Brazil, which is a small business financial services ecosystem.

And we found Konfio, which is focusing on the credit space, small business credit. But they have an aspiration of becoming like what Square is in America or TAG and Stone are in Brazil, which is a small business financial services ecosystem. So, for small businesses, you do their payments, you do their credit, and you do their management information systems or accounting and processing. And that is the path that they are on. So, credits first, but they have also now moved into payments, inorganic as well as organic, and same with ERP.

So, this is a company which in the last round was worth about 300 $ million. They are probably having to raise more money this year. And this is a company that will support them in that journey. But this is one that can be the dominant financial services play for small businesses in Mexico and. And even across the world, Tilman, you find the small businesses – I guess Germany is an exception because small businesses are everything in Germany and the banks are built to support small businesses. But you know, elsewhere in the world, small businesses are one of the biggest unserved parts of financial services. Everybody focuses on consumers or big corporations, but small businesses do not get a lot of love. So that is a big opportunity.

Optionalities in the businesses

[00:58:22] Tilman Versch: That’s interesting. What do you think about optionalities in the businesses you own? You can also think about certain examples. What businesses might come out of these businesses, where you might have a chance to even conquer new markets?

[00:58:40] David Nangle: I think there are two things about that. I think one is broader than financial services. So, what we are seeing globally are companies that are in e-commerce, social, ridesharing, and moving into financial services. So, you see Google, Apple, Facebook through moving into payments and maybe credit – even Amazon.

At the same time, we are seeing a lot of these new fintech companies moving into the real economy. So, you started off as a digital bank, but also suddenly you are doing ticketing. And you are doing E-commerce or marketplace on top. You might be doing auto lending, but suddenly you are doing buying and selling cars and maybe producing cars. So, financial services are moving into the real world while the real world’s moving into financial services. So, I can see that through a lot of our companies, especially the ones that have a lot of customers, have a lot of brand loyalty and capital, moving beyond core financial services into other areas. Specifically, that can be in areas like health or mobility or education around which people are borrowing for payments in.

So, I can see that through a lot of our companies, especially the ones that have a lot of customers, have a lot of brand loyalty and capital, moving beyond core financial services into other areas.

Geographically, I think there are lots of opportunities, especially Creditas and Konfio. They can dominate Latin America for their product suite. And then going beyond that is probably a push too far, but you never know, REVO is across Eastern Europe now, and Jumo in Africa could easily be across Southeast Asia, which is a very similar market to the subcontinent and Southeast Asia. So, geographic expansion is a lot easier than product expansion. But that product rollouts beyond the core that they are all delivering on, can be a financial service, which is easy to go from payments to credit to investments to insurance. Outside of financial services – that is starting to happen, which is probably one of the more interesting dynamics that we are seeing.

Follow Tilman for more insights

Follow Tilman for more insights

Moving concepts out of emerging markets to developed markets

[01:00:27] Tilman Versch: There are some innovative concepts coming from emerging markets as, for instance, like in China, every social media company in the West now looks at China and copies them. Could you think about moving concepts from emerging markets and to develop markets?

[01:00:45] David Nangle: The problem with developed markets is that everything works. So, we have had all the iterate financial services. We have gone from cash to check to card to mobile. But cash still exists and credits, checkbooks still exist in some markets, and cards still exist, physical plastic cards and mobile phones. You go to China, and you jump from cash to digital. So, you would love to be able in a lot of developed markets to jump to the future. But in many emerging markets or frontier markets, specifically, you can go straight to the future, and you can jump or leapfrog all these different phases.

The problem with developed markets is that everything works.

So, I guess if you are going to Sudan, or you going to Bangladesh or pick a market. And you are looking at the future of funds, you do not have to go through all the historic chapters, and you can go straight to the best in class. You mentioned China. China has a great track record of data just moving straight to digital because it was driven by the new economy companies.

So, I think there’s learning there, but I think that the unfortunate part about the developed markets is: We have a history. You do not get rid of those things gradually and then innovators come through. And they take the top of the ends of the pyramid, and it comes rolled through to everybody else. So, I do not know if we could do take the benefits of emerging markets to the developed world in such a dramatic sense. Gradually, but not as dramatic as what happens in China, where you go from cash over here to a hundred percent digital over there.

The next frontiers

[01:02:24] Tilman Versch: Could we expect new regions or topics you might see coming up in your pipeline and you are playing with?

[01:02:26] David Nangle: I think regionally what we are, where we are heavy is Brazil, Mexico, India. That is where we are spending a lot of time. But beyond them, we are looking at the next frontier growth markets. Pakistan gets a lot of time. Egypt is getting a lot of time. We would love to do the first investment in Egypt. And that is all while still, we love markets like Russia and Turkey, which are always on our radar. I think what is more interesting is on a segment’s viewpoint, where embedded fintech is becoming more interesting. Where we are looking at more companies in education, healthcare, rideshare, which is not our core. But they are getting more into fintech, whether it is payments, credit investments, insurance, and it is becoming a bigger part of their business.

So, we are looking at them, with fintech eyes, even though they are not a core fintech companies. So, I guess what, you could see something popping up in our portfolio in health or education. And you might go, what the hell is that? But there is an aspect of fintech and a growing aspect of fintech in that. So, I guess that is probably the most interesting one. And then do the insurance parts where classic fintech innovation is being quicker or deeper than what has happened on the insurance side. The insurance opportunity is as big. So, we are looking at the innovation and that is probably the next wave of investment source to do, you know, as that progresses.

Opportunities in the portfolio

[01:03:48] Tilman Versch: In your smaller positions or the “dwarfs” in your portfolio: Which companies are you most bullish on? Where do you think they could double and double and double for the future that makes them a bigger position?

[01:04:01] David Nangle: On top of the pile still stays Creditas because it is doubling and doubling before our eyes. If something that doubles is small, it is fine. But something doubles when it is big, it just gets bigger. And so, we love the doubling – the super compounding of value from that side. So, it kind of helped pointing to Creditas because that makes everything tick.

That said, if I look through our portfolio and some of the names that exist across different areas. Like there are more recent ones in India. India – such a scale market. But it is Juspay and mobile payments or rupee gold back lending. No matter how you look at them, they are only getting started even though they are a company worth north of a 100 $ million dollars. There is so much scale in that market and so much wealth creation on an individual and collective basis in that market. From a macro perspective, you cannot help, but be excited by the Indian opportunities in the portfolio.

I guess I am looking at a specific FinanZero in Brazil, which is very early. It is a marketplace for lending. But lending is just booming in Brazil, and they are just sitting in the middle.

But if it went back down to the smaller end of the scale, and what is interesting. Which one would I pick? I guess I am looking at a specific FinanZero in Brazil, which is very early. It is a marketplace for lending. But lending is just booming in Brazil, and they are just sitting in the middle. They are not taking it onto the balance sheet. They are just connecting lenders to borrowers like the smarter model in Europe or Lendo in Scandinavia. Copy-paste, replicate: We talked about this. Great founders executing and that they just can keep on doubling and doubling. Without taking any balance sheet risks, just being part of the market trends. So, that is quite nice to see play out.

VEF in 5 years (community exclusive)

[01:05:38] Tilman Versch: You’re now like five-plus years at VEF and looking out like five years to 2026, where do you see your VEF and yourself?

Closing remarks from David

[01:06:30] Tilman Versch: I am going to give you the room to add something we have not discussed. Is there anything you want to add to our conversation?

[01:06:35] David Nangle: I think it is a big thanks for this interview and for how prepared you have been on the questions you have asked. Because you have hit all the right spots in the high notes.

Two it is an element of the space that we are in, the markets – emerging markets – and fintech we are only getting started in terms of, five years in, a lot of value created, but you know, there is a long-term journey here and we are very comfortable in our own skin. And there will be cycles in this and what we do. These markets blow hot and cold. But we are doing it for the next 5, 10, 15, 20 years. So, we are making decisions today, which are very much focused on that long-term horizon, as opposed to maybe some of the classic VCs, which raise a fund to close a fund, raise another fund to close a fund. Ours is evergreen and it is important that we think long-term.

But we are doing it for the next 5, 10, 15, 20 years. So, we are making decisions today, which are very much focused on that long-term horizon, as opposed to maybe some of the classic VCs, which raise a fund to close a fund, raise another fund to close a fund.

Thoughts on scalability

[01:07:31] Tilman Versch: Maybe let me do another follow-up question: What do you think about the concept of scale and scalability? Do you see any innovations enabling your companies and investments to scale even more?

[01:07:47] David Nangle: The innovation of the smartphone, which is obviously a historic innovation, has been the great enabler for a lot of fintech like it has been for a lot of new economies. And then the penetration of that, and the availability of Wi-Fi globally has been key to enable this. And a lot of countries are mobile-first, like India, Pakistan. They will never be desktop first or a smart device versus a smartphone first. So, I think that is the innovation that continues to drive. You combine that with the right regulatory drive and the right wealth levels and growth levels in a certain market, and it comes together as a great force of opportunity. I think also what is drawn is the capital, the amount of capital to support these companies in these countries today is more than ever. So, it is not innovation, but its capital being drawn into countries delivered by innovation. So, it is a great time to be in these markets and where are you seeing this volume and these companies being enabled to create what is being created in the developed markets over many years.

[01:08:55] Tilman Versch: Maybe another question. What is the main interface your consumers are interacting with the companies you invested in? Is it the mobile phone?

[01:09:03] David Nangle: It is. The Turkeys, the Russias, the Brazils – you get some desktops and laptops. But realistically north of 50% is mobile-first. You go to India, it is 80%, 90% mobile-first. So, the more frontier the market, the more it is cheap smartphones being purchased from China – the device upon which a lot of these companies’ success is being built. I think smartphone first and that is where these countries are.

[01:09:35] Tilman Versch: Are there any higher percentages of personal interaction or other interfaces, people are interacting with the companies you are invested in?

[01:09:45] David Nangle: Like on a person-to-person basis there is some call center support in some markets to some agents and agency networks, like Konfio and small business. Minu, which is wage advanced. And so are Europe, Brazil, and Mexico. They are working with HR departments. So, some outbound sales teams, but do any of our companies have branches? No. Physical locations? No. But they do have people that may be doing call centers or maybe outbound sales. But it is digital-first across the board.

[01:10:19] Tilman Versch: David, thank you very much for this great insight into your company and for your time. Thank you!

[01:10:23] David Nangle: Thank you.

[01:10:28] Tilman Versch: And bye-bye to the viewers and listeners.

[01:10:29] David Nangle: Bye-bye!

[01:10:34] Tilman Versch: Here is the disclaimer. You can find the link to the disclaimer below in the show notes. The disclaimer says: